Surveillance State Expands, AI's Water Crisis Deepens, The Chip Wars Enter a New Phase

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

This issue of GeoTech Radar makes one thing uncomfortably clear – the AI race is no longer constrained primarily by science, capital, or code. Now, AI development collides with hard limits such as water tables, energy and cooling efficiency, fab capacity, mineral stockpiles, talent pools, regulatory regimes, and political powerplays. Microsoft's water footprint is swelling. Apple is struggling to contain its AI brain drain. Washington is stockpiling rare earths. And the Moltbook incident has exposed a crisis of attribution in agentic AI. The main constraint is now infrastructural power, and states and firms are competing over much more than innovation. Now, they need to consider the physical, human, and institutional substrates that make innovation possible.

The result is a less glamorous but more consequential and less linear phase of techno-geopolitics that plays out through confusing tensions. America's chip policy oscillates between denial and monetization. Europe hardens its regulatory enforcement while entertaining the possibility of loosening GDPR and the EU AI Act as transatlantic unity frays. India and Saudi Arabia pursue sovereign AI as a hedge against dependence, but with billions of dollars of U.S. investments. The U.S. enforces chip restrictions globally but then permits the most cutting-edge ICs for export to China. China weaponized minerals exports to the U.S. in protest against chip export restrictions, but now weighs whether it even still wants those chips. And, in a sign of just how binding terrestrial constraints have become, AI's frontier is now being imagined in orbit.

What emerges is not a single race but a constraint-optimization problem that pushes us beyond earth. Those who can align water, energy, minerals, talent, capital, data, and governance will shape the next decade of AI power. The firms and governments that still think this is merely a technology story are already behind. Governments should inject GeoTech experts into their embassies. Corporations should create GeoTech SWAT teams at the C-level.

On the Radar

The signals affecting the GeoTech landscape this week

ICE's Surveillance Arsenal: The Infrastructure of Mass Deportation

Immigration and Customs Enforcement (ICE) has deployed an unprecedented array of surveillance technologies in support of the Trump administration's deportation campaign. With a fiscal year budget of $28.7 billion – ten times the agency's total surveillance expenditures over the past 13 years – ICE has purchased facial recognition systems, iris scanners, cellphone location databases, military-grade drones, and spyware capable of remotely hacking phones.

The Department of Homeland Security (DHS) disclosed this week that ICE has "significantly expanded the operational scope" for its use of facial recognition, AI, and other advanced technologies. The Mobile Fortify app, powered by NEC's facial recognition suite, allows agents to scan faces in the field and compare them against 200 million images in government databases. ICE has signed a $3.75 million contract with Clearview AI, which expanded beyond its original child exploitation mandate to investigate "assaults against law enforcement officers." The agency purchased Paragon Solutions spyware, which is capable of remotely hacking phones, after the Biden administration's freeze was reversed. Thomson Reuters provides license plate data from 20 billion scans. Penlink's Webloc enables geofencing without warrants.

Legal challenges are mounting. Illinois Attorney General Kwame Raoul and the City of Chicago filed suit, alleging DHS used Mobile Fortify in the field more than 100,000 times. The ACLU has challenged warrantless geolocation tracking under Webloc. Clearview AI faces ongoing litigation in Illinois under the state's Biometric Information Privacy Act, with potential damages exceeding $50 billion if class certification succeeds.

WHY THIS MATTERS: The GeoTech implications extend beyond immigration. ICE's surveillance buildup represents the largest peacetime deployment of integrated biometric and location tracking capabilities against a civilian population in U.S. history. The architecture being constructed – including Palantir platforms that integrate facial recognition, phone tracking, license plate data, and social media monitoring – establishes infrastructure that agencies could repurpose for broader domestic surveillance. The facial recognition systems deployed domestically are also sold internationally, including to governments with poor human rights records. The Clearview AI database is accessible to law enforcement across 27 countries.

SO-WHAT: Companies providing data, technology, or services to ICE face mounting reputational and legal exposure. Palantir's $29.9 million enforcement platform contract, Clearview AI's expanding mandate, and commercial data brokers like Thomson Reuters and Penlink are now central to operations drawing international criticism. For tech companies considering government contracts, the calculus has shifted. What was once a straightforward B2G opportunity now carries significant brand risk and potential exposure to legal challenges in jurisdictions with stricter privacy regimes. For companies with immigrant workforces, understanding the surveillance capabilities being deployed against your employees has become operationally essential.

Musk's Orbital Compute Play: SpaceX Eyes $1 Trillion IPO

SpaceX is preparing to go public in 2026, with Elon Musk targeting a valuation that could exceed $1 trillion. The company is simultaneously completing its merger with xAI, Musk's AI venture. The combined entity will unite rockets, satellites, and AI under a single corporate structure.

The IPO funds would support an audacious new project. In a filing last week, SpaceX sought FCC permission to launch up to one million satellites that would function as orbital data centers. The solar-powered network would provide AI computing capacity from space, bypassing terrestrial constraints on power and cooling.

WHY THIS MATTERS: The filing signals an attempt to solve the binding resource constraints now limiting AI development on Earth. Data centers in Texas will use 49 billion gallons of water in 2025, and as much as 399 billion gallons by 2030. AI systems could have a carbon footprint equivalent to that of New York City in 2025. SpaceX argues that orbital compute sidesteps all of this. "Freed from the constraints of terrestrial deployment,” the company said in its filing, “within a few years the lowest cost to generate AI compute will be in space."

The SpaceX-xAI merger creates vertical integration across the entire stack of launch vehicles, satellite manufacturing, orbital infrastructure, and the AI models that consume the compute power. xAI raised $20 billion in its Series E round and has scaled its "Colossus" supercomputer to over 200,000 Nvidia H100 chips, but terrestrial expansion is hitting power walls. SpaceX is not alone in this race. Google's Project Suncatcher is testing TPUs in orbit, projecting that space-based data centers could become cheaper than terrestrial operations by 2035. Blue Origin announced TeraWave, a datacenter-focused optical communications satellite system.

SO-WHAT: The orbital compute thesis reframes the AI infrastructure race. If launch costs continue to decline and Starship achieves reliable reusability, the economics of space-based processing could fundamentally shift where and how AI models are trained and deployed. For hyperscalers and AI labs facing grid constraints, regulatory friction, and community opposition, orbital alternatives could become strategically relevant within this decade. More immediately, a SpaceX IPO at $1 trillion or more would redirect enormous capital toward space-based infrastructure, potentially accelerating timelines for competitors and partners alike.

U.S. Launches $12 Billion "Project Vault" to Stockpile Rare Earths

The Trump administration announced plans to create a $12 billion strategic reserve of critical minerals for civilian manufacturers, combining $10 billion in Export-Import Bank financing with $1.67 billion in private capital. The initiative, dubbed Project Vault, represents the first large-scale mineral stockpile designed specifically for private-sector use.

General Motors, Boeing, Google, and more than a dozen other manufacturers have signed on as participants. Three commodities trading houses – Hartree Partners, Traxys North America, and Mercuria Energy Group – will handle procurement. The stockpile will cover rare earths, lithium, cobalt, nickel, and graphite.

Rare earth prices have surged 40% since China's export restrictions took effect. Lithium carbonate trades at approximately $12,000 per ton, down from 2022 peaks but still volatile. The stockpile aims to buffer against price spikes that can exceed 200% during supply disruptions.

WHY THIS MATTERS: Project Vault marks an escalation in Washington's strategy to counter China's dominance over materials critical to AI infrastructure, defense systems, and clean energy manufacturing. China hosts about 70% of the world's rare earths mining and 90% of global rare earths processing. The move shifts U.S. strategy from future incentives to present control. While existing programs such as the Pentagon's MP Materials partnership and new domestic processing facilities target long-term supply chain development, a stockpile provides an immediate buffer against disruption.

SO-WHAT: Project Vault offers participating manufacturers a mechanism to hedge against volatile input prices without maintaining proprietary stockpiles. The initiative follows the Pentagon's landmark deal with MP Materials last July, in which the Defense Department took a 15% equity stake in America's only integrated rare earth producer. Together, these moves signal that Washington now treats critical minerals as instruments of geopolitical power rather than ordinary commodities. For technology and manufacturing executives, the era of cheap, frictionless access to Chinese-processed materials is ending. Those without diversified sourcing strategies or government-backed supply arrangements face growing exposure to both price volatility and potential supply disruptions.

Iran Crisis Tests Tech Supply Chain Resilience: Hormuz Chokepoint Threatens 20% of Global Oil

President Trump pulled back from the brink of military strikes on Iran this week after a sustained lobbying campaign by Israel, Saudi Arabia, and the UAE. The crisis carries profound technology and energy implications. Twenty percent of global oil transits the Strait of Hormuz, and an extended conflict would disrupt energy supplies critical to global manufacturing and emerging minerals processing investments in the Gulf. Iranian ballistic missiles can reach U.S. bases, allied infrastructure, and oil facilities across the Gulf.

"It was really close,” a U.S. official told Axios. “The military was in a position to do something really fast, but the order didn't come." U.S. troops had begun evacuating from Al-Udeid Air Base in Qatar, and Iran closed its airspace in anticipation of attack. The crisis emerged after Iranian security forces killed an estimated 5,000 protesters in a brutal crackdown on nationwide demonstrations. Trump threatened intervention and declared "help is on its way." He was presented with military options including strikes on regime targets and potential raids inside Iran.

One surprising voice urged caution. Israeli Prime Minister Benjamin Netanyahu warned the Islamic regime might not yet be weakened enough for strikes to deliver a decisive blow. Saudi Arabia and UAE ruled out use of their airspace for attacks, while Turkey offered to mediate. The deployment continues. An "armada" including F-35 and F-22 fighters, two carrier strike groups, B-2 stealth bombers, and additional Patriot and THAAD anti-missile systems is positioned in the region.

WHY THIS MATTERS: The Iran crisis reveals how energy and technology dependencies shape military options. Unlike the Venezuela operation that removed Nicolás Maduro, Iran can defend itself with ballistic missiles capable of targeting U.S. bases, allied infrastructure, and oil facilities across the Gulf. The June 2025 strikes on Iranian nuclear sites demonstrated capability but also the limits of airpower for regime change. Israel's intelligence chief traveled to Washington and Saudi Arabia is passing messages between capitals. The near-miss underscores that the technology of precision warfare cannot substitute for the political constraints on its use.

SO-WHAT: Energy and supply chain teams should answer three questions immediately: (1) What percentage of our inputs transit the Strait of Hormuz, directly or through suppliers? (2) Which critical vendors have single points of failure in Gulf logistics? (3) What is our operational continuity plan if Gulf energy supplies are disrupted for 30, 60, or 90 days? Insurance markets are already pricing Iran risk into regional shipping rates. Companies dependent on TSMC should model how Gulf energy disruption would cascade into semiconductor production timelines. The crisis is paused, not resolved. The carriers and bombers remain deployed, and another decision point could come within weeks.

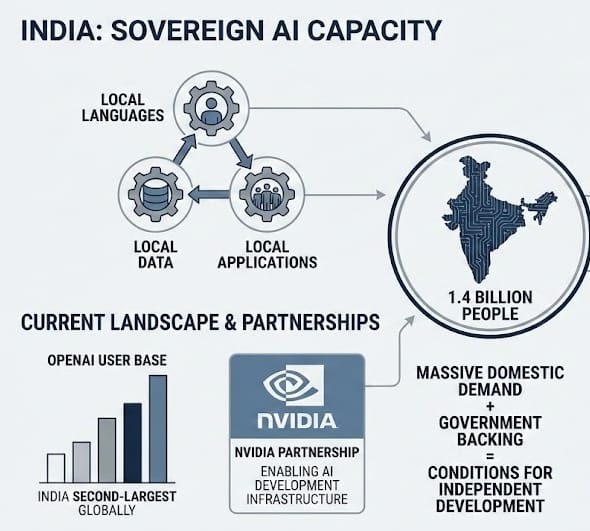

India's AI Factory Moment: NVIDIA Bets Big on the Subcontinent

NVIDIA has joined India's Deep Tech Alliance as a founding member of a $2 billion investment fund targeting semiconductors, AI, robotics, and energy startups. The company will train and mentor emerging deep tech companies through its Deep Learning Institute. Separately, Reliance Industries is building a 1-gigawatt AI data center in Gujarat powered by NVIDIA Blackwell GPUs, with eventual capacity of 2,000 MW, putting it among the world's largest AI-specific facilities.

India now hosts over 80,000 GPUs across public and private sectors, with 34,000 under the government's IndiaAI Mission. Data center capacity will more than double from 950MW in 2024 to 2GW by 2026. "It makes complete sense that India should manufacture its own AI," NVIDIA CEO Jensen Huang said. "You should not export data to import intelligence." India has developed the Nemotron-4-Hindi-4b model for Hindi language tasks. Partners including Flipkart, Sarvam AI, and Zoho are building multilingual AI for India's 22 official languages.

WHY THIS MATTERS: India is positioning itself as an alternative pole for AI infrastructure alongside the U.S. and China, but through a different model. Rather than competing on frontier models, India is building sovereign AI capacity focused on local languages, local data, and local applications serving 1.4 billion people. The strategic logic echoes Saudi Arabia's HUMAIN, Kazakhstan's AlemAI, and the EU's digital sovereignty agenda. By exporting data to import intelligence, those nations cede strategic autonomy. In India, the combination of massive domestic demand, government backing, and the NVIDIA partnership creates conditions for AI development that bypass the U.S.-China technology competition entirely.

SO-WHAT: India offers an alternative compute geography for companies seeking to diversify AI infrastructure away from concentration in U.S. and Chinese facilities. The combination of engineering talent, expanding GPU capacity, and government incentives creates development conditions potentially more stable than policy-volatile alternatives. Companies building multilingual AI applications should consider India-based partnerships that provide access to Hindi and regional language training data, a resource that’s scarce elsewhere. The February AI Impact Summit, featuring Jensen Huang and Demis Hassabis, will signal which global players are serious about the India opportunity.

The H200 Flip-Flop: Trump Opens China Chip Sales, Beijing Hesitates

The Trump administration has approved exports of NVIDIA's H200 chips to China, reversing Biden-era restrictions, with a 25% "security fee" attached. The same day, the Justice Department announced it had shut down a smuggling network trafficking the exact same chips, calling them "integral to modern military applications" and declaring, "the country that controls these chips will control the future."

Chinese companies have ordered more than 2 million H200 chips for 2026, but NVIDIA holds only 700,000 in stock and has asked TSMC to restart production. Beijing hasn't approved imports, citing concerns about overreliance on foreign technology. ByteDance reportedly plans to spend 100 billion yuan (about $14.4 billion) on NVIDIA chips in 2026 if regulators permit. Chinese officials are considering proposals that would require companies to purchase domestically produced processors alongside imports. The policy shift has strained TSMC's CoWoS advanced packaging capacity, creating global supply bottlenecks.

WHY THIS MATTERS: The H200 reversal represents a fundamental shift from technology denial to revenue extraction, taxing strategic technology transfer rather than preventing it. If implemented loosely, analysts estimate China could receive enough chips to build the largest AI data center in the world, increasing installed AI compute by 250% relative to reliance on domestic chips alone. The bipartisan consensus in Washington that sustained export controls since 2022 is fracturing, and Beijing's hesitation to approve imports reveals its own strategic calculus. Reducing dependency on American technology might matter more than immediate capability gains.

SO-WHAT: AI infrastructure planning now requires geopolitical scenario modeling. Chip availability could swing based on policy reversals, congressional action, or Chinese import decisions. The demand surge is straining TSMC's capacity, potentially affecting delivery timelines for all customers, not just those selling to China. Companies building on NVIDIA architecture face supply uncertainty as production is stretched. The "flip-flop" environment means infrastructure strategies must be engineered for regulatory volatility and aim at resilience and redundancies. The only certainty is continued uncertainty, and procurement teams need optionality built into hardware strategies.

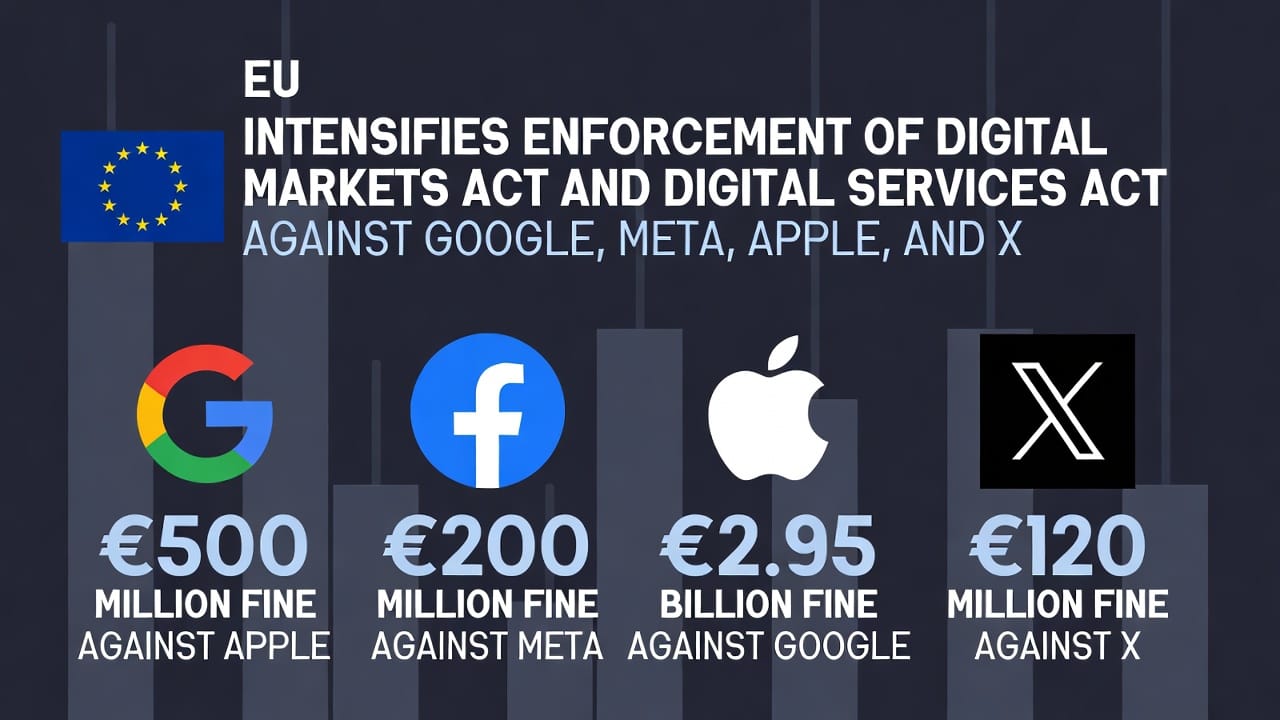

EU vs. Big Tech: Brussels Shifts from Negotiation to Enforcement

The European Union is intensifying enforcement of its Digital Markets Act (DMA) and Digital Services Act (DSA) against Google, Meta, Apple, and X, despite Trump administration threats of trade retaliation. In 2025, the EU fined Apple €500 million, Meta €200 million, Google €2.95 billion, and X €120 million. EU Competition Commissioner Teresa Ribera told the Financial Times: "We are not going to scrap our regulation simply because you don't like it."

In December, the Commission launched investigations into Meta's AI policy on WhatsApp (which prohibits rival chatbots) and Google's use of online content to train AI models. The geopolitical dimension is sharpening. Big Tech is lobbying aggressively on both continents. Google claims investigations "risk stifling innovation." Apple demands the DMA be scrapped entirely. Meta accuses the Commission of seeking to "handicap successful American business while allowing Chinese and European companies to operate under different standards." Elon Musk called for the EU to be "abolished."

WHY THIS MATTERS: The transatlantic tech conflict reveals Europe's strategic vulnerability. The DMA aims to constrain large incumbents, but Europe has no scaled alternatives to fill the gap. There is no European search engine, no European social network at scale, nor any European cloud provider that can match AWS’ or Azure's global footprint. OVHcloud and Hetzner serve niche markets. Mistral AI shows promise but remains a fraction of OpenAI's size. The Draghi Report acknowledged this explicitly. European regulation constrains American platforms without producing European champions. Denmark is phasing out Microsoft Teams for government use and Austria's military migrated to LibreOffice, but these are defensive retreats not competitive advances. Europe's digital sovereignty agenda is real, but it is sovereignty through restriction not construction.

SO-WHAT: For companies operating across jurisdictions, plan for sustained divergence. Key compliance factors to watch include Meta's revised advertising model (January 2026), regional variation in Apple's App Store terms, and the Commission's Amazon and Microsoft cloud gatekeeper assessments, which will conclude by Q2. Build compliance infrastructure that assumes different rules in different markets indefinitely, and track AI investigations closely. The Commission's inquiries into Meta's WhatsApp AI restrictions and Google's training data practices signal that AI-specific enforcement will arrive before AI-specific legislation. Companies designated as gatekeepers face rolling obligations that require dedicated compliance teams, not one-time fixes.

AI's Water Crisis: Microsoft's 28 Billion Liter Problem - A Canary in A Coal Mine?

Microsoft expects the annual water consumption across its roughly 100 existing data center campuses worldwide to more than triple to 28 billion liters by 2030, up from 7.9 billion liters in 2020, according to The New York Times. After the Times inquiry, Microsoft revised the projections down to 18 billion liters, but that 150% increase excludes more than $50 billion in new data center deals signed last year.

The geography of Microsoft’s AI water demand maps directly onto water-stressed regions. Near Jakarta, a metropolis sinking into the Java Sea partly due to drained aquifers, Microsoft's water use was projected to quadruple to 1.9 billion liters by 2030. Around Phoenix, an area navigating two decades of drought, withdrawals were forecast to reach 3.3 billion liters, more than any other location. In Pune, India, where water shortages sparked a "No Water, No Vote" campaign, Microsoft projected needs of 1.9 billion liters by 2030. Amazon has abandoned a planned Arizona complex over water concerns. Google withdrew from Chile. And Meta faces accusations of harming drinking water supplies in Newton County, Georgia.

"Water took a back seat," said Priscilla Johnson, Microsoft's former director of water strategy. "Energy was more the focus because it was more expensive. Water was too cheap to be prioritized." A multiplier effect compounds the problem. Most data center electricity comes from power plants that require massive water supplies for cooling. Cornell researchers estimate this would roughly triple actual water footprint to nearly 80 billion liters by 2030 for Microsoft alone.

WHY THIS MATTERS: The AI race is becoming a resource race with profound geo-economic implications. Water scarcity will increasingly determine where governments and companies can build AI infrastructure, and therefore which nations can develop sovereign AI capabilities. Countries with abundant water (e.g. Canada, Nordic nations, and parts of Southeast Asia) gain strategic advantages in the compute economy. Water-stressed regions (e.g. Middle East, North Africa, American Southwest, and South Asia) face constraints that no amount of capital can overcome. Microsoft Vice Chair Brad Smith compared AI infrastructure needs to the construction of power grids and highway systems. But unlike those precedents, AI's water demands concentrate in locations chosen for electricity and proximity to users, often the same drought-prone regions facing climate-driven water stress. Those earlier systems created geographic winners and losers based on physical constraints. The same could happen with AI.

SO-WHAT: Companies planning AI infrastructure must factor water availability into site selection with the same rigor as electricity access. The lack of disclosure requirements creates information asymmetry, and companies that track water dependencies gain competitive intelligence about infrastructure constraints facing rivals. Water rights in data center regions will appreciate in value, giving early movers who secure access a lasting advantage. For enterprises relying on cloud AI services, water risk becomes part of vendor due diligence. A data center in Phoenix faces different resilience profiles than one in Oregon or Ireland. The companies that survive the infrastructure buildout will be those that recognize that compute, energy, and water form an inseparable constraint triangle.

Under the Radar

The deep analysis that connects the dots

The Attribution Collapse: When AI Agents Become Plausible Deniability Infrastructure

Last week, 1.5 million AI agents joined Moltbook, a social network built exclusively for autonomous bots. The platform was "vibe-coded" by an AI assistant. Within 72 hours, security researchers at Wiz found the entire database of API tokens, private messages, and email addresses exposed. Anyone could hijack any agent, including one belonging to former OpenAI director Andrej Karpathy.

Stories about secret agentic societies, religions, and languages – all shielded from humans – generated plenty of headlines, but a deeper story did not.

Behind those 1.5 million agents were only 17,000 humans for an average ratio of 88 agents per person. Those agents operate with root access to its owner's machine, so each is capable of posting, communicating, and taking actions autonomously. Moltbook had no mechanism to verify whether content came from AI or from a human. Attribution is, as the Network Contagion Research Institute put it, 'fundamentally ambiguous'—textual output alone cannot reliably distinguish human-authored content from AI-generated content

The GeoTech implications of this type of infrastructure – a large-scale influence operation with built-in deniability – are profound. A human could seed behavior into an agent, let it propagate through an agent network, and claim the AI acted on its own. Attribution and the foundation of accountability in both law and international relations breaks down when you cannot distinguish principal from agent.

Singapore saw this coming. Frequently a first-mover on smart regulation for digital, the country released the world's first governance framework specifically for agentic AI last month at Davos. South Korea's AI Act took effect the same day. The EU's high-risk obligations land this summer. Yet again, the U.S. has only a patchwork of state laws and agency memos. No federal framework addresses autonomous systems that reason, plan, and act.

The governance arbitrage has begun. Jurisdictions with permissive rules will attract agent development, and jurisdictions without identity verification for AI systems will become launchpads for coordinated action that no one can trace back to a human decision-maker. The National Law Review analysts predict 2026 produces the first "agentic liability" crisis.

Twenty years of cybersecurity architecture was built on the assumption that humans initiate actions and systems execute them. Agentic AI inverts this. Systems now initiate, and humans observe. Attack surfaces now include the entire context window, not just the perimeter, and the threat has expanded from mere code injection to memory poisoning.

Palo Alto Networks calls it this sort of private data access, untrusted content exposure, and external communication ability the "lethal trifecta." OpenClaw has all three, plus persistent memory. Gartner issued an advisory calling it "unacceptable cybersecurity risk," but Token Security says 22% of its enterprise customers already have employees running it inside corporate networks.

What to watch: Capability curves and deployment curves are different. The agents on Moltbook are not sophisticated, the coordination is shallow, and nothing dangerous has happened yet. But it could at any moment as we stress-test this type of infrastructure on primary devices in the wild before we understand the failure modes and consider potential safeguards, remedies, and recovery protocols. The next iteration will not be an accident. It will be deliberate. Agent swarm deployment requires proactive governance on the enterprise and national levels. Agents don’t know values, rules, and state borders unless they’re chartered and taught to.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai