The $650 Billion Infrastructure Gamble, Starlink's Battlefield Kill Switch, Southeast Asia's AI Archipelago

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

The leadership challenge in the AI era is not about mastering tools, it’s about mastering context. This issue is a case study in how fast that context is shifting. Crypto markets now move on tariff threats, not technology. Nuclear SMRs (small modular reactors) are being positioned as the only viable power source for AI’s energy resilience, notwithstanding big questions around maturity. Starlink has crossed the line from neutral infrastructure to active battlefield instrument. Compute is fragmenting into regional “AI archipelagos” rather than consolidating globally. NATO is mobilizing to defend undersea cables as critical strategic assets. None of these are incremental changes. Together, they signal a phase shift in how digital systems intersect with power, security, and statecraft. Leaders who still treat these as separate domains are already behind.

That is why the World Economic Forum’s concept of digital embassies matters, especially for small and mid-sized economies (https://www.weforum.org/meetings/world-economic-forum-annual-meeting-2026/sessions/digital-embassies-for-sovereign-ai/). Mutual accords for data center and compute sharing – combined with joint governance and reconnaissance of threats and infractions – have become a necessary foundation for cognitive resilience. For countries without the scale to build fully sovereign AI stacks, the path to autonomy involves federated approaches that are anchored in shared values, legal interoperability, and mutual trust. Digital embassies would allow data, models, and governance to move together across borders under agreed rules. This logic is far less applicable to continental-scale powers like India, where internal diversity, market size, and strategic autonomy favor national architectures over federation. Sovereignty is not binary, it is contextual.

This concept addresses a fundamental asymmetry in AI development. Building domestic data center capacity takes years, and the legal, regulatory, and security obligations apply from day one. For the 150+ countries that cannot realistically build their own infrastructure networks fast enough, digital embassies offer a mechanism to access global AI capabilities while maintaining jurisdictional control over data, systems, and policies. The framework offered by UAE-based G42, for example, treats sovereign AI infrastructure like diplomatic territory, so a nation's data and compute capacity can operate anywhere while remaining under that nation's legal jurisdiction. Just this week, the Government of India said it had signed agreements with 23 countries for the sharing or cooperation on its India Stack Digital Public Infrastructure, a standardized protocol for digital identity, payments, and services that offers a parallel model focused on applications.

For multinationals, the implication is growing complexity in data governance when data physically hosted in one country might be legally governed by another's rules by design. This fragmentation demands new risk and opportunity frameworks built on continuous sensing, not static planning. Leaders need real-time visibility into policy shifts, infrastructure bottlenecks, energy security, capital flows, and geopolitical signals as they evolve. This is where the GeoTech SWAT teams we described in this WEF article (https://www.weforum.org/stories/2024/02/tech-geopolitics-strategic-capabilities-geotech-organizations/) become essential. These small, cross-functional units fuse intelligence, policy, technology, and operations to simulate and anticipate shocks, stress-test strategic choices, and translate geopolitical, societal, technological, and resource change into decisive action. In a world where context moves faster than institutions, system foresight becomes a core operating capability in every market.

On the Radar

The signals affecting the GeoTech landscape this week

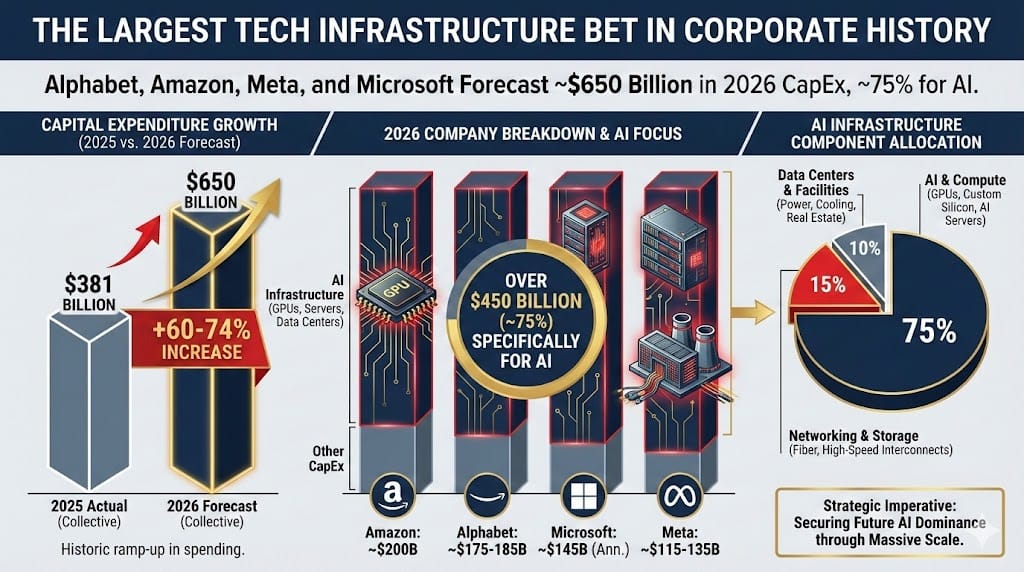

Big Tech’s $650 Billion Bet: Creative Destruction?

THE BRIEFING: GeoTech Radar has tracked the hyperscaler infrastructure race across multiple issues. This week, earnings season made it official. Alphabet, Amazon, Meta, and Microsoft each used their Q4 2025 earnings calls to confirm the $650 billion collective capex forecast we flagged previously. Amazon confirmed approximately $200 billion. Alphabet guided $175-185 billion. Microsoft annualized at $145 billion. Meta set a range of $115-135 billion. Roughly 75% is earmarked for AI infrastructure.

The market reaction was telling. Despite confirming historic spending levels, none of the four stocks dropped on the capex guidance, mainly because investors have already priced in the infrastructure bet. What they have not priced in is the financial strain now visible in the filings. Amazon projects negative free cash flow of $17 billion to $28 billion this year. Meta’s free cash flow is down 90% and expected to remain negative through 2028. These companies are increasingly turning to debt markets to bridge the gap, transforming historically cash-funded business models into leveraged operations. The question is no longer whether the money will be spent. It is whether the returns will justify what Goldman Sachs analysts are comparing to the 1990s telecom bubble.

SO-WHAT FOR LEADERS: With board-level commitments locked in, these capital flows are no longer speculative. Energy grids, water systems, and real estate markets in data center corridors will feel the impact for years. For companies dependent on cloud AI services, hyperscaler financial health is now a supply chain variable worth monitoring quarterly. The geographic distribution of these investments – which countries get data centers, which grids can support them – will shape sovereign AI capabilities globally. For investors, the simultaneous repricing of software stocks downward (see SaaSpocalypse, below) and infrastructure stocks upward suggests the market believes the AI value chain will concentrate at the physical layer. The comparison to historic bubbles warrants attention, too. The railroads and telecoms created lasting infrastructure even as they destroyed investor capital. The question is whether your organization is positioned as builder, beneficiary, or casualty of this transition.

Crypto’s Tariff Reckoning: Digital Assets as Geopolitical Casualties

THE BRIEFING: Bitcoin has dropped from its October 2025 peak of $127,000 to approximately $70,000 this week, a decline of more than 40% that wiped out the gains accumulated since Trump's re-election. The catalyst was Trump's October threat of 100% tariffs on Chinese imports, which triggered a broader risk-off move that hit crypto harder than any other asset class. Unlike equities, which recovered, crypto never bounced back. Institutional demand has reversed, with U.S. spot Bitcoin ETFs suffering outflows exceeding $12 billion since November. Trading volumes have collapsed, liquidity has evaporated, and analysts at Deutsche Bank and CryptoQuant are calling this a full "crypto winter."

The irony is acute. Trump campaigned on making America "the crypto capital of the world" and delivered major legislative wins, including the GENIUS Act. Yet his January tariff threats against eight European nations over Greenland triggered $875 million in liquidations within 24 hours. The China tariff threat issued in October produced $19 billion in forced closes across exchanges in a single day. Crypto's supposed independence from traditional finance has proven illusory so far. It trades as a high-beta risk asset, amplifying rather than hedging geopolitical volatility.

SO-WHAT FOR LEADERS: Whether this proves to be a full crypto winter or a sharp correction that recovers, the episode exposes the gap between crypto’s narrative (i.e. digital gold, inflation hedge, uncorrelated asset) and its reality (i.e. speculative vehicle highly sensitive to macro conditions). For GeoTech analysis, the lesson is that digital assets remain tethered to physical-world politics. Tariff threats move crypto more than blockchain developments. Trade negotiations determine whether institutional capital flows in or out. The integration of crypto into traditional finance through ETFs has made it more, not less, vulnerable to geopolitical shocks. Nations and corporations considering crypto as a strategic asset should recognize it as a proxy for risk appetite, not a hedge against uncertainty. Companies with crypto treasury holdings face material valuation risk tied to trade policy volatility. The U.S.-India trade deal announced this week triggered a partial recovery, demonstrating that diplomatic developments are now as likely to move crypto markets as any technical factor. Corporate treasury and risk teams should model crypto exposure against geopolitical scenarios, not just market conditions.

Starlink's Battlefield Kill Switch: When Private Infrastructure Gets Weaponized

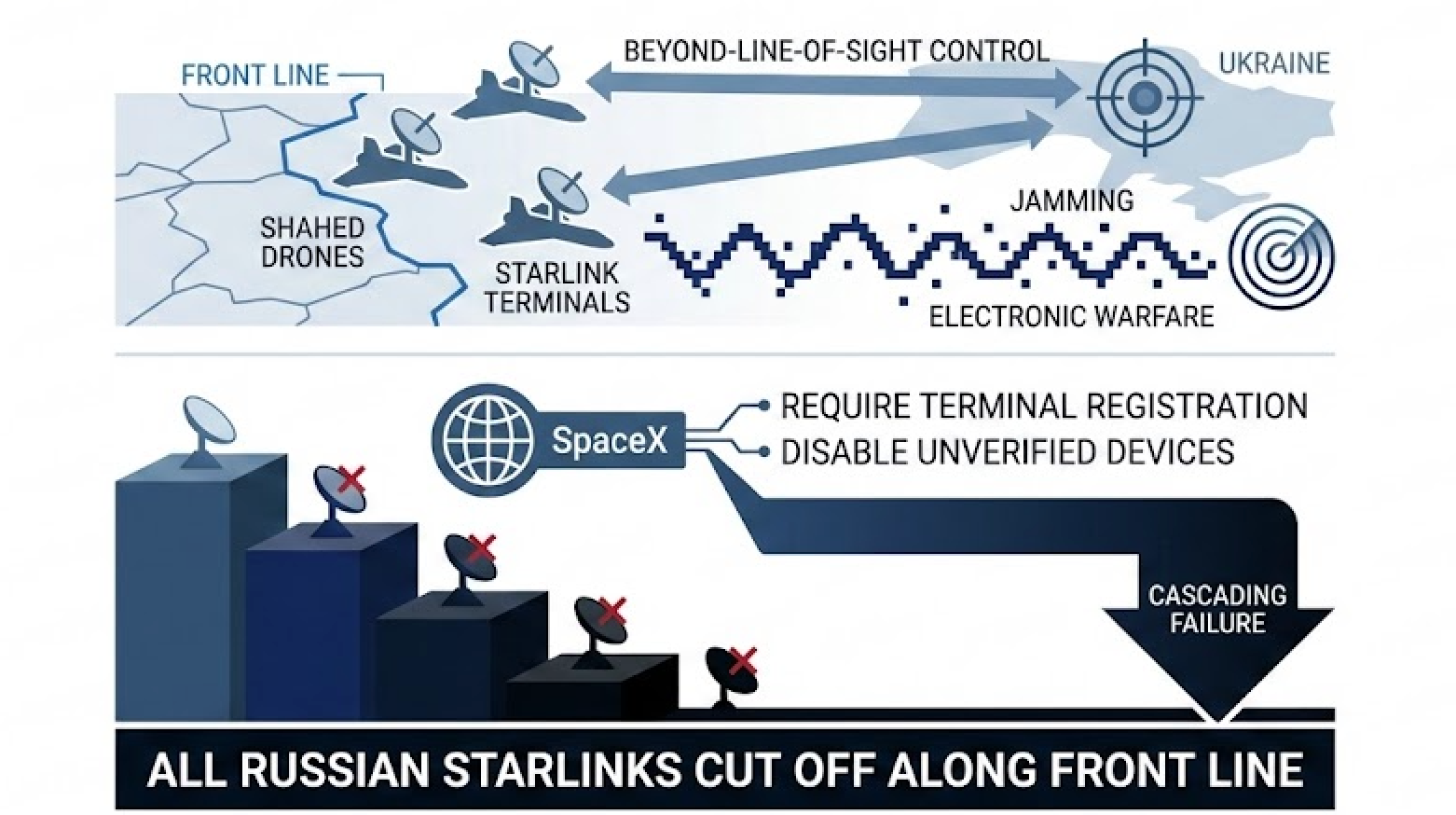

THE BRIEFING: SpaceX has implemented a "whitelist" system that cut off Russian military access to Starlink terminals in Ukraine, producing what Ukrainian officials describe as a "catastrophe" for Russian command and control. Ukrainian Defense Minister Mykhailo Fedorov announced this week that the company worked with Kyiv to block unauthorized terminals, with "real results" visible within days. A source at the Ukrainian General Staff claimed "all Russian Starlinks have been cut off" along the front line. Russian military bloggers confirmed the disruption, with one noting "all command and control of the troops has collapsed" and "assault operations have been halted in many areas."

The crisis emerged after Ukrainian officials documented "hundreds" of Russian drone attacks using Starlink terminals for beyond-line-of-sight control, including a strike on a civilian train in eastern Ukraine. Russia had been mounting terminals on Shahed drones to bypass Ukrainian electronic warfare that jams GPS and radio signals. SpaceX responded by requiring terminal registration and disabling unverified devices. Elon Musk confirmed on X that "the steps we took to stop the unauthorized use of Starlink by Russia have worked." Russian propagandist Vladimir Solovyov responded by suggesting attacks on Starlink factories or satellites, underscoring how dependent Russian forces had become on infrastructure they do not control.

SO-WHAT FOR LEADERS: A private American company just made operational decisions with immediate battlefield consequences in an active armed conflict, all without government mandate, treaty obligation, or formal legal framework. SpaceX exercised power traditionally reserved for states, flexing its ability to enable or deny military communications across an entire theater of war. Commercial satellite providers are no longer passive infrastructure. They are actors whose technical decisions shape tactical outcomes. For military planners globally, this creates a new category of dependency risk. For investors, tech and communications solutions could go “dual use” in ways that suddenly impact ROI. For international governmental organizations, it exposes a governance vacuum in which private operators can deny service to combatants based on corporate policy rather than coherent national or international standards. Any organization dependent on commercial satellite connectivity now faces a demonstrated risk that access can be revoked based on geopolitical considerations. Companies should map their satellite dependencies and develop contingency plans for service denial. Demand for sovereign or ally-controlled alternatives to commercial low-earth orbit (LEO) constellations will increase.

AI's Nuclear Renaissance: Big Tech Risky Bets on Atoms For Electrons

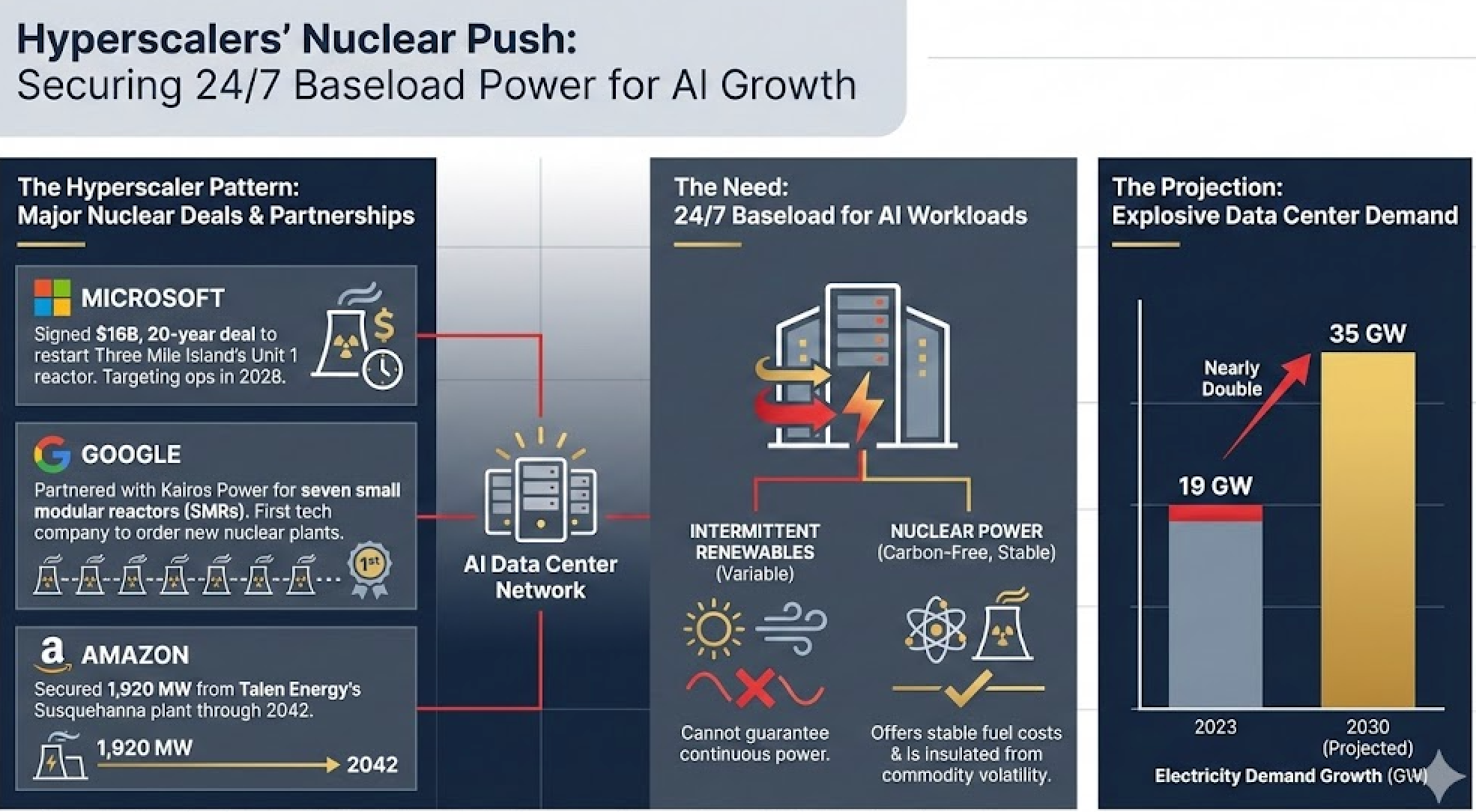

THE BRIEFING: Meta has emerged as one of the world’s largest corporate buyers of nuclear power, signing deals in January that could deliver more than 6.6 GW of electricity by 2035, enough to power approximately 5 million homes. The agreements with Vistra, TerraPower (backed by Bill Gates), and Oklo (backed by OpenAI’s Sam Altman) will support Meta’s Prometheus AI supercluster in Ohio, expected online this year, and the larger 5 GW Hyperion facility in Louisiana targeted for 2028.

Meta’s nuclear push follows a pattern across hyperscalers. Microsoft signed a $16 billion, 20-year deal to restart Three Mile Island’s Unit 1 reactor, aiming to start operations in 2028. Google partnered with Kairos Power to commission seven small modular reactors (SMRs), the first targeted for 2030. Amazon secured 1,920 MW from Talen Energy’s Susquehanna plant through 2042. It’s critical to note, however, that most of these projects remain years from operational status. No SMR is yet operational in the United States. NuScale holds the only NRC-approved SMR design, with deployment targeted for 2030. TerraPower’s Natrium demonstration reactor in Wyoming is under construction with a 2030 target. Kairos’s Hermes test reactor in Oak Ridge, Tennessee, could operate as early as 2026, but its commercial units will not arrive until the 2030s. China’s Linglong One, the first commercial onshore SMR, is expected to begin operations this year. Meanwhile, data center electricity demand is projected to nearly double from 19 GW in 2023 to 35 GW by 2030.

Bloomberg analysts estimate nuclear power costs Meta $141 to $220 per megawatt hour, compared to $50 to $60 for gas, wind, or solar. So why pay 3x-4x market rates? AI data centers require 24/7 baseload power that intermittent renewables cannot guarantee, and nuclear power offers carbon-free electricity with stable fuel costs insulated from commodity volatility.

SO-WHAT FOR LEADERS: Nuclear power’s resurgent appeal illustrates that electrons constitute as binding a constraint on AI development as algorithms and chips do. The hyperscalers’ willingness to pay premium rates signals that energy security, not just cost, drives infrastructure decisions. But this renaissance carries significant uncertainties. Public opinion remains divided on nuclear safety, and the projected cost per MWh for SMRs remains unproven at scale. If SMR performance disappoints in early deployments, the entire technology roadmap could slip. Watch closely for early performance data from Kairos’s Hermes reactor and China’s Linglong One. These will be the first real-world benchmarks for whether SMRs can deliver on cost, reliability, and safety. The broader energy price impact matters, too. Nuclear deals by hyperscalers are already tightening available grid capacity, with the PJM Interconnection’s independent market monitor filing emergency complaints about data center loads overwhelming regional grids. For enterprises planning AI infrastructure, nuclear-adjacent locations could offer more reliable power access, but only if the reactors actually get built on schedule.

Southeast Asia's AI Archipelago: A New Compute Geography Takes Shape

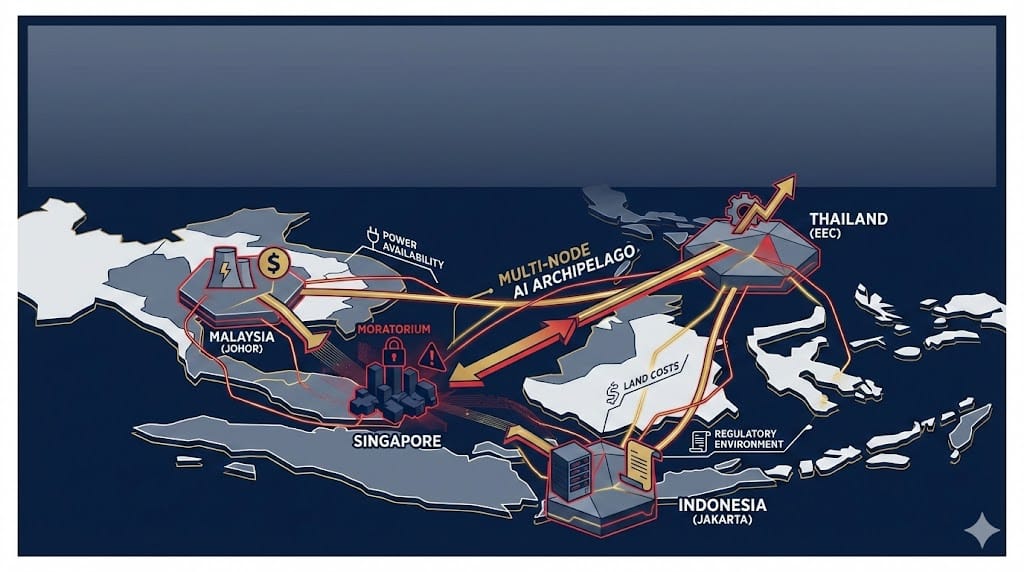

THE BRIEFING: Southeast Asia is emerging as a critical node in global AI infrastructure, with planned data center capacity in the region outstripping the current operational base by nearly four times. Malaysia leads the surge with approximately 4.8 GW in planned capacity, overtaking traditionally dominant Singapore, which is constrained by limited land, tight regulations, and data center moratoriums. Thailand is positioned to surpass Indonesia in planned capacity between 2026 and 2031, with a pipeline reaching 2.87 GW (nearly 3.7 times Indonesia’s total). The Thailand Board of Investment approved $3.1 billion in data center investments in a single batch, including the 84 MW DAMAC Digital facility and 200 MW Zenith hyperscale campus.

The hyperscaler commitments in the region are impressive, too. AWS has pledged $6 billion in Malaysia and $5 billion in Thailand. Microsoft is investing $2.2 billion in Malaysia, $1.7 billion in Indonesia, and selected Thailand for its lead regional data center. Google has earmarked $1 billion for Thailand and in January launched an initiative to develop a local cloud region around Bangkok. Chinese players are equally aggressive. ByteDance committed $8.8 billion for regional data center development, with its subsidiary TikTok investing $3.8 billion in Thailand alone. GDS Holdings’ overseas unit DayOne and Bridge Data Centers (part of China’s Chindata Group) operate multiple hyperscale facilities across Malaysia. China’s Galaxy Data Center announced a $2 billion investment in Thailand’s Eastern Economic Corridor. The Southeast Asian data center market, valued at $13.71 billion in 2024, is projected to more than double to $30.47 billion by 2030. By that date, Asia-Pacific data center capacity is expected to account for 40% of the global total, fueled by some $800 billion in investments.

Singapore’s constraints are pushing hyperscalers into Malaysia’s Johor state, Thailand’s Eastern Economic Corridor, and Indonesia’s Jakarta metro. This creates a multi-node “AI archipelago” where compute capacity is distributed across national boundaries based on power availability, land costs, and regulatory environment. In practice, this means data centers in Malaysia’s Johor serve workloads for Singapore-based enterprises. Thailand is becoming a processing hub for demand across mainland Southeast Asia, including Vietnam and Cambodia. Chinese-owned data centers in Vietnam now represent one of the largest concentrations outside mainland China, drawing international scrutiny over compliance with technology regulations and semiconductor handling. Vietnam’s 2026 Party Congress resolution made the shift explicit, targeting 10% annual GDP growth anchored in AI and semiconductors. Data sovereignty rules are fragmenting what was once a Singapore-centric regional architecture.

SO-WHAT FOR LEADERS: Companies planning AI infrastructure in Asia face a more complex decision matrix than "pick Singapore." Thailand offers tax incentives (e.g. eight-year corporate income tax exemptions), power availability, and government support for AI workloads. Malaysia provides scale and proximity to Singapore's subsea cable ecosystem through the Johor-Singapore Special Economic Zone. Indonesia offers reach into the world's fourth-largest population. Execution risks still could emerge from power grid readiness, contractor capacity, regulatory uncertainty, and other constraints. Supply could still lag demand by 15-25 GW by 2028, despite rapid expansion. For enterprises, the strategic question is whether to consolidate or distribute across the emerging archipelago for cost, resilience, and sovereignty benefits.

Sources: CBRE, Light Reading, Data Center Knowledge, Turner & Townsend, FTI Consulting, Research and Markets

The SaaSpocalypse: AI Disrupts Its Own Creators

THE BRIEFING: Enterprise software stocks have entered a bear market as investors reprice the sector for an AI-dominated future. The industry's average forward P/E ratio has plummeted from 39x eight months ago to roughly 21x today, the largest four-month valuation compression since the lingering fallout of the dot-com bust in the early 2000s. Jefferies traders have dubbed it the "SaaSpocalypse." ServiceNow is down 28% year-to-date despite beating earnings for nine consecutive quarters. Salesforce has fallen 26%. Intuit has lost more than 34%. The IGV software ETF is down 22% from its highs, with January 29 marking the worst single day for software since the COVID crash.

The trigger was Anthropic's release of Claude Cowork in January 2026, a productivity tool that sent legal software and publishing stocks tumbling. Thomson Reuters plunged 16%. London Stock Exchange Group fell 13%. LegalZoom dropped 20%. The pattern has repeated across sectors as investors realize that AI doesn't just enhance software, it can replace it. The historical link between corporate headcount and software spend is breaking. If AI agents can do the work of multiple humans, companies need fewer seats. Meta is spending $135 billion on AI capex this year. That money is coming from enterprise software budgets. "App fatigue is real," said SaaStr founder Jason Lemkin. "CIOs are consolidating, not expanding."

Not everyone thinks the SaaSpocalypse narrative holds up. Geoffrey Moore, author of The Infinite Staircase and one of Silicon Valley’s most influential strategists, argues the market is confusing the points at which AI creates value and risk. Moore’s Core vs. Context framework draws a sharp distinction between enabling functions and mission critical contexts. For enabling functions, such as innovation, experimentation and process automation, AI is a genuine game-changer, Moore says. But for mission-critical contexts, such as the systems of record that enterprises depend on for compliance, auditability, and operational reliability, replacing proven SaaS platforms with custom AI-built alternatives would be “stupid” because mission-critical context requires reliability, consistency, and best practices refined across thousands of customers, Moore says. “What is mission-critical context for you is mission-critical core for SaaS vendors,” he writes. “Who do you think is going to recruit the better talent? Who is going to have the bigger budget?” The real AI opportunity in enterprise software is not replacement but augmentation, he says, overlaying conversational interfaces and agentic AI on top of proven workflows rather than rewriting them from scratch.

SO-WHAT FOR LEADERS: The SaaSpocalypse illustrates AI’s double-edged nature for the technology sector. Bank of America analysts call the selloff “internally inconsistent,” noting that if AI is powerful enough to destroy software companies, then it must be valuable enough to justify the infrastructure spending that markets are simultaneously rewarding. The real sorting mechanism is Moore’s distinction. SaaS companies serving mission-critical workflows with deep domain expertise and data moats will likely survive and integrate AI. Those selling generic productivity tools that AI can replicate face genuine existential risk. For enterprise buyers, the software budget reallocation is real, so expect vendors to become more aggressive on pricing and more desperate to demonstrate AI integration. Organizations should evaluate their software portfolio for AI disruption risk and their vendor relationships for financial stability.

Baltic Cable Wars: NATO's New Front Against Hybrid Threats

THE BRIEFING: The Baltic Sea has become the world's most contested zone for subsea infrastructure security. Since 2022, approximately 10 cables have been cut in the region, with seven incidents occurring between November 2024 and January 2025 alone. Finnish police have seized multiple vessels suspected of dragging anchors to sever telecommunications cables. The most recent incident on December 31, 2025, damaged a cable connecting Finland and Estonia. The detained vessel was found carrying sanctioned Russian steel. EU foreign affairs chief Kaja Kallas stated that "Europe's critical infrastructure remains at high risk of sabotage" and attributed the incidents to "Moscow's shadow fleet."

The attribution picture is contested. U.S. and European intelligence officials have told reporters that evidence, including intercepted communications, suggests the cable breaks were accidental, caused by inexperienced crews aboard poorly maintained vessels rather than directed sabotage. However, European officials maintain the pattern is suspicious. NATO has launched "Baltic Sentry," a new operation involving maritime patrols, aircraft, and naval drones to protect undersea infrastructure. The EU announced an action plan for cable security including new surveillance capabilities, repair capacity, and measures against Russia's shadow fleet. Sweden conducted military exercises practicing responses to covert sabotage missions.

SO-WHAT FOR LEADERS: Whether accidental or deliberate, the Baltic incidents expose the vulnerability of the physical infrastructure underlying digital connectivity. The Baltic states depend on a small number of submarine cables running through shallow Baltic waters to connect to the Western European internet backbone infrastructure in Scandinavia, Germany, and Poland. A concentrated attack could isolate these nations from Western digital networks. This vulnerability extends worldwide, with 95% of intercontinental data flows running through approximately 550 submarine cables. The incidents have prompted the most significant NATO response to infrastructure protection since the Nord Stream explosions. For companies with operations in the Baltic region, assess telecommunications redundancy and business continuity plans for cable disruptions. The incidents did not cause major service outages because carriers had redundant routes, but concentrated attacks could overwhelm backup capacity. The EU’s planned investments in cable resilience create infrastructure opportunities. Insurance

Building Leaders in the Age of AI: Why Human Judgment Still Matters

THE BRIEFING: AI will amplify, rather than replace, the need for distinctly human leadership capabilities, according to an article last month from McKinsey Global Managing Partner Bob Sternfels, WEF President Børge Brende, and McKinsey Senior Partner Daniel Pacthod. In the report, the authors identify three irreplaceable leadership functions – setting aspiration (defining purpose and vision that inspires commitment); exercising judgment (making decisions under uncertainty where data is incomplete); and fostering creativity (generating novel solutions to unprecedented challenges). These are areas where humans have an edge, they write. They require emotional intelligence, ethical reasoning, and the ability to inspire trust, qualities that AI cannot replicate.

The authors argue that AI's rise demands a fundamental shift in leadership philosophy, from command-and-control to context-setting. The best leaders will increasingly be those who set context and stay alert to shifts in context, rather than those who issue detailed directives. They advocate for breaking the "paper ceiling" that excludes talented individuals lacking traditional credentials, building cultures that embrace continuous learning, and practicing "servant leadership" that prioritizes team development over personal achievement. The piece emphasizes protecting time, energy, and attention as the scarcest resources in an AI-augmented workplace where information abundance can overwhelm decision-makers.

NVIDIA CEO Jensen Huang offered a strikingly complementary perspective in a recent interview on A Bit Personal with Jodi Shelton (Episode 1, Season 1). Asked who the smartest person he’s ever met is, Huang declined to answer, instead challenging the premise. “The definition of smart is someone who solves problems, technical. But I find that’s a commodity, and we’re about to prove that Artificial Intelligence is able to handle that part easiest.” He pointed to software programming: “Everyone thought that software programming was the ultimate smart profession. Look what is the first thing that AI is solving.” For Huang, the future of “smart” is someone who is technically astute but with human empathy, able to infer the “the unknowables” by seeing around corners with a combination of data, lived experience, and wisdom.

Under the Radar

The deep analysis that connects the dots

Africa's Race to Close the 300% Gap

Africa already processes $1.1 trillion in annual mobile money transactions, 65 percent of the global total, while internet adoption grows at twice the global average from a base of just 38 percent penetration. Indicators of the continent’s economic growth potential. Yet the infrastructure underpinning that activity remains lacking. Africa faces a stark digital infrastructure deficit. The continent hosts less than 1 MW of data center capacity per million people, compared with 88.5 MW in the Americas and 73.9 MW in Europe. A wave of hyperscaler investment is now racing to close that growing gap, driven by demographics, diversification strategy, and the realization that the world's fastest-growing digital market cannot remain dependent on infrastructure an ocean away.

The Deficit: Africa's extreme infrastructure shortage creates both vulnerability and opportunity. South Africa dominates with 70% of the continent’s capacity concentrated in 56 facilities, but Nigeria has 26 data centers that represent just 15% of capacity. Most African enterprises and governments depend on data centers in Europe or the Middle East, creating latency, sovereignty, and resilience challenges. The continent that will add more people than any other this century processes most of its data elsewhere.

The Investment Surge: Global players are moving to fill the void. Microsoft committed to training a million South Africans in AI by 2026 and invested almost $340 million in cloud infrastructure. Its $1 billion Kenya partnership with G42 will establish a 100 MW geothermal-powered data center. Google is expanding its Johannesburg cloud region while building support for 50+ African languages. Equinix committed $390 million over five years for expansion across Nigeria, South Africa, and East Africa. NVIDIA's $700 million partnership with Cassava Technologies is deploying GPU clusters for sovereign AI workloads. And the International Finance Corporation (IFC) invested $100 million in Raxio Group, a leading Sub-Saharan African data center platform, to support expansion across six countries.

The Binding Constraint: Power remains the limiting factor. Nigerian data center expert Ifetayo Agboola identifies "reliable and affordable power" as the single biggest bottleneck. Operators rely heavily on backup generators, directing resources toward electricity production rather than capacity expansion. Currency volatility compounds the challenge, with providers charging in hard currency as local economies fluctuate. Transmission infrastructure, not just generation, limits delivery to large facilities. These constraints explain why Africa's AI readiness is "rapidly rising but uneven, with pockets of excellence still challenged by power and infrastructure gaps."

The Strategic Logic: For hyperscalers, Africa offers compute geography diversification away from concentrated facilities in the U.S., Europe, and Asia. The continent's young population, projected to exceed 830 million working-age people by 2050, represents the fastest-growing market for digital services. Bringing AI workloads closer to users would reduce latency while keeping data under local regulatory oversight. South Africa's Teraco is building a 120 MW solar plant to power data centers with renewable energy. Morocco's Naver-NVIDIA-Nexus partnership is developing a 500 MW AI campus. If companies and governments can solve the power constraints, the investment surge in the projects above could help Africa leapfrog legacy infrastructure patterns.

What to Watch: Monitor power infrastructure investments and financial hedging trends alongside data center announcements, because the former determine whether the latter can scale. Track hyperscaler cloud region expansions as indicators of where enterprise AI workloads will localize. Watch sovereign AI initiatives, such as Morocco's "Maroc IA 2030" roadmap and South Africa's Draft National AI Strategy, both of which signal government priorities. The GITEX Africa conference in Marrakech this April will showcase the continent's ambitions. For companies seeking supply chain diversification or African market access, the infrastructure buildout creates partnership opportunities, but due diligence on power reliability and regulatory clarity remains essential.

Cambrian Partner By Invitation

Expert analysis from our global network

Beyond Ethics: Calling for 'Earth Alignment' as AI Growth Threatens to Overshoot Remaining Planetary Boundaries

On November 5, 2025, the Stockholm Resilience Centre released its landmark report, AI for a Planet Under Pressure, introducing the principle of "Earth Alignment". The report warns that without a fundamental shift to align AI development with the Earth's life-support systems, the technological revolution risks accelerating the very environmental crises it promises to solve. This isn't just a matter of ethics; it is a systemic necessity to ensure that AI does not further erode the "safe operating space" for humanity.

If you're stranded on an island with a stranger, you'd better team up if you want to survive.

Our island is Earth. And the "stranger" we're suddenly sharing it with is rapidly expanding, omnipresent AI. This genie is not going back in the bottle. At the same time, we face the urgent reality of the climate crisis and the need to reverse our overshoot of planetary boundaries.

Too often, AI sees sustainability as a constraint and sustainability sees AI as a threat. Rising energy and water demands fuel that tension: the International Energy Agency estimates data-center electricity consumption could hit 945 TWh by 2030, twice Germany's current usage. Bloomberg reported that 2/3 of new data centers since 2022 are in places with high water stress. And as the Geotech Radar noted on 5 February, water scarcity will increasingly dictate where new AI infrastructure can even be built.

It's time for these two strangers to finally talk. AI has a lot to offer. Initiatives like UNDP's Nature ID, the Hamburg Declaration on "AI for the Planet", the Coalition for Sustainable AI of UNEP/ITU and the Global Digital Compact highlight how AI can accelerate sustainable development rather than slow it down. The WEF has demanded AI strategies to integrate energy, water, minerals and biodiversity risks. The UN Secretary General has proposed an Independent International Scientific Panel on AI that aims to shed light into its global importance. Also OECD is doing good work on this topic.

Yet this is often a conversation about AI and about sustainability, but not a face-to-face dialogue between big tech and the global sustainability community.

Big Tech seems not to be overly keen to discuss energy and resource constraints with climate and environment policy makers. The global climate community has only limited knowledge about the potential of AI to support their case.

We need a structured, ongoing forum, whether through WEF, OECD or a UN platform, to explore both the possibilities and the limits of AI. Imagine annual reports on the global state of AI and sustainability jointly produced by Big Tech and IPCC, shared openly and transparently as way to achieve Earth Alignment. If we want to safeguard our future, these two communities can't remain strangers. AI and sustainability must become allies.

About the partner

Hinrich Thölken is a former Digital Ambassador and Climate and Energy Ambassador of the German Foreign Service. He now serves as Executive Vice President and Sustainability Lead at Capgemini, a global consulting and IT services company that helps organizations with digital transformation, technology solutions, and business innovation.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai