SCOTUS Redraws the GeoTech Map. Beijing Outspends DC on R&D. Tehran and AI Brace for Impact.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

The new geography of cognitive power means global governance for AI, data, and compute – including minerals and capital – is a fiercely contested space where commercial strategy and economic development meet geopolitical opportunism.

In one week, the Supreme Court curtailed the president’s unilateral tariff authority, Beijing overtook Washington in R&D spending. India convened the Global South, with domineering voices rejecting universal AI rules in favor of plurilateral clubs. And the Pentagon signaled that AI safety commitments might not survive contact with national security demands.

Three tensions define this evolving landscape.

1. Executive Coercion vs. Legal Authority

SCOTUS drew a line around presidential tariff power, pushing trade authority back toward Congress and injecting legislative risk into supply chains. At the same time, the Pentagon’s pressure on Anthropic illustrated the government’s ability to condition market access on model behavior. Trade flows and AI guardrails now sit in the same arena as constitutional limits, procurement leverage, and national security. For leaders, this determines tariff exposure, model deployment choices, and the risk of corporate commitments being overridden by the state.

2. Private Capital vs. Public Power

In China, where state direction and corporate capital are fused, spending compounds directly into standards, labs, talent pipelines, and rapid development cycles. In the U.S., federal research uncertainty contrasts with VC and sovereign wealth investment, with the private-sector leading the way. India converts capital commitments into sovereign compute capacity with uncertain public/private balance as of yet. In all of these, capital underwrites national capability. The question is whether market-driven systems can outpace state-coordinated ones, or whether the state’s capital can lead to more coordinated and strategic longer term advantages

3. Exclusivity vs. Stability in Minerals

The FORGE and Project Vault programs move U.S. mineral policy from deals to blocs, using price floors and stockpiles to secure aligned supply. However, producer countries are exercising new leverage. Indonesia forced downstream nickel investment. The DRC is demanding equity, not just royalties. Chile is rewriting lithium terms. The African Union has formalized value-chain participation as policy. Many will join Western frameworks and hedge with Beijing simultaneously. Exclusivity offers security for buyers. Stability requires flexibility for sellers.

No universal global systems are emerging across trade law, AI governance, capital flows, and mineral supply. Overlapping clubs with competing rules and coercive tools requires a strategy that doesn’t choose sides, but instead builds resilience and exploits opportunity across groups that have multiple allegiances.

On the Radar

The signals affecting the GeoTech landscape this week

SCOTUS Clips Trump’s Trade Arsenal. Tech Supply Chains Catch the Shrapnel.

The Supreme Court just gutted tariffs, but the trade war is not over. It just got messier.

SO WHAT FOR LEADERS: Audit your tariff exposure now. The Supreme Court struck down International Emergency Economic Powers Act (IEEPA) tariffs, but the trade war didn’t end. It shifted to Congress. While IEEPA tariffs on tech inputs are gone, the Section 232 and 301 tariffs remain. If you import server components, fiber, or rare earth magnets, your landed costs just changed. Steel and aluminum? No change. Map the delta and renegotiate fast.

The White House will seek new trade authority, and the 150-day Section 122 window (capped at 15%) is a brief window of clarity. Lock in contracts, stress-test procurement, and track the legislative calendar. The next tariff regime will be written by Congress.

THE BRIEFING: The Supreme Court ruled 6-3 on February 20, 2026 that IEEPA does not authorize the President to impose tariffs. Chief Justice Roberts wrote that Trump asserted “the extraordinary power to unilaterally impose tariffs of unlimited amount, duration, and scope” and that the text “cannot bear such weight.” The ruling invalidated the broadest swath of Trump-era tariffs, including reciprocal tariffs and fentanyl-related duties on China, Canada, and Mexico. CBP had collected roughly $133 billion in IEEPA tariffs as of mid-December. Trump immediately imposed a 10% “temporary import surcharge” under Section 122 of the Trade Act of 1974, raising it to 15% the next day.

For two years, the president cited IEEPA as justification for unchecked authority to impose tariffs at any rate, on any country, with no Congressional approval and no expiration. That power was unprecedented and, according to six justices, unconstitutional. The ruling restores the basic principle that taxing authority belongs to Congress. Section 122 caps emergency tariffs at 15% for 150 days. Section 232 and Section 301 remain for national security and unfair trade cases, but both require formal investigations and statutory timelines.

India Hosts the Global South’s First AI Summit

New Delhi rewrites the AI playbook. The Global South gets a seat, but Washington says there are no global rules.

SO WHAT FOR LEADERS: If your AI strategy assumes the regulatory debate is between Washington and Brussels, update it. Delhi just opened a third front, and three factors illustrate how seriously Indian leaders take their GeoTech role.

First, the country has committed more than $200 billion toward developing itself as a major compute geography, rather than just a talent pool. India formally joined Pax Silica on the summit’s final day, tightening the U.S.-India technology axis. And new partnerships between frontier AI labs and Indian conglomerates signal the next wave of AI deployment will not run exclusively through Silicon Valley and Shenzhen.

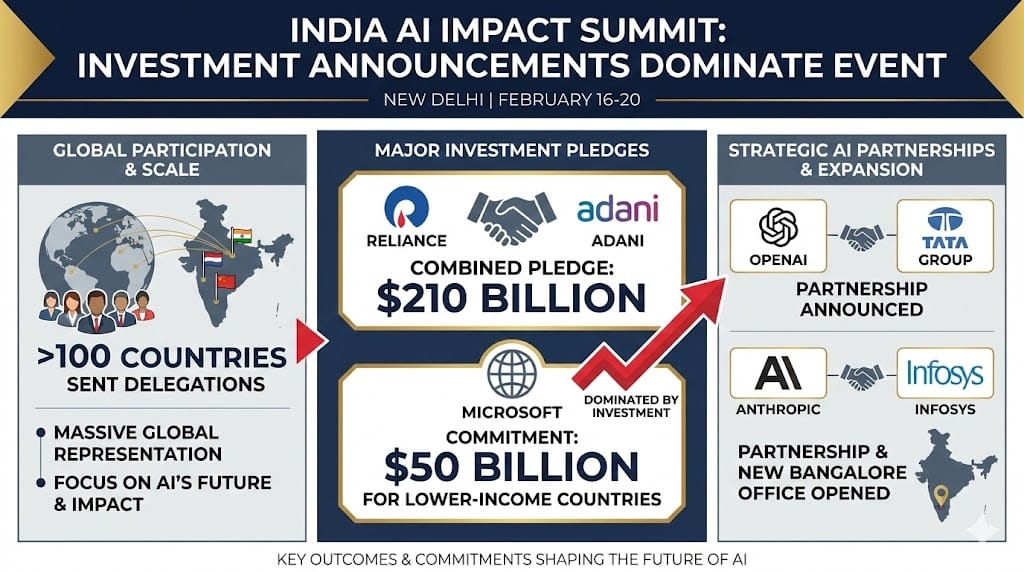

THE BRIEFING: The India AI Impact Summit ran February 16-20 in New Delhi, the first such summit hosted by a Global South nation after previous gatherings in Bletchley Park, Seoul, and Paris. More than 100 countries sent delegations, and investment announcements dominated the event. Reliance and Adani pledged a combined $210 billion for data center and AI infrastructure buildouts, Microsoft committed $50 billion for lower-income countries, OpenAI partnered with Tata Group, and Anthropic partnered with Infosys and opened a Bangalore office. President Trump’s science and technology adviser Michael Kratsios used the platform to reject global AI governance outright, unveiling the American AI Exports Program and declaring that “ideological, risk-focused obsessions, such as climate or equity, become excuses for bureaucratic management and centralization.”

On the summit’s final day, India formally joined Pax Silica, the U.S.-led coalition launched in December 2025 to secure semiconductor and critical mineral supply chains. India was notably absent from Pax Silica’s original launch alongside Australia, Japan, South Korea, Singapore, and the UK, making its inclusion a significant expansion of the U.S.-India technology axis. At least 75 countries signed the non-binding “Delhi Declaration,” although China was largely absent. The summit confirmed that the governance circuit has expanded beyond the transatlantic axis, but also that no common rules will emerge from it.

The Pentagon Tells AI: Drop Your Guardrails or Lose the Contract

Defense Secretary Hegseth threatens to blacklist Anthropic. The real target is every AI company’s safety commitments.

SO WHAT FOR LEADERS: Map your AI vendor’s government exposure now. The Pentagon’s negotiations with frontier AI firms will shape what AI can and cannot do across the entire economy, not just defense.

Claude is the only frontier model on classified networks, making Anthropic a key test case, but the real target is industry-wide safety constraints. OpenAI, Google, and xAI have already signaled compliance. If Anthropic yields or is forced out, no firm will retain safety commitments that conflict with government demands.

The leverage comes from a potential “supply chain risk” designation, which was built for foreign adversaries like Huawei. Used against a domestic AI company, though, it would ripple far beyond defense into the commercial stack.

THE BRIEFING: The confrontation reached a breaking point in February 2026, but the initial trigger came on January 3, when the U.S. military captured Venezuelan President Nicolás Maduro. Axios reported that Claude was used during the operation through Anthropic’s Palantir partnership. Pentagon officials allege an Anthropic executive subsequently contacted Palantir to express disapproval. Although Anthropic flatly denied this, Secretary of War Pete Hegseth on February 15 moved to cut ties with the company. Within days, the chief Pentagon spokesman confirmed the relationship was “being reviewed,” and Undersecretary Emil Michael publicly urged Anthropic to “cross the Rubicon.”

Anthropic’s two stated red lines are mass domestic surveillance and fully autonomous weapons. OpenAI, Google, and xAI have all agreed to lift consumer-facing guardrails for military work, but none yet operate on classified networks where Claude has no peer. The broader question is whether safety commitments survive contact with the world’s largest customer. The July 2026 deadline for all AI vendors to sign “any lawful use” terms is the clock to watch.

China Outspends the U.S. on R&D

China surpassed the U.S. in R&D spending for the first time. The innovation order has shifted.

SO WHAT FOR LEADERS: If your strategy assumes enduring American tech dominance, stress-test it now.

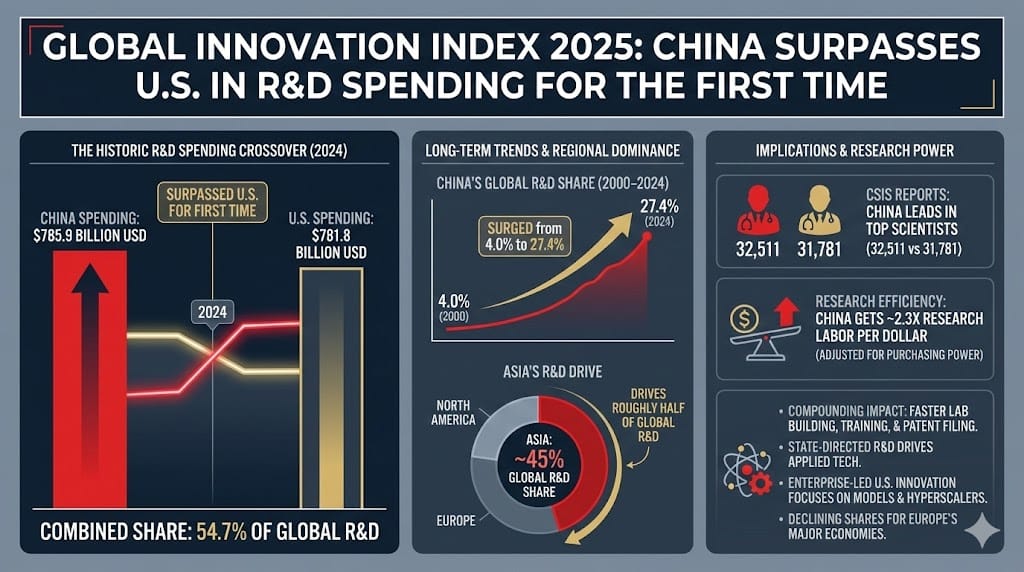

This current cycle of high-tech development differs from the usual “China is rising” cycle because of the booming scale of Chinese investment. China has 524 firms in the global top 2,000 R&D spenders, and in 2024 it outspent the U.S. on R&D for the first time ($785.9 billion versus $781.8 billion). That greater spending will compound, too. More capital builds more labs, talent, and patents. While U.S. enterprise still leads in frontier models, China’s state-directed system delivers scale across AI, chips, biotech, quantum, and advanced manufacturing, often with 2.3 times the research labor per dollar on a purchasing power basis.

The winners will build into both ecosystems without tripping regulatory wires. Conduct a fine-mesh risk and opportunity scan now.

THE BRIEFING: According to the World Intellectual Property Organization’s Global Innovation Index 2025, China surpassed the U.S. in R&D spending for the first time in 2024. Together the two countries account for 54.7% of all global R&D. However, China’s share has surged from 4% in 2000 to 27.4% today. It now fields more top scientists than the U.S. and, thanks largely to Chinese investments, Asia now drives roughly 45% of global R&D. CSIS reports China has also surpassed the U.S. in number of top scientists for the first time (32,511 vs 31,781). Europe’s major economies saw declining global shares across these metrics.

The country that spends more this year will build the labs, train the researchers, and file the patents that produce next decade’s breakthroughs. China’s state-directed R&D can drive faster gains in applied technologies, particularly where sustained investment over many years is required. The U.S. enterprise-led model still tends to drive more frontier innovation around models, but it depends on federal funding for basic research that is now under threat.

Tehran Braces for Impact. The Gulf’s Compute Bet Does Too.

The U.S. has two carrier groups off the coast of Iran, and the largest air buildup since 2003. Diplomacy, as well as energy and tech supply chains, have days, not months.

SO WHAT FOR LEADERS: Activate your Gulf contingency plans now, not next week.

Rather than just listening to diplomatic statements, watch the insurance markets. Shipping premiums in the Strait of Hormuz have spiked. Lloyd’s of London is adjusting war risk coverage. Energy futures are pricing in disruption risk. These are not political signals, they are actuarial ones. The money has already decided this is serious.

Your analytical frame should be second-order effects. A fifth of globally traded oil transits a 21-mile chokepoint. Even a limited disruption cascades through energy prices, shipping insurance, and supply chains from East Asia to Europe within hours. A conflict that disrupts Gulf energy grids does not just move oil prices, it threatens the physical compute infrastructure on which billions of dollars in AI investment plans depend. Model the Hormuz disruption scenario and update personnel contingency plans for the Gulf. The signal-to-noise ratio has shifted from rhetoric to readiness

THE BRIEFING: The U.S. has deployed the USS Abraham Lincoln and USS Gerald R. Ford carrier strike groups, plus an estimated 50+ additional fighter jets to the Middle East. This is the largest American airpower concentration in the region since the 2003 Iraq invasion. Trump told reporters on February 20 that “10-15 days would be pretty much maximum” for Iran to present a deal. Indirect talks in Geneva on February 18 produced no breakthrough. The White House has been briefed that the military is ready for strikes, though Trump has not made a final decision.

Iran has responded by hardening nuclear sites at Natanz and Parchin, increasing naval patrols, and holding joint exercises with Russia. Iran’s proxy buffer has collapsed after Israeli operations against Hamas and Hezbollah, removing the asymmetric options Tehran relied on for decades and making direct confrontation more likely. The technology dimension is the Gulf’s emerging role as AI infrastructure. The UAE and Saudi Arabia are building 3.3 GW of data center capacity by 2030, triple the current 1 GW, anchored by projects like the 5 GW Stargate UAE campus and Saudi Arabia’s Humain initiative. The Gulf electricity that makes these projects viable depends on stable hydrocarbon supply, so a conflict that disrupts Gulf energy grids threatens the physical infrastructure layer of an AI buildout worth tens of billions in committed investment. Meanwhile, war risk insurance premiums for vessels transiting the Strait of Hormuz have already jumped more than 60%, adding $200,000-$360,000 per VLCC voyage. Those costs cascade through every supply chain that routes through the Gulf.

The Minerals Trade Bloc Takes Shape

The U.S. gathers 54 countries, sets price floors, and creates a $12 billion stockpile. Washington just proposed a NATO for minerals.

SO WHAT FOR LEADERS: Map your supply chains against FORGE member countries now. If your gallium comes from China and your lithium from a non-FORGE producer, you are exposed to both price floor increases and potential supply disruption.

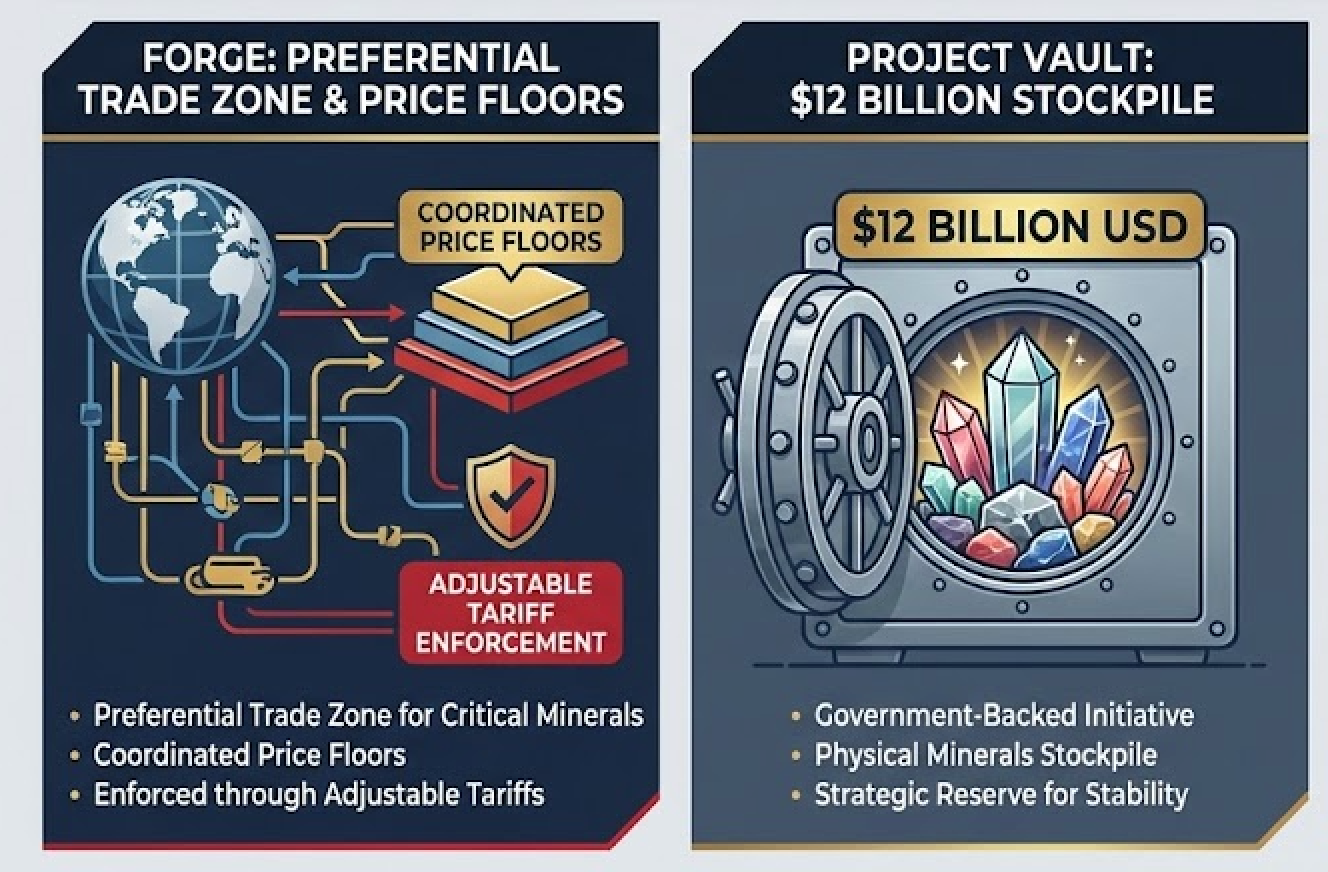

Critical minerals policy has graduated from bilateral deals to a broader institutional architecture, with FORGE bringing certain nations into a preferential trade zone with coordinated price floors enforced through adjustable tariffs. Along with Project Vault, the $12 billion minerals stockpile, the U.S. has become a convener of a minerals coalition and a commodities market-maker, a combination with no precedent in modern trade policy. This could raise your input costs for AI chips, batteries and defense systems. Producers will join if the economics work, but they’ll hedge with Beijing regardless.

THE BRIEFING: On February 4, the U.S. convened 54 countries at the inaugural Critical Minerals Ministerial in Washington. The centerpiece was the Forum on Resource Geostrategic Engagement (FORGE), replacing the Biden-era Minerals Security Partnership. Vice President J.D. Vance described it as a “preferential trade zone for critical minerals” with “reference prices at each stage of production” maintained through “adjustable tariffs.” Two days earlier, Trump announced Project Vault, a $12 billion strategic minerals reserve backed by a $10 billion EXIM loan, the largest in the bank’s history. GM, Boeing, Google, Stellantis, and Corning have reportedly expressed interest in tapping the stockpile.

The U.S. signed 11 new bilateral mineral frameworks, bringing the total to 21 in five months with 17 more in negotiation. The U.S., EU, and Japan announced joint action plans including border-adjusted price floors. The Atlantic Council assessed FORGE as a shift from bilateral dealmaking to plurilateral coalition-building. The Natural Resource Governance Institute warned the trade bloc approach forces producer countries into alignment choices many will resist. The coalition’s first real test comes when reference prices are set. If FORGE price floors push input costs above what manufacturers can absorb, members will face pressure to defect or seek exemptions. The July USMCA negotiation deadline should be a critical inflection point.

Under the Radar

The deep analysis that connects the dots

The Global South’s Leverage Play

The countries that own the ground are rewriting the rules, and neither Washington nor Beijing controls the outcome.

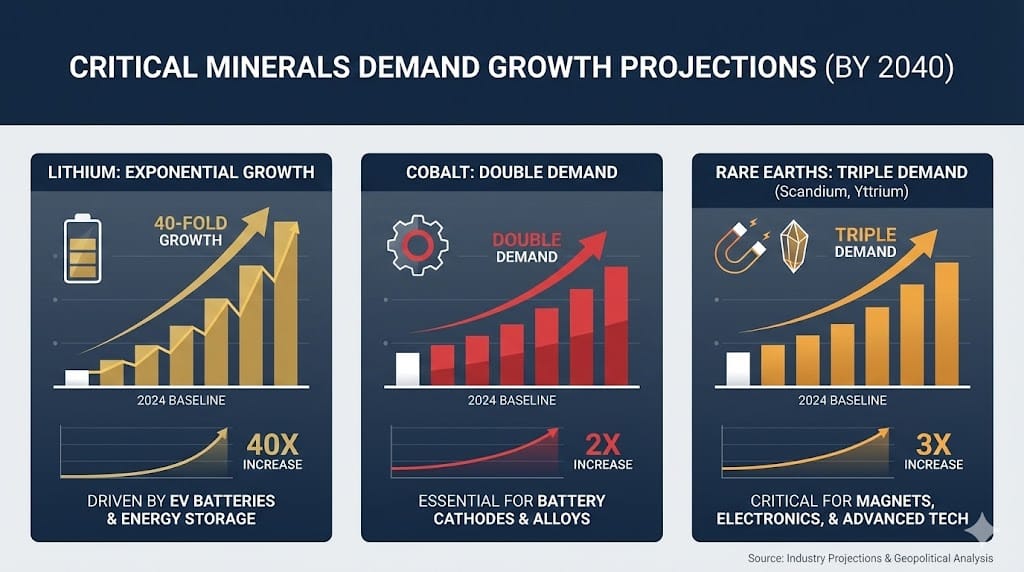

SO WHAT: Get your cost structure ready to absorb increased minerals supplier leverage. The countries sitting on the raw inputs required by AI infrastructure, such as cobalt, lithium, rare earths, and gallium, are discovering that structural demand gives them leverage that previous commodity cycles never did.

The Global South has spent decades on the wrong end of resource extraction. Cobalt mined in the DRC got processed in China and turned into batteries sold by American companies. That dynamic is reversing because both Washington and Beijing now need these countries badly enough to compete for their alignment.

The risk for Washington and Brussels is that their mineral diplomacy assumes these countries will choose sides. They will not. They will play both. The mineral map is also a power map, and it is being redrawn by the people who own the ground.

DEEP DIVE: Indonesia banned raw nickel exports in 2020, forcing $15 billion in foreign smelter investment and turning the country from a raw commodity exporter into the world’s largest nickel processor within three years. The DRC, which supplies more than 70% of the world’s cobalt, is now conditioning mining concessions on conflict resolution frameworks and demanding equity stakes in processing facilities rather than royalty-only arrangements. Rather than isolated policy, these and similar choices by countries with critical mineral resources represent a coordinated recognition that the clean energy transition and AI infrastructure buildout has resulted in structural demands that will not disappear. The demand curve will give producer countries durable leverage they’ve never had before. The question is whether they can institutionalize it before the window closes.

The geopolitical dynamics create a uniquely favorable environment for resource nationalism. Washington is building FORGE and signing bilateral frameworks as fast as it can. Beijing is deploying infrastructure-for-minerals deals across Africa and Central Asia. The EU is scrambling to catch up with its Critical Raw Materials Act. All three are competing for the same finite set of deposits, and all three need access urgently enough to make concessions they would not have considered five years ago. Producer countries are exploiting this competition with increasing sophistication. Pakistan, for example, structured the $1.3 billion Reko Diq copper-gold deal to give the government a 25% equity stake plus royalties, a model that would have been unthinkable a decade ago.

The deeper question for strategists is whether this leverage window is permanent or cyclical. Three factors suggest it has staying power. First, the minerals in question have no near-term substitutes at scale. You cannot build an AI chip without rare earths. Second, new mine development takes 10 to 15 years from discovery to production, meaning supply cannot respond quickly to demand shifts. Third, the simultaneous competition from multiple great powers ensures that no single buyer can dictate terms.

The risk for corporate procurement teams is that they keep treating mineral sourcing as a cost optimization problem when it has become a geopolitical function. The risk for Washington is assuming that alliance frameworks guarantee stable supply. They guarantee access, not loyalty. As CFR President Michael Froman observed, the U.S. “might be an increasingly difficult partner, but on a number of issues, we remain indispensable.” Producer countries will hedge with Beijing the moment FORGE economics stop working for them, and a single U.S. tariff escalation against a FORGE member could fracture the coalition. The risk for Beijing is that its refining dominance becomes a liability if producer countries condition raw material exports on local processing requirements. The companies and governments that understand these dynamics will secure predictable supply. Those that assume the old extraction model still holds will find themselves outmaneuvered by the countries that own the ground.

Cambrian Partner By Invitation

Expert analysis from our global network

Before the Quantum Storm: A Migration Roadmap for Leaders

Quantum computing represents a phenomenal leap forward in its promise for solving computational problems that cannot be managed by today's classical computing. The growing potential for groundbreaking advances in medicine, material sciences, energy, finance, and logistics hint at the remarkable upside of quantum computing. However, we must also protect against its possible downsides, especially its ability to break modern day encryption. While necessary, an active migration to quantum-resistant cryptography on our classical compute infrastructure brings a degree of complexity for all organizations.

Since 2024, CISA and NIST have released guidance that mandates federal agencies to prepare now for the deprecation of current encryption standards by 2030 (RSA, ECDSA, ECDH). NIST plans to disallow these standards entirely by 2035. According to ISACA's 2025-2026 study, 55% of organizations report not having started evaluating this issue, and only 4 to 5% have a defined strategy.

What Organizations Can Do Now

First, treat this as a long-term security and business migration, not a quantum technology initiative. Resist the urge to explore every quantum use case. Quantum technology is merely the potential threat vector in this classical cybersecurity scenario. Focus leadership's attention on broader enterprise risk: which systems are most critical to the organization's function and survival, and which exposures would leave the organization legally, operationally, and financially vulnerable?

Treat this undertaking as you would a modernization effort. Convene a cross-functional team to prioritize high-value systems for transition and evaluate the complexity, budget, timeline, talent, and leadership needed to produce a practical roadmap that the C-Suite and Executive Board can approve. Establish common metrics for testing, remediation, documentation, and accountability across system owners, software components, cryptographic assets, and third-party dependencies. The cryptographic asset discovery, inventory, and testing phases must be comprehensive, accurately vetted, and mutually agreed upon by system owners, IT, and Security.

These migrations can take upwards of seven to ten years or more to complete, and the window for waiting is closing. Know your organization's threat profile and requirements in great detail prior to investing in consultants and tools to assist. These are actions you will not regret.

About the Partner

Debbie Taylor Moore is a 25-year information security executive who has led implementations of security programs across 26 countries and four continents. She is a former VP of Cybersecurity for IBM Consulting, SecureInfo, and Verizon, and is Founder and CEO of The Quantum Crunch, a U.S.-based advisory firm serving global government and commercial entities on Post-Quantum Cryptographic Migration. She serves as Vice Chair of the Cyber AB Board for the Pentagon and on the Executive Board of the Consumer Technology Association, which produces CES, the largest tech show on earth.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 8'