The AI Kill Chain. Beijing’s Blueprint. The Compute Schism.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

I watched this week's events with an unease that did not pass with a good night's sleep. Fortunately, my creative instincts kicked in and I began to see opportunities for change. Hopefully, after wrapping your head around the three main themes in this newsletter, you will, too.

Formal strategy declarations are at best a lagging indicator of your situational awareness. Every story in this issue follows directly from choices that leaders made years ago when nobody was calling them strategic. China's latest Five-Year Plan names AGI as a target, but the infrastructure behind that goal was built years ago. The United States designated Anthropic a supply chain risk after its model was already load-bearing inside the most advanced targeting system in the world. Ukraine can build a China-free drone, but the magnets, the battery cells, and the gallium-nitride chips are still Chinese because that was the cheaper call two years ago. Europe declared digital sovereignty, but cloud contracts run for years. In every case, the strategy arrived after the architecture. By the time the document circulates, the window has already closed. That pattern, while alarming on its face, could open up new opportunities for companies and governments to get better at sensing early signals and leading indicators to calibrate their strategies going forward.

Speed has outrun accountability. The deaths of more than 160 people at an Iranian girls' school in Minab shook many of us to the core. The analysis of the strike suggests that outdated data and too few human planners failed to safeguard against the error before it became a strike. This does not appear to be an algorithmic failure in the narrow technical sense. It looks like a human and organizational failure enabled by a system optimized for speed over verification. But that distinction offers cold comfort, because it points to something we need to be far more honest about. AI models could carry epistemic closure as a design feature. They are built to converge fast, which means they can be structurally resistant to countervailing information that arrives late or sits outside their training. That is a fine property for throughput, but it is a lethal one when the output is a strike authorization. Human oversight is not a concession to slowness. It is the only verification layer capable of staying open to what the model has already ruled out. We now have an opportunity and the motivation to build that layer before we need it again. We will not have time to build it after.

Declared intent has outrun operational capacity, and that opens the door for agile, frugal approaches. European governments are decoupling from U.S. platforms while their private sectors cannot. Kazakhstan has critical assets, genuine political will, and a credible broker architecture, but it does not yet possess the institutional capacity to execute on them. Ukraine can produce a China-free drone but not at the scale the battlefield demands. The U.S. designated its own AI provider a risk while depending on it for its most sensitive operations. I see this pattern everywhere I advise. Leaders articulate a new vision, start expecting execution and then discover that the legacy reality beneath them points in a different direction and creates drag. This is a governance and transformation problem, and it compounds quietly until it is too big to ignore. Fortunately, these execution gaps provide us an opportunity to air out old liabilities, re-design architecture, and partner for new capabilities. That is precisely when agility and frugality beat legacy and scale.

The world is not waiting for your organization to catch up. Neither, frankly, should you. You face a tough challenge with moving targets. To that end, I hope you’ll find this issue valuable and look forward to hearing from you one way or another.

– Olaf

On the Radar

The signals affecting the GeoTech landscape this week

The AI Kill Chain: Machine-Speed Targeting Rewrote the Rules of War in Four Days

The U.S. struck more than 5,500 targets in Iran using AI-driven targeting that compressed kill chains from hours to minutes. Every military on earth is watching.

BRIEFING: During the first 96 hours of Operation Epic Fury, U.S. forces struck more than 2,000 targets inside Iran. By March 11, CENTCOM commander Admiral Brad Cooper reported the total exceeded 5,500. The pace far surpassed the opening of the 2003 Iraq invasion. The Department of War’s chief digital and artificial intelligence officer confirmed that the Maven Smart System, built by Palantir, compressed the targeting cycle from what previously required eight or nine separate systems and hours of human review into a single integrated workflow. A defense technology expert told the Financial Times that legacy kill chains “are measured in hours and sometimes days” and that AI’s purpose is to compress that timeline to “seconds and minutes, almost instantaneous.”

Maven processes intelligence from satellites, drones, radar, and more than 150 additional sources to identify targets, match them with weapons, and estimate civilian casualties before human commanders authorize strikes. During the 2003 Iraq invasion, a 2,000-person intelligence unit handled target identification. In Operation Epic Fury, roughly 20 personnel carry the same workload. The system relies in part on Claude, Anthropic’s AI model, which serves as the reasoning engine inside Maven’s decision-support architecture. That dependency persists, for now, even as the Department of War designated Anthropic a supply chain risk and ordered a six-month transition to alternative providers. Members of Congress have called for oversight hearings. A strike on a girls’ school in the Iranian city of Minab that killed more than 160 people has intensified scrutiny of how targeting decisions are validated at machine speed.

SO WHAT FOR LEADERS: This conflict is the first large-scale demonstration that AI can compress the decision cycle of a major international war. Defense procurement officers should expect every allied military to accelerate adoption of integrated AI targeting platforms over the next 12 to 24 months. The Maven system’s single-platform architecture will become the baseline standard. Companies that cannot deliver equivalent capability will lose contract access. For tech providers not willing to participate in the AI kill chain, audit your defense-tech portfolio for exposure to it. If your firm supplies sensors, communications, or intelligence software, your integration timeline with platforms like Maven just shortened dramatically.

For leaders outside defense, the operational learning matters just as much. Decision compression driven by AI applies to supply chain management, financial trading, and infrastructure operations. The organization that moves the fastest from detection to action sets the tempo for everyone else. Build your verification and oversight layer now, before the speed of your AI systems outpaces your ability to audit them. The Minab school strike is a warning of what happens when the pace of algorithmic output exceeds the pace of human judgment. Ethical fallout and legal liability can accrue along many different dimensions.

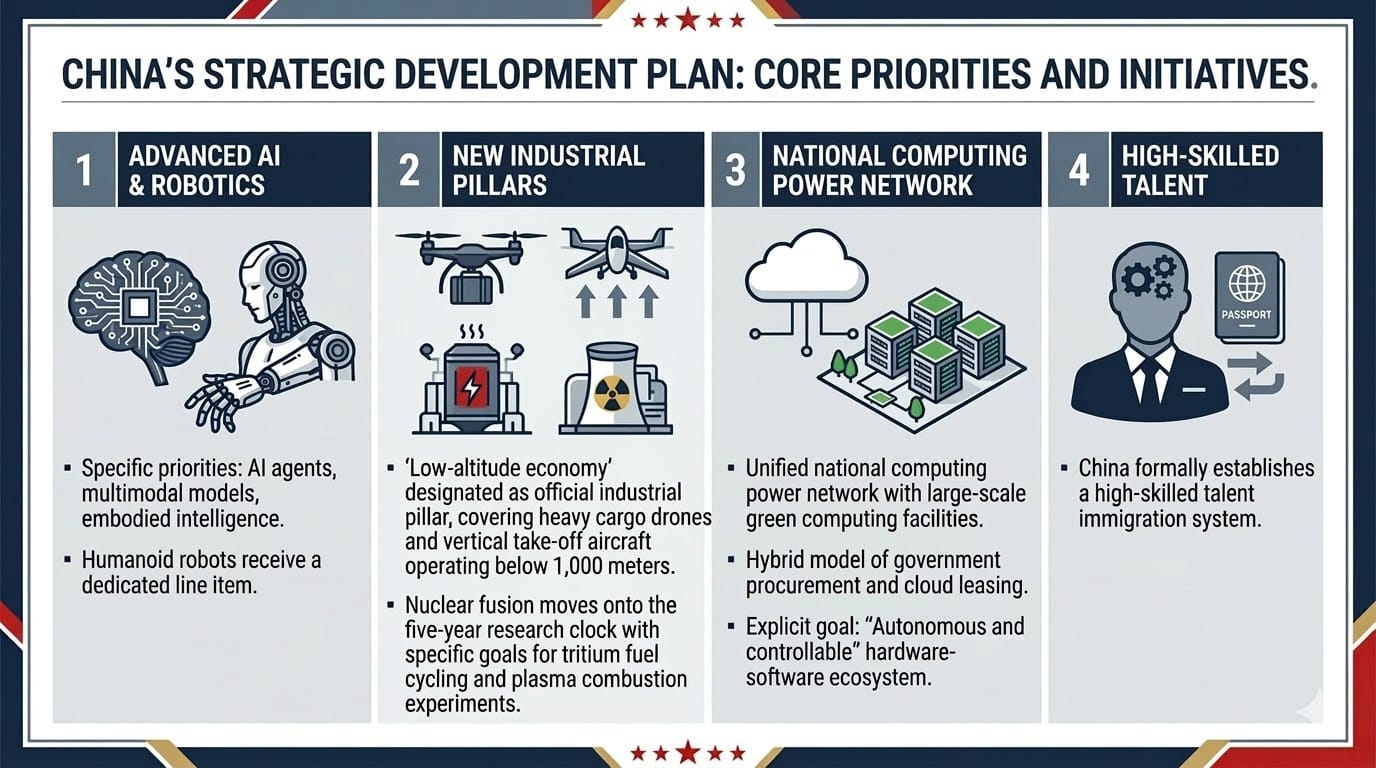

Beijing’s Blueprint: China Puts AGI, Talent Immigration, and Computing-as-Utility in Its Next Five-Year Plan

China’s 15th Five-Year Plan names artificial general intelligence for the first time, establishes a high-skilled talent immigration system, and treats computing power as a public utility. This is an operational roadmap for a country with a track record of execution.

BRIEFING: China released the draft of its 15th Five-Year Plan on March 5 during the National People’s Congress. The 141-page document names artificial general intelligence (AGI) as an explicit research target for the first time and mentions “AI” 51 times. Specific priorities include AI agents, multimodal models, and embodied intelligence. Humanoid robots receive a dedicated line item, upgraded from the previous plan’s general manufacturing category. The plan designates the “low-altitude economy” as an official industrial pillar, covering heavy cargo drones and vertical take-off aircraft operating below 1,000 meters. Nuclear fusion moves onto the five-year research clock.

Two structural shifts stand out. First, computing power is reframed as a public utility. The plan calls for a unified national computing power network with large-scale green computing facilities, a hybrid model of government procurement and cloud leasing, as well as an explicit goal of an “autonomous and controllable” hardware-software ecosystem. Second, China formally establishes a high-skilled talent immigration system. The 14th Plan tentatively mentioned “exploring” such a system, but the 15th drops the hedging. For a country that has historically made permanent residency difficult, this represents a direct entry into the global talent competition. The plan also grants leading technology companies formal ownership over research and development decisions and seats them at the table when national science policy is made, a notable departure from China’s traditional top-down governance of research.

SO WHAT FOR LEADERS: Treat this document as an operational roadmap, not propaganda. China’s previous Five-Year Plans have a strong track record of execution on strategic technology commitments. Three elements demand particular attention. First, the compute-as-utility framework means Chinese companies and researchers will access state-subsidized AI infrastructure at a scale and cost that private Western competitors cannot match without equivalent policy support. If your AI strategy assumes that compute costs remain a competitive differentiator, pressure-test that assumption against a state-backed compute grid. Second, the talent immigration system targets the same researchers and engineers that Western firms recruit. Assess whether your compensation, visa sponsorship, and retention packages remain competitive against a country that just removed one of its biggest barriers to foreign talent. (This is especially pertinent and urgent given unstrategic restrictions on H1B visas in the U.S.) Finally, the “AI+” strategy of embedding artificial intelligence into manufacturing, healthcare, education, and government services describes a deployment velocity that most Western companies have not yet achieved. Map your sector against Beijing’s named priority verticals and determine where Chinese state-backed competitors will arrive first.

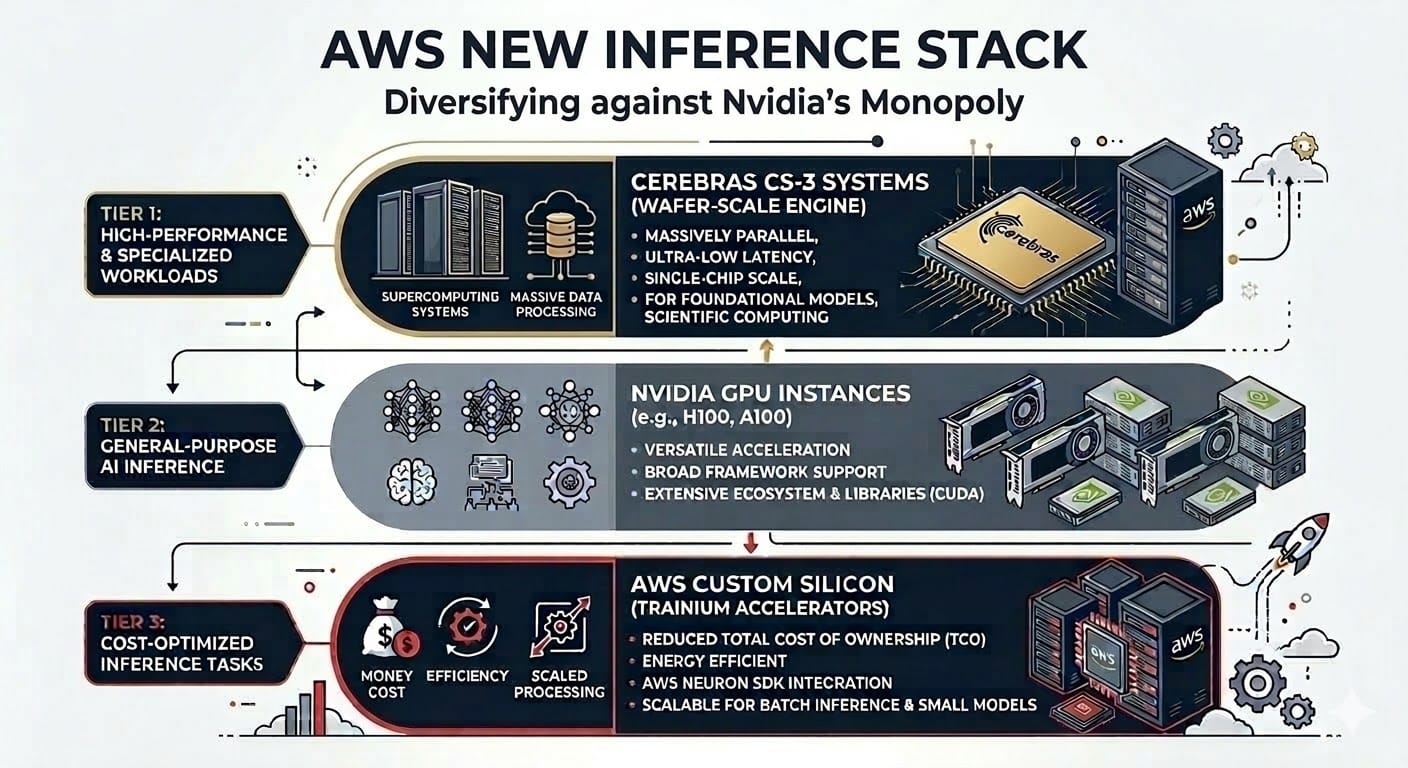

The Compute Schism: AWS Bets on Cerebras and Breaks Nvidia’s Lock on AI Infrastructure

Amazon Web Services will deploy Cerebras’ Wafer-Scale Engine for AI inference, the first time a major hyperscaler has adopted a non-Nvidia architecture for production AI workloads at scale. The chip monopoly might be starting to fragment.

BRIEFING: AWS announced it will deploy Cerebras’ Wafer-Scale Engine chip for AI inference functions across its cloud infrastructure. The Cerebras chip, a single silicon wafer roughly the size of a dinner plate, processes AI workloads using a fundamentally different architecture than Nvidia’s GPU-based approach. AWS will continue offering its own Trainium processors for slower, cheaper computing, creating a three-tier inference stack: Cerebras for high-performance workloads, Nvidia GPUs for general-purpose AI, and Trainium for cost-optimized tasks.

Nvidia currently controls roughly 80 percent of the AI chip market. Every major government AI strategy, from the U.S. CHIPS Act to China’s Fifteen-Year Plan to Gulf sovereign compute programs, depends on access to Nvidia’s hardware. That concentration has given Nvidia extraordinary pricing power and made its export status a frontline instrument of U.S. foreign policy. The AWS-Cerebras partnership does not replace Nvidia overnight, but it establishes a production-grade alternative at hyperscale for the first time. Cerebras has previously deployed systems with the Department of Energy and several pharmaceutical companies, but an AWS deployment puts its architecture in the hands of millions of cloud customers who previously had no practical alternative to Nvidia silicon.

SO WHAT FOR LEADERS: For AI infrastructure planners, this changes the negotiation. Nvidia’s pricing power has rested on the absence of credible alternatives at scale. A three-tier inference stack from the world’s largest cloud provider gives procurement teams a lever they have not had. Benchmark your workloads against the new options and use the results to renegotiate your GPU commitments. Nvidia’s strongest defense is not the hardware itself but CUDA, its proprietary software platform that most AI developers have built their code on. Switching chips means rewriting software, and that friction is real. The AWS move chips away at the hardware lock-in, but the software lock-in persists for now.

For sovereign compute strategists, diversification within the U.S. chip ecosystem does not weaken Washington’s export control leverage. Cerebras is also an American company, subject to the same Bureau of Industry and Security rules as Nvidia. What changes is that the U.S. semiconductor sector as a whole gains depth: more chip architectures, more suppliers, more resilience against single points of failure. Countries building national AI infrastructure should welcome the optionality but should not mistake it for an escape from U.S. technology dependencies. For investors, watch how quickly other hyperscalers follow. If Microsoft Azure or Google Cloud announce similar non-Nvidia partnerships in the next two quarters, Nvidia’s margin assumptions need revision.

The Drone Supply Chain Reckoning: Ukraine Builds China-Free, but the World’s Drone Arsenal Still Runs on Chinese Parts

Ukraine achieved a milestone when it built drones with no Chinese components. Mass production at that standard remains years away, however, and the entire global drone supply chain, from Kyiv to the Pentagon, still traces back to the same Chinese factories.

BRIEFING: Ukraine can now produce drones with zero imported Chinese components, according to a March 11 New York Times report. The company F-Drones went from a 100 percent Chinese supply chain in 2023 to near-full domestic production in just two years, localizing carbon frames, antennas, flight controllers, speed controllers, radio modems, and video transmission systems. Major Robert “Magyar” Brovdi, commander of Ukraine’s Unmanned Systems Forces, told the Times that drones account for more than 90 percent of Russian battlefield losses. Ukraine plans to produce more than 7 million drones in 2026. Two Ukrainian companies producing drones without Chinese components were selected to compete for contracts under the Pentagon’s $1.1 billion Drone Dominance Program.

The milestone is real but narrow. Ukrainian officials acknowledge that mass production of China-free drones remains years away because Chinese components are significantly cheaper. Many parts manufactured outside China still contain Chinese-sourced materials further up the supply chain. A CSIS analysis identified four critical chokepoints where Chinese manufacturing dominates global drone production: carbon fiber composites, rare-earth magnets for motors, lithium-ion battery cells, and gallium-nitride chips. Roughly 90 percent of the types of magnets essential for drone motors are produced in China. Both sides of the Ukraine conflict draw from the same Chinese component ecosystem. China shipped 328,000 miles of fiber-optic drone cable to Russia while restricting component access for Ukraine and its allies. NATO designated China a “decisive enabler” of Russia’s war in July 2025.

SO WHAT FOR LEADERS: Ukraine’s experience is a preview of what every country building a drone industrial base will face. Replacing a finished drone is straightforward. Replacing the component ecosystem behind it requires years of capital investment in materials science, precision manufacturing, and supply chain development that most Western countries have not started. The Pentagon’s Drone Dominance Program and Brave1’s U.S. venture capital roadshow this month signal that Washington recognizes the gap, but the scale is daunting: Ukraine consumed 20 million drone motors in 2025 alone, and European production cannot cover even a few months of that demand.

Defense procurement leaders should map their drone supply chains below the tier-one contractor level. A “Made in America” or “Made in Europe” label means nothing if motor magnets, battery foils, or camera sensors originate in China. The companies that secure non-Chinese sources of rare-earth magnets, lithium-ion cells, and gallium-nitride semiconductors will own the next generation of drone production capacity. For investors, follow the Ukrainian model: the firms that localized fastest under wartime pressure are now competing for NATO contracts worth billions.

The opportunity extends beyond defense. Drone components overlap heavily with civilian applications in agriculture, logistics, inspection, and emergency response. As the non-Chinese component ecosystem matures under defense-driven demand, civilian product supply chain managers and ecosystem strategists should track which new suppliers emerge and at what price points. The same motors, sensors, and battery cells that go into military drones power commercial fleets. Western innovators who invest now in alternative component manufacturing will serve both markets as they scale.

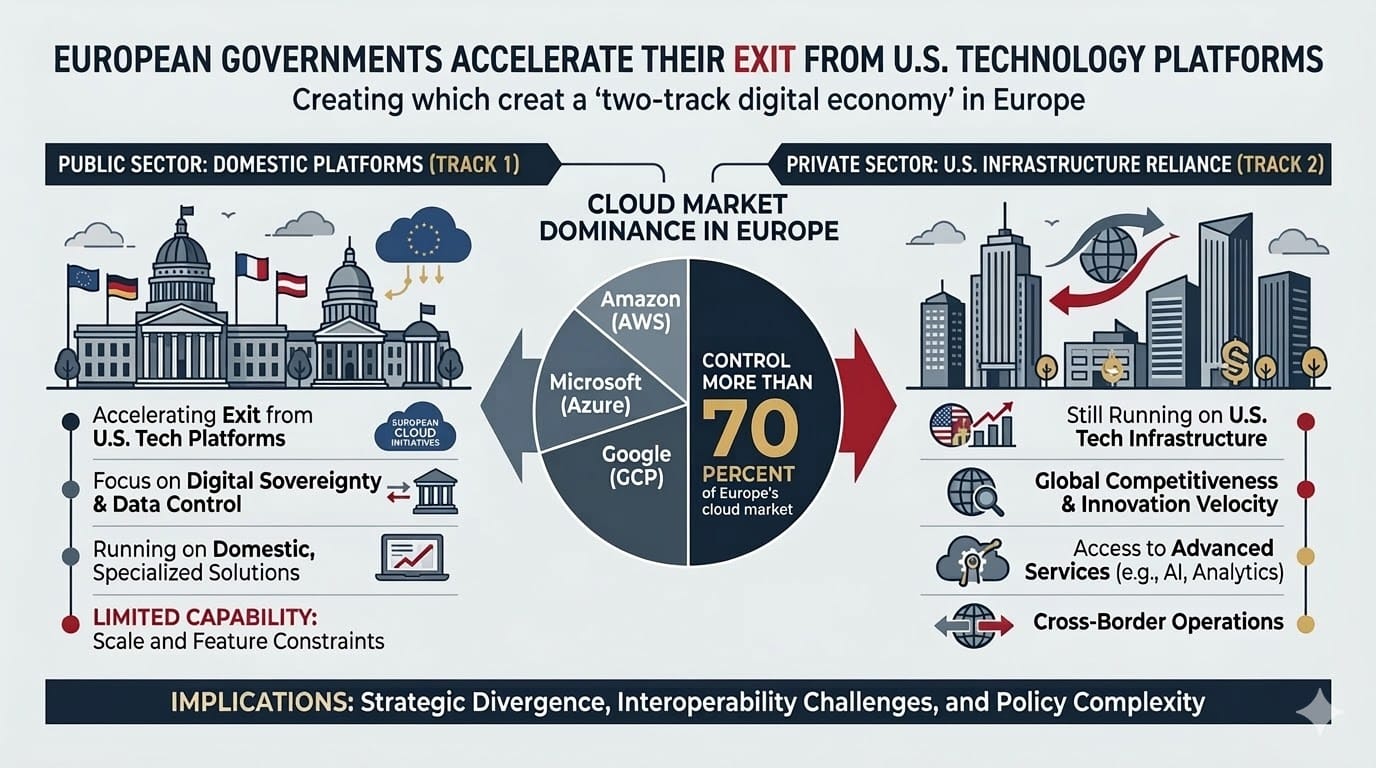

Europe’s Two-Track Trap: Governments Decouple from U.S. Tech While Their Own Companies Say They Can’t

France ordered 2.5 million civil servants off Microsoft Teams. Austria’s military migrated to LibreOffice. But Europe’s banks, manufacturers, and infrastructure operators warn the sovereignty push could damage competitiveness more than the dependency it aims to fix.

BRIEFING: European governments are accelerating their exit from U.S. technology platforms. France gave all ministries until 2027 to transition 2.5 million civil servants away from Zoom and Microsoft Teams to Visio, a French-built videoconferencing platform. Austria’s armed forces migrated 16,000 workstations from Microsoft Office to LibreOffice. Germany’s Schleswig-Holstein region is moving its entire state administration off Microsoft products. All 27 EU member states signed a declaration in November committing to “strengthen Europe’s digital sovereignty.” The European Commission plans to unveil a “tech sovereignty package” next month. Gartner projects that spending on sovereign cloud infrastructure in Europe will more than triple to $23 billion by 2027.

The business community is pushing back. Executives at ASML, Ericsson, and Capgemini cautioned against protectionist reflexes that could raise costs and slow investment. Deutsche Bank warned that the financial sector’s reliance on a small number of global cloud providers creates concentration risk but said the alternatives are not ready. Erste Group’s chief operating officer said the idea that a global provider would stop serving Europe once seemed unthinkable but “is more realistic today.” Amazon, Microsoft, and Google control more than 70 percent of Europe’s cloud market. European banks flagged the risk that U.S. providers could be forced to cut off service through sanctions or export controls, pointing to the 2025 episode in which Microsoft suspended the email account of the International Criminal Court’s chief prosecutor after U.S. sanctions were imposed.

SO WHAT FOR LEADERS: The danger is not the dependency itself. The danger is the fracture between government procurement mandates and the operational reality facing European businesses. European governments are decoupling at speed. European companies are locked into contracts, workflows, and technical architectures that cannot be unwound without multiyear migration programs and significant cost. That gap creates a two-track digital economy: a public sector running on domestic platforms with limited capability, and a commercial sector still running on U.S. infrastructure with growing regulatory exposure. If your organization operates in Europe, you face both tracks simultaneously.

Map where your European operations depend on U.S. cloud providers for regulated workloads, sovereign data, or critical infrastructure. Identify which contracts are vulnerable to a policy change that restricts U.S. provider access, and then build contingency plans for those workloads specifically rather than attempting a wholesale migration. For U.S. technology companies selling into Europe, the sovereign cloud market is a growth opportunity if you offer local hosting, systems that operate independently without connection to external networks, and contractual assurances that satisfy the new procurement rules. Look into the Digital Embassies concept, which would carve out sovereign territory on U.S. hyperscaler servers. For European technology firms, the window to compete for these government contracts is open now.

Under the Radar

The deep analysis that connects the dots

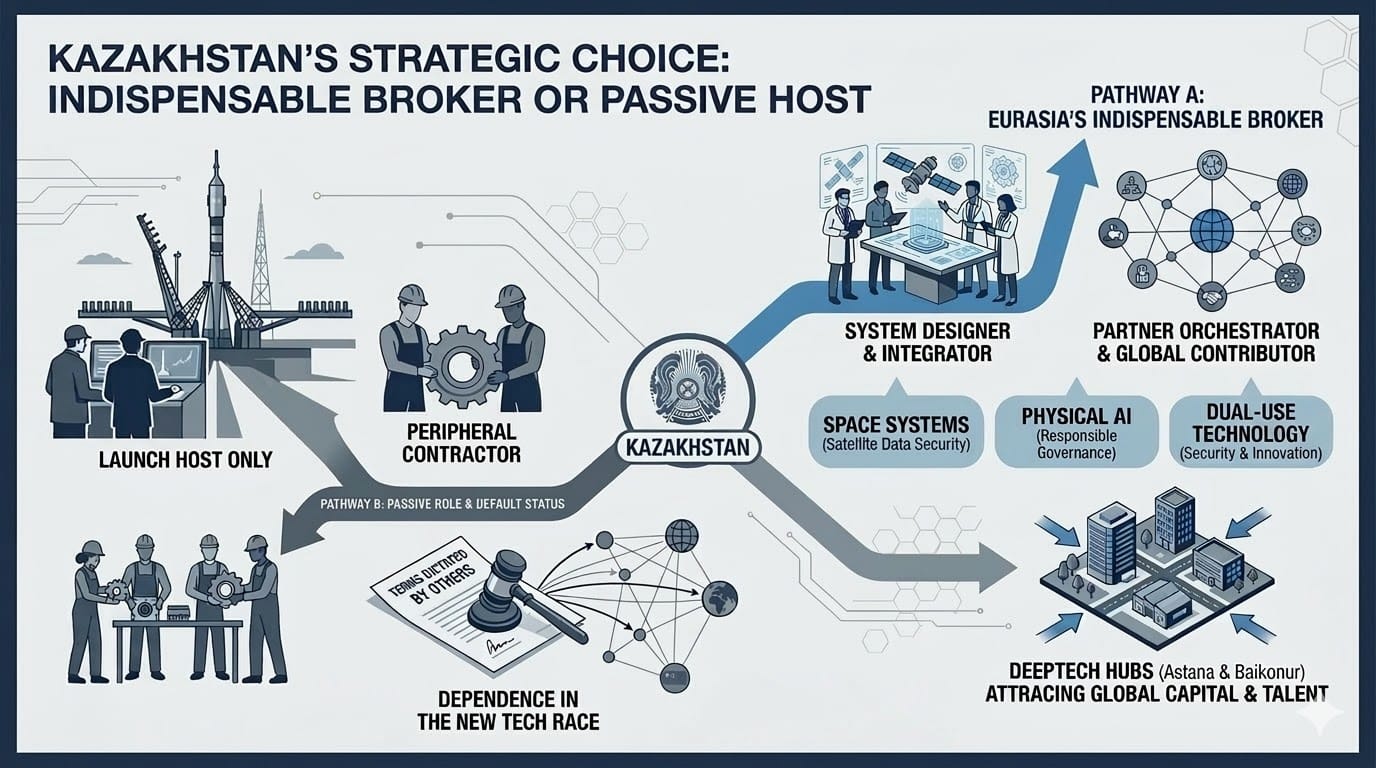

The Eurasian Broker: Kazakhstan’s Window to Become a GeoTech Orchestrator in SpaceTech Is Now Wide-Open

Kazakhstan can either become Eurasia’s indispensable broker of space, AI, and advanced technology, or it becomes a pawn in a competition it does not control. The choice is being made now.

Kazakhstan sits at the intersection of Russian legacy infrastructure, Chinese scaling power, European governance frameworks, and American technology platforms. It hosts the Baikonur Cosmodrome. It created a Ministry of Artificial Intelligence and Digital Development. President Tokayev established an AI Development Council staffed with international experts, including Cambrian Futures CEO Olaf Groth. In a SpaceNews op-ed published March 13, Groth and Kazakhstan’s Deputy Prime Minister and Minister of AI & Space Zhaslan Madiyev argued that the country faces a strategic choice for space technologies. It can either build itself into Eurasia’s indispensable technology broker for compute and space tech, or default to a passive role where others dictate terms in the new race on both fronts.

The broker path would transform Kazakhstan from a launch host into a system designer and partner orchestrator, with its engineers and scientists contributing to global missions and supply chains rather than serving as peripheral contractors. The country could convene forums on dual-use technology governance, satellite data security, and responsible Physical AI in space systems. Deeptech hubs linked to Baikonur and Astana could attract global capital and talent, positioning space as an innovation catalyst across the economy. But the dependencies are real. Historical ties with Russia’s scientific community must be maintained, and Russia’s cultural and educational legacy needs to be respected given its proximity and the Russian minority in the country. China’s supply chain position and proximity also make it indispensable for trade. Europe serves as a governance anchor, science and education partner. The U.S. is still the dominant force on AI and SpaceTech innovation, entrepreneurship, and capital. The Gulf States and Israel offer important technological and educational opportunity horizons. Navigating all of these relationships without becoming captured by any one of them requires institutional reforms and strategic investments that Kazakhstan has discussed but not yet fully committed to. Governance and technocracy agility are both key to this, as is capital market liberalization and trust assurance to bring funding to Kazakhstan’s commercial sector. The country has global governance credibility based on its adherence to global nuclear non-proliferation regimes, and it appears willing to take leadership roles beyond the region via its participation in Abraham Accords and Peace Board.

THE GEOTECH SIGNAL

Kazakhstan’s dilemma is a template for every mid-tier country positioned between major GeoTech blocs. The question is whether you shape the terms of education, science and technology, and capital cooperation in your region toward local value-add and capacity building. The alternative is to accept whatever terms the larger powers impose and become an extraction hub. For executives with operations in the Gulf or Southeast Asia, watch Kazakhstan closely as a compute, space innovation, and launch gateway to Central Asia. If it succeeds in building a credible broker model with trusted data corridors, dual-use governance frameworks, and neutral convening power, it creates a replicable playbook. If it stalls, the vacuum will be filled by players with less interest in neutrality. Companies operating in Eurasia should engage with Kazakhstan’s AI Council, investment board, and space cluster now, while the architecture is still being designed, rather than waiting for the rules to be written without their input.

Cambrian Partner By Invitation

Expert analysis from our global network

The Race To Turn Infrastructure Into Intelligence

Last week at the GPU Technology Conference (GTC), Nvidia CEO Jensen Huang declared that "every industrial company will become a robotics company" and unveiled new platforms for deploying physical AI at production scale. ABB, FANUC, KUKA, and more than a dozen humanoid robot firms announced they are building on Nvidia's technology to embed intelligence into factories, logistics networks, and surgical suites. The implication is clear: physical AI is no longer a research concept. But the path to getting there does not always require new hardware.

Until recently, adopting physical AI required significant investments in new hardware, sensors, and infrastructure. Today, that barrier is falling. Advances in software, edge computing, and cloud-based AI now enable organizations to transform existing devices, especially cameras, into intelligent sensing systems without costly upgrades. This shift is unlocking new value from infrastructure that has long been underutilized.

Traditionally, cameras in enterprise and public environments have served primarily as security tools. With spatial intelligence, they can now provide real-time operational insights. Organizations can query video feeds to understand patterns such as foot traffic, queue lengths, dwell times, and resource utilization, enabling faster, data-driven decision-making.

Airports offer a compelling case study. With hundreds or even thousands of cameras already deployed, they can now gain end-to-end visibility into the passenger journey from curb to gate. Insights into wait times, congestion points, and operational bottlenecks allow airport leaders to optimize staffing, improve throughput, and enhance the passenger experience, all while reducing manual data collection.

For leaders, the imperative is clear: start by assessing existing infrastructure, prioritize high-impact use cases, and invest in capabilities that augment—not replace—what you already have. Those who act early will turn their environments into intelligent systems and gain a meaningful operational advantage.

About Professor Jonathan Reichental

Dr. Jonathan Reichental is a multiple-award-winning technology leader and educator, whose career spans the private, public, and academic sectors. He's been a senior software engineering manager, a director of technology innovation, and has served as chief information officer (CIO) at both O'Reilly Media and the City of Palo Alto, California. Reichental is currently the founder of advisory, investment, and education firm, Human Future, and also creates online education for LinkedIn Learning and Coursera. In academia he is a professor at the University of San Francisco and several other universities and colleges. He has a regular column in Forbes and has written many books including Smart Cities for Dummies, Exploring Smart Cities Activity Book for Kids, and Data Governance for Dummies. He is a member the Cambrian Futures Network. You can reach him on LinkedIn: https://www.linkedin.com/in/reichental/

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 10'