The First Cyber-Kinetic War. AI’s Loyalty Test. The Mineral Map Redraws.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

This week wasn't about tech news. It was a stress test, and the results tell us something important about where we actually stand.

The stories in this week's GeoTech Radar aren't isolated incidents, and once you see the pattern you can’t deny it. Decisions about what infrastructure we trust, who controls our tech stacks, and where we plant our ethical flags are now inseparable from the P&L. They expose us directly to potential liability but, if we’re thoughtful about it, they can provide us with a survival plan, as well.

Here's what I kept coming back to this week:

Whoever controls the processing layer controls the game. Iran built a censorship network on Huawei infrastructure but, when Israel flipped the switch, Iran lost command-and-control of its own systems. OpenAI just closed a record $110 billion round, but what it really did was lock in a vertical fusion of capital, compute, and customers so tightly that everyone outside it is now a cognitive tenant paying rent in money and agency. Kazakhstan is sitting on rare earth deposits that could reshape critical supply chains, but without refining capacity they're just holding someone else's raw materials. The chokepoint in every one of these cases – the mine mouth, the model weights, the data center, the satellite – is the processing layer. If you don't own it, you depend on whoever does.

The line between "foreign" and "domestic" is gone. I know that might be uncomfortable, but look at the facts. The Pentagon deal that Anthropic refused could have turned frontier AI into a domestic surveillance instrument with no meaningful guardrails. ICE is already running that instrument through Palantir – warrantless and at scale. The cyber tools used to degrade Iran's internet were built on the same dual-use logic as the commercial spyware sitting in an ICE agent's pocket right now. And Meta is about to hand facial recognition to anyone wearing a pair of smart glasses, giving them the same capability governments used to build for themselves, only now privatized and consumer-grade. These technologies simply don't recognize the legal categories we spent decades constructing. That's not a policy gap, it’s a strategic reality you need to plan around.

Loyalty has become a procurement criterion, and the negotiating window is shorter than you think. Anthropic drew a principled line with the Pentagon deal. I respect that, but it also cost them a near-existential commercial hit. OpenAI took a different path, with secured classified access under terms where the safeguards depend on existing law, not contractual prohibitions. When critics showed that existing law still permits the same surveillance Anthropic refused to enable, Altman revised the contract in 72 hours. This isn't a morality contest between two companies. It's a masterclass in how leverage works when the state becomes your largest potential customer. When you negotiate, what you refuse to put in writing matters as much as what you sign. Every frontier AI company, every defense contractor, every enterprise software vendor needs to understand that calculus.s It has become a boardroom reality.

Taken together, these trends illustrate how the global GeoTech map is being redrawn around whoever owns the infrastructure everyone else runs on – chips, satellites, minerals, data pipelines, and AI models. These aren't just inputs into the economy. They are the new instruments of cognitive power, simultaneously defining who profits, who is trusted, and who governs. Yes, some will draw the parallel to Big Oil and the commanding heights of the industrial era, but that analogy flatters us with the idea that we understand what's happening. This is different. The power shifts depending on who gets to see, say, do, mine, and profit from whom, what, when, and on what terms.

Your profits are someone else's politics. And their politics will become your problem, whether you planned for it or not. It’s circular and you can’t escape it.

The leaders I talk to who navigate this well aren't the ones who have all the answers. They're the ones who've stopped pretending the question doesn't apply to them.

On the Radar

The signals affecting the GeoTech landscape this week

The First Cyber-Kinetic War: Iran, Digital Sovereignty, and the Gulf’s Compute Exposure

The U.S. and Israel hit Iran with the largest cyberattack in history, in which cyber was the primary, synchronized lead for a major bombing campaign. Gulf compute infrastructure is in the blast radius.

BRIEFING: The United States and Israel launched coordinated strikes against Iran on February 28 under Operations Epic Fury and Roar of the Lion. Israel simultaneously executed a layered cyber offensive that combined electronic warfare, denial-of-service attacks, and deep intrusions into energy and aviation systems, collectively degrading the IRGC’s communications to prevent a coordinated counterattack. NetBlocks confirmed Iran’s internet connectivity dropped to just 4%. The cyber campaign exploited the “Barracks Internet” architecture Iran built for itself, which routed all traffic through state-controlled chokepoints built with Chinese-supplied equipment from ZTE, Huawei, Tiandy, and Hikvision . The same centralized design that isolated 85 million citizens from the global internet severed the regime’s own command-and-control from its military units when attackers targeted those chokepoints.

Iran’s retaliation turned the war into the scenario the Gulf had not planned for. Tehran launched more than 180 ballistic missiles, 800-plus drones, and cruise missiles at eight countries. The UAE absorbed the worst of it, with drone debris striking Dubai International Airport, Jebel Ali Port, Palm Jumeirah, and the Burj Al Arab. As of midweek, three people were killed and roughly 70 wounded. The IRGC declared the Strait of Hormuz closed and threatened to attack any vessel that attempted passage. Commercial shipping effectively halted, and at least five tankers were damaged and 150-plus ships stranded. Major insurers cancelled war risk coverage, and Maersk and Hapag-Lloyd suspended transits. Brent crude prices rose 13% since the conflict began.

Drones struck two AWS data centers in the UAE and damaged a third in Bahrain, the first time a major U.S. tech company’s data center has been taken down by military action. AWS told customers to migrate Middle East workloads to other regions immediately. The January 2026 Pax Silica framework, the U.S.-UAE chip security partnership, was designed to keep advanced semiconductors away from China. It did not contemplate someone firing missiles at the buildings where those chips run.

SO WHAT FOR LEADERS: If your organization runs workloads in AWS’s Middle East regions, follow Amazon’s own guidance and migrate critical workloads now. If your supply chain or energy exposure routes through the Strait of Hormuz, activate contingency plans today. The conflict is ongoing, the IRGC claims complete control of the strait, and the UAE is publicly weighing direct strikes on Iran, which would escalate the threat further. Audit every cloud, logistics, and energy dependency that touches the Gulf and map which ones have no alternative path.

The deeper question is whether the Gulf’s AI infrastructure thesis survives this war. Less than a year ago, the UAE and Saudi Arabia were celebrated as the next frontier for artificial intelligence. Microsoft committed $15 billion to UAE data centers. The Stargate UAE campus and Saudi’s Humain initiative promised gigawatts of new compute. The security frameworks around those deals were built for supply chain control and geopolitical alignment, not for protecting buildings during a regional war. That gap is now exposed. Reassess any AI infrastructure investment predicated on Gulf compute availability, and recognize that any government operating a centralized internet kill switch has built both a tool of control and an attack surface for adversaries. Iran proved both propositions in the same week.

Blacklisted for Ethics: Anthropic, the Pentagon, and the Price of Saying No

The DoW designated an American AI company a national security risk. Does loyalty beat integrity?

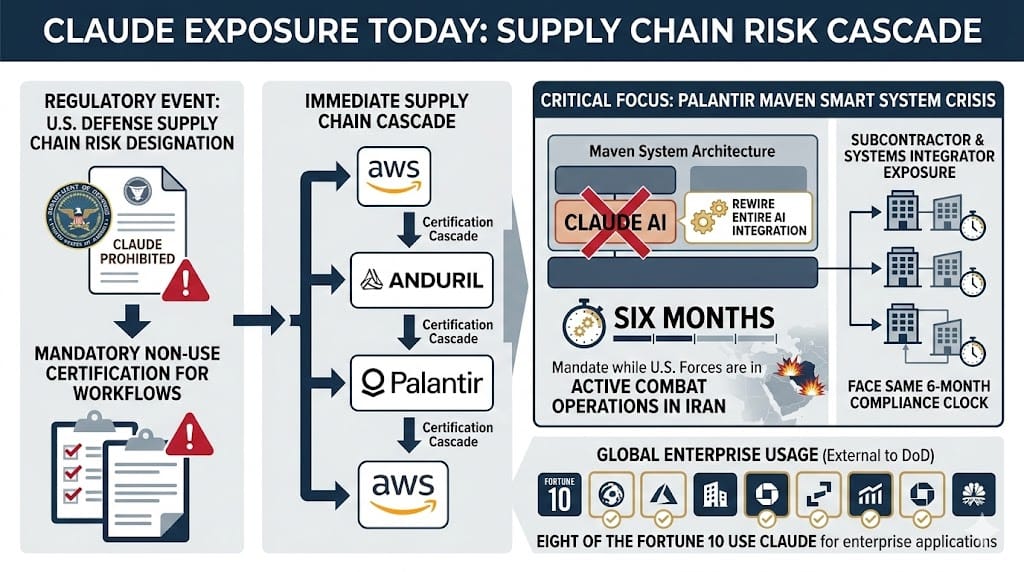

BRIEFING: The Trump administration designated Anthropic a “supply chain risk to national security” on February 27, a classification previously reserved for foreign adversaries like Huawei. President Trump ordered all federal agencies to cease using Anthropic’s technology immediately, with a six-month phase-out for the Department of War. Defense Secretary Hegseth declared the designation minutes after his Friday deadline passed. Trump posted that Anthropic “better get their act together” during the transition “or I will use the Full Power of the Presidency to make them comply, with major civil and criminal consequences to follow.” Anthropic vowed to challenge the designation in court.

Axios reported that the specific deal Anthropic rejected included the collection or analysis of Americans’ personal data, including geolocation, web browsing, and personal financial data purchased from brokers. CEO Dario Amodei responded, “We cannot in good conscience accede to their request.” and warned the technology could enable “billions of AI-controlled drones” and convert “scattered data into complete life portraits.” Hours later, OpenAI announced a Pentagon deal for classified network access. CEO Sam Altman said the deal was “definitely rushed” and admitted it “looked opportunistic and sloppy.” OpenAI claims three red lines: no mass domestic surveillance, no autonomous weapons, no social credit systems. However, the safeguards differ from what Anthropic sought. Anthropic demanded contractual prohibitions beyond existing law. OpenAI’s agreement relies on compliance with existing statutes, including Executive Order 12333, which critics note still permits significant data collection on U.S. persons. By March 3, Altman announced revisions to the contract, adding explicit language that the system “shall not be intentionally used for domestic surveillance of U.S. persons and nationals,” including commercially acquired data. OpenAI also stated it would not allow intelligence agencies to use its tools. The original terms did not contain these restrictions.

SO WHAT FOR LEADERS: When the state can designate an American AI company a national security risk for refusing to cross an ethical line, every company that sells to the government faces the same calculation. The question is not whether your technology could be used for domestic surveillance. The question is what you will do when your largest potential customer asks you to allow it. Anthropic drew a principled line and paid a near-existential commercial price. OpenAI negotiated terms it then had to publicly revise within 72 hours after backlash. Neither path was clean. But leaders in every sector that touches government procurement need to decide now, before the ask comes, where their own lines are.

For companies with existing Pentagon exposure, the compliance clock is immediate. The supply chain risk designation forces every defense contractor to certify it does not use Claude in its workflows. Palantir built its Maven Smart System on Claude and must now rewire its entire AI integration on a six-month timeline while U.S. forces are engaged in active combat operations against Iran. Eight of the Fortune 10 use Claude for enterprise applications. Audit your Claude exposure today and model the brand risk of compliance across all your business segments, not just the defense vertical.

The Steppe Dividend

Kazakhstan discovered enough rare earths to rank third in the world. The minerals map has a new heavyweight, though processing questions remain.

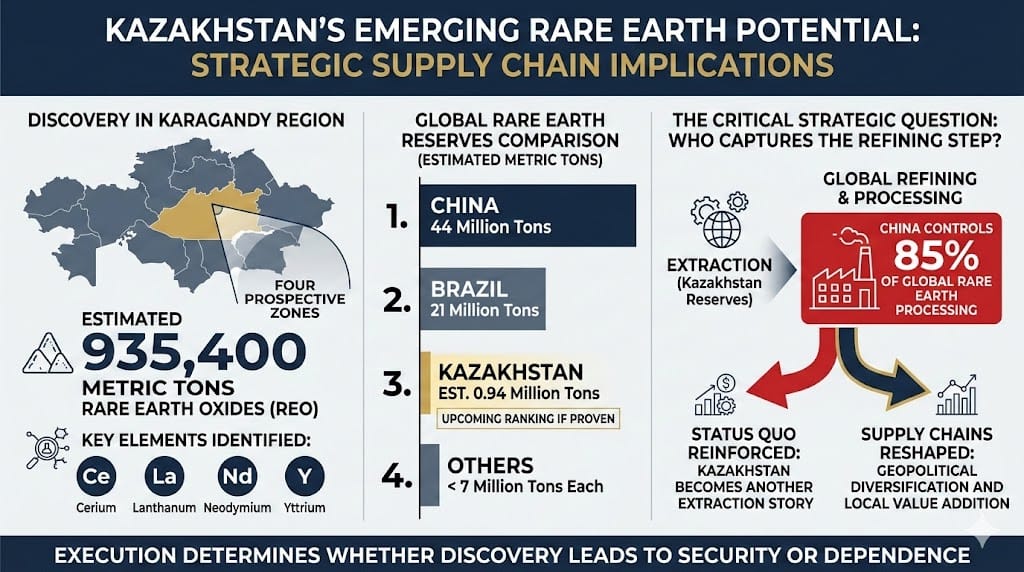

BRIEFING: Exploration in Kazakhstan’s Karagandy region has identified an estimated 935,400 metric tons of rare earth oxides, including cerium, lanthanum, neodymium, and yttrium. Geological modeling suggests the wider ore body may extend to 20 million metric tons. If those projections hold, Kazakhstan would rank behind only China (44 million tons) and Brazil (21 million tons) in global rare earth reserves. No other country currently exceeds 7 million tons, according to U.S. Geological Survey estimates. Arthur Poliakov, executive chairman of the MINEX Forum, estimates that extraction is 10 to 12 years out, with initial investment needs starting at $10 million before accounting for downstream processing infrastructure that Kazakhstan does not yet possess.

Kazakhstan timed the announcement strategically. The discovery was disclosed on the eve of the first EU-Central Asia Summit in Samarkand in April 2025. The EU-Kazakhstan cooperation framework on critical raw materials predates the find. A strategic partnership was signed at COP27 in November 2022. But the Karagandy disclosure elevated Kazakhstan’s position within that framework. EU Ambassador Aleška Simkić confirmed the timing was deliberate, stating it “succeeded in putting Kazakhstan on the map for the EU.” Brussels endorsed a cooperation roadmap naming Kazakhstan a priority partner and has committed more than 10 billion euros under its Global Gateway program, with 2.5 billion euros earmarked specifically for critical raw materials, transport through the Caspian Sea via the Middle Corridor, clean energy, and digital connectivity. The Atlantic Council published a policy brief calling for a U.S.-Kazakhstan cabinet-level task force and recommending the Development Finance Corporation and Export-Import Bank prioritize Kazakh mineral projects.

SO WHAT FOR LEADERS: The question that determines whether this reshapes supply chains or becomes another extraction story is who captures the refining step. China controls 85% of global rare earth processing. If Karagandy’s minerals end up in Chinese processing facilities, Kazakhstan subsidizes Beijing’s industrial sovereignty. The Atlantic Council’s recommendation to co-locate processing near the mine head with Western financing is the critical variable. We recommend a US-EU-Kaz joint venture for maximum expertise pooling, supply and demand complimentary and resilience. The EU corridor investment is committed capital for distribution infrastructure. The U.S.’s FORGE framework creates preferential terms for aligned mineral suppliers. That is a strong combination. Meanwhile. Beijing has countermoves, such as market saturation to collapse prices, restrictions on Chinese engineering collaboration, or pressure through Moscow.

For corporate procurement and institutional investors, this is a positioning window. The organizations that build Kazakh relationships now, especially with investments to build local capabilities that differentiate from Chinese ones, will have a structural advantage when extraction begins. The conditions are favorable: The Astana International Financial Centre operates under common-law, English-language legal infrastructure designed for Western capital entry.

No Fab, No Fix: The $10.6 Trillion Taiwan Scenario the Industry Refuses to Plan For

The CIA warned Silicon Valley three years ago, and the industry just shrugged. The 2027 timeline keeps closing in.

BRIEFING: A New York Times investigation revealed that CIA Director William Burns and Director of National Intelligence Avril Haines personally briefed Apple’s Tim Cook, Nvidia’s Jensen Huang, and AMD’s Lisa Su in a classified 2023 session, warning that China could move on Taiwan by 2027. Taiwan produces roughly 90% of the world’s most advanced chips. Treasury Secretary Scott Bessent told Davos last month that a blockade would be “an economic apocalypse.”

The industry’s response to geographic diversification has been slow, because fab and talent development take much time and capital. As a result, domestic chips also cost over 25% more than Taiwan produced ones. TSMC’s Arizona expansion is advancing, but McKinsey’s semiconductor practice leader captured the prevailing mindset, executives believe “if we’re screwed, everyone else is screwed” and take no action. Bloomberg Economics modeled five Taiwan scenarios and found the worst case would erase $10.6 trillion in global GDP in year one, eclipsing COVID-19 and the 2008 financial crisis.

SO WHAT FOR LEADERS: Run a 90-day advanced chip supply disruption scenario and identify which systems degrade first. Japan’s Rapidus and TSMC Kumamoto will not reach volume production before 2028. TSMC’s Arizona fab is advancing but domestic chips still cost over 25% more than Taiwanese production. Intel’s Ohio expansion and Samsung’s Texas facility remain years from volume. No U.S. site closes the concentration gap before 2028. The gap between today’s Taiwanese concentration and credible alternative supply is years, not months. Lock in alternative sourcing agreements now. Once formal diversification begins, everyone competes for the same constrained capacity.

The geopolitical trajectory heightens the urgency. President Trump’s transactional posture toward Taiwan, demanding 10% of GDP on defense and 40% semiconductor onshoring, signals to Beijing that Washington’s commitment is conditional and extractive. Xi has leverage through rare earths, trade and President Trump’s self-image as dealmaker. The military timeline might stretch, but the strategic trajectory favors Beijing. Trump’s transactional framing signals to Xi that Washington’s commitment to Taiwan is conditional, which lowers the perceived cost of coercion. Xi has additional leverage through rare earth export controls, trade negotiations, and Trump’s self-image as dealmaker. Plan for disruption before the market prices it in.

Musk’s Orbital Stack Grows

SpaceX absorbs xAI, files for a million satellites, and eyes the largest IPO in history. Grok enters classified systems as Claude exits.

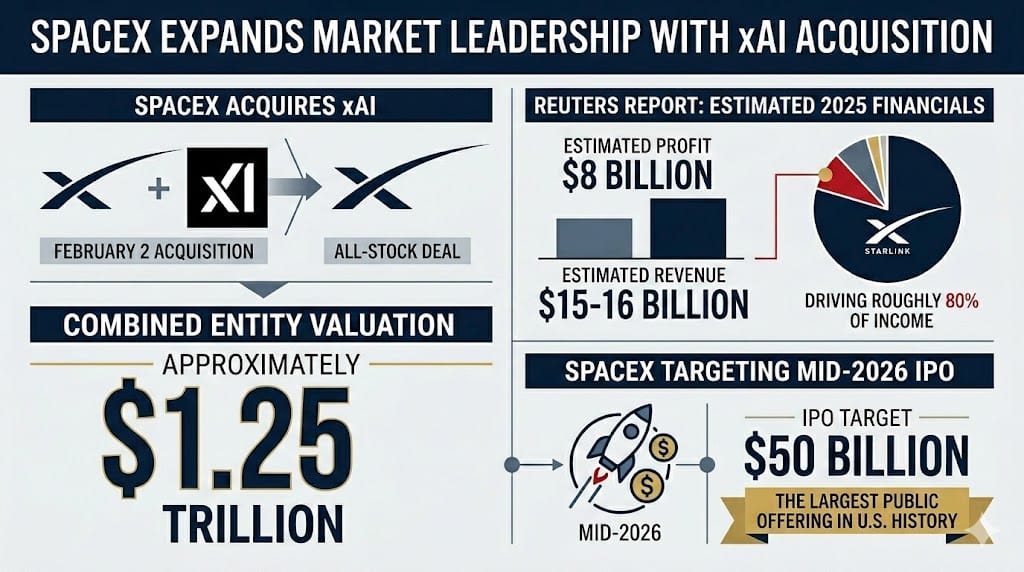

BRIEFING: X and xAI announced on March 2 that they will repay $17.5 billion in combined debt in full. The repayment includes $3 billion in xAI high-yield bonds being redeemed at approximately 117 cents on the dollar, a significant premium for an early buyback on securities issued just last June at a 12.5% coupon. Morgan Stanley, which handled both companies’ debt, has been informing lenders. The source of the $17.5 billion has not been disclosed, though xAI raised $20 billion in equity in January.

The debt clearance is a balance-sheet cleanup ahead of SpaceX’s anticipated IPO. Bloomberg reports SpaceX could file confidentially with the SEC as early as this month, targeting a June listing at a valuation up to $1.75 trillion. This would be the largest IPO in history. SpaceX acquired xAI on February 2 in an all-stock deal creating a combined entity valued at $1.25 trillion. The merger has already prompted a reorganization at xAI, with several co-founders departing. SpaceX announced at Mobile World Congress this week that its next Starship launch is planned in four to six weeks, the first since the merger, with an operational timeline targeting early 2027 flights and a new Starlink satellite constellation by mid-2027.

xAI’s Grok has been deployed within the Pentagon’s classified systems since January. With Anthropic’s Claude being phased out on a six-month timeline, Grok is positioned as one of its primary replacements at the precise moment the Defense Department is running AI-assisted operations in Iran. SpaceX generated an estimated $8 billion in profit on $15 billion to $16 billion in revenue in 2025, with Starlink driving roughly 80% of income. xAI was burning approximately $1 billion per month prior to the merger.

SO WHAT FOR LEADERS: The combined company controls the world’s largest satellite internet constellation, a frontier AI model with classified military access, the only heavy-lift orbital launch capability, and a social media platform. Jared Isaacman, a former SpaceX investor, now leads NASA. No single entity has ever held this combination of defense, communications, and AI infrastructure under one roof. A regulatory framework to govern it does not exist.

If your organization depends on Starlink for connectivity, SpaceX for launch, or Grok for AI, model the scenario in which a single corporate decision, regulatory action, or geopolitical event disrupts all three simultaneously. While vertical integration can reduce cost, this is not necessarily true for quasi-monopolies. At a $1.5 trillion IPO valuation, shareholder pressure to monetize every vertical will intensify. Map your new cost structure now.

Under the Radar

The deep analysis that connects the dots

The Surveillance Stack Comes Home

ICE built the most advanced domestic surveillance apparatus in American history using commercial technologies. Half the countries surveilling domestically are democracies, and the U.S. now leads that pack.

The Procurement

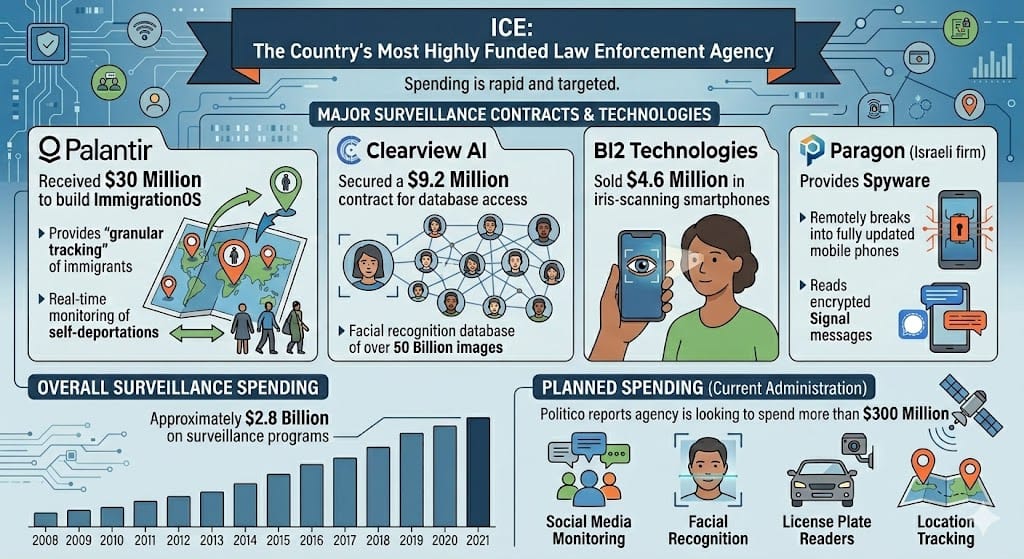

Last summer, Congress transformed ICE into the country’s most highly funded law enforcement agency. The One Big Beautiful Bill Act, signed July 4, 2025, added $75 billion over four years to ICE’s approximately $10 billion base budget, tripling the agency’s effective annual spending to nearly $30 billion. That is more than Poland’s entire military budget. The agency’s subsequent spending on surveillance technology has been rapid and targeted. Palantir received $30 million to build ImmigrationOS, a platform that provides “granular tracking” of immigrants including real-time monitoring of self-deportations. Clearview AI secured a $9.2 million contract for access to a facial recognition database of over 50 billion images. BI2 Technologies sold $4.6 million in iris-scanning smartphones. Paragon, an Israeli firm, provides spyware capable of remotely breaking into fully updated mobile phones and reading encrypted Signal messages. Politico reports the agency is looking to spend more than $300 million specifically on social media monitoring, facial recognition, license plate readers, and location tracking.

The Deployment

ICE agents carry smartphones loaded with Mobile Fortify, a custom DHS app that compares any person’s face against more than 200 million images drawn from DHS, FBI, and State Department databases. The Illinois Attorney General alleges the app has been used more than 100,000 times. A separate Palantir tool called ELITE creates instant dossiers and generates predictive probability scores for a target’s likely location at a given time. Agents can also get warrantless access to Webloc, which tracks phone locations using advertising data from commercial brokers. License plate readers already cover cities that are home to three of every four American adults. NBC News documented agents photographing faces of bystanders and protesters in Minneapolis, Chicago, and Portland and running them through real-time recognition software.

The Consumer Convergence

This type of surveillance stack is about to go retail. Meta plans to add facial recognition to its Ray-Ban smart glasses this year through a feature internally called “Name Tag.” Internal documents obtained by The New York Times show Meta is timing the launch for a “dynamic political environment where many civil society groups that we would expect to attack us would have their resources focused on other concerns.” The company sold more than 7 million pairs last year. The glasses look identical to prescription eyewear, and Name Tag would let any wearer discreetly identify people across Meta’s 3.3 billion monthly active users. In 2024, two Harvard students demonstrated a prototype using the same glasses with PimEyes to identify strangers in real time, surfacing names, home addresses, and phone numbers. Meta scrapped Facebook’s facial recognition in 2021 after paying $1.4 billion in biometrics privacy settlements. Now it is putting the same capability back on millions of faces.

The GeoTech Signal

The AI governance debate is overlooking the connection between these threads. The Pentagon deal Anthropic rejected included permissions that would allow analyses of Americans’ geolocation data, browsing history, and financial records from data brokers. ICE already purchases and operationalizes exactly that data, at scale, through commercial vendors and can do so without traditional warrants because of the third-party doctrine established in Smith v. Maryland (1979): information voluntarily shared with third parties, such as phone companies and app providers, carries no reasonable expectation of privacy under current law. The Electronic Communications Privacy Act of 1986 has not been meaningfully updated for the smartphone era. Palantir, the same company that integrates Claude into the military’s classified systems, built ImmigrationOS for ICE. The pipeline connecting frontier AI to domestic enforcement is identical to the pipeline connecting it to military intelligence. Only the customer label changes.

What makes the American model distinctive is not that it exists, but how it was assembled. Iran built the socalled Barracks Internet through explicit state policy, with Chinese-supplied equipment (Huawei, ZTE, Tiandy, Hikvision) and a Supreme Council of Cyberspace established by the then Supreme Leader. The American model achieves comparable surveillance capability through a different mechanism: hundreds of individual procurement contracts and data broker purchases, each defensible on its own terms, that collectively produce a system no single democratic process authorized.

No law mandated ImmigrationOS. No regulation required Clearview’s 50-billion-image database. No vote approved warrantless geolocation tracking. Yet the capability exists, it is operational, and it scales. Senator Markey’s ICE Out of Our Faces Act would ban facial recognition at ICE and CBP, but it faces the same political headwinds as every privacy bill of the last decade. For leaders concerned with the balance between public security and the risk of abuse, the question is not whether new regulations will arrive. It is what governance safeguards you can institute now, within your own organization, before the regulatory environment catches up to the technology.

Cambrian Partner By Invitation

Expert analysis from our global network

Sovereign AI Governance in an Emerging Technological Architecture: The Kazakhstan Approach

Remarkable things are happening in an increasingly critical region of the global economy: Central Asia. Within it, the biggest and most AI-focused economy, Kazakhstan, just took some cutting-edge steps one might otherwise expect from leading AI innovation nations. With the adoption of Kazakhstan's Law on Artificial Intelligence and the launch of sovereign AI infrastructure, the country has entered a new phase of state-level AI governance.

Over the past decade, Kazakhstan has moved from digitizing public services to building the foundations of intelligent governance. This transformation was not limited to technology deployment. It required institutional restructuring, legal modernization, and the development of national computational infrastructure. A centralized data architecture enabled proactive service delivery. Legislative reforms clarified data rights, oversight mechanisms, and accountability standards. More recently, the elevation of AI to the ministerial level marked the institutional consolidation of this transition.

Yet infrastructure, law, and institutional elevation, while necessary, are not sufficient.

In a world where AI governance is increasingly shaped by dominant models associated with China's state-coordinated approach and the United States' market-driven ecosystem, mid-sized states face a structural dilemma. Alignment with a single pole may create short-term regulatory and technological clarity, but over time it introduces structural constraints and strategic exposure. The question is how to design a governance framework that protects sovereign decision-making while preserving technological optionality.

For Kazakhstan, this begins with diversified infrastructure. Computational capacity, data platforms, and cloud ecosystems must avoid geopolitical lock-in. Technological resilience becomes a function of strategic optionality. Second, strict adherence to international legal norms, in data governance, transparency, and cross-border cooperation, signals reliability in a fragmented global environment. Third, digital, institutional, and legal architecture ultimately serve an economic objective: attracting investment, expertise, and trusted partnerships.

For mid-sized states, the defining factor will not be scale, but strategic design. Sovereignty without isolation, and integration without dependency, becomes the core balancing act.

About the Partners

Dmitriy Mun is Vice Minister of Artificial Intelligence and Digital Development of Kazakhstan. He has been directly involved in the development of the national Smart Data platform and contributed to the drafting of Kazakhstan's Digital Code and Law on Artificial Intelligence, which established the country's institutional framework for AI governance.

Askar Sinchev is a technology and digital transformation professional working at the intersection of AI, big data, and institutional innovation. He serves as a consultant to the Executive Office of the President of the Republic of Kazakhstan and engages in international AI governance dialogue as an IVLP alumnus (U.S. Department of State) and a member of the Ethics and Regulation Board of the Global Alliance on AI for Industry (UNIDO).

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 8'