Munich Recalibrates. Sovereign Capital Floods AI. Japan Returns to Silicon.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

The mood in Munich was sober, even frayed. American and European officials spoke of unity while insisting on renegotiating its terms. Defense budgets will rise. NATO will adapt. But will it do so fast enough with new defense tech and geotech capabilities?

Beyond the speeches and communiqués, a different story has started to unfold. As Washington and Brussels debate percentages of GDP and institutional prerogatives, sovereign wealth funds from Singapore, Abu Dhabi, and Doha are savvily writing checks to the architects of the AI era. These countries are accumulating stakes in frontier model builders, securing relationships with cloud providers, and anchoring themselves inside the most consequential technology platforms of the century. They have understood that strategy, at this moment, is less about future reliance than about today’s capitalization.

Compute resources tie these developments together through critical tensions: The cost of AI inference is collapsing at extraordinary speed, even as total spending on AI infrastructure surges. Open-weight models are approaching parity with proprietary systems, reshaping the economics of software and eroding old moats. Cheaper intelligence does not reduce demand, it multiplies it. Each incremental decline in cost expands the range of applications, which in turn drives more demand for data centers, advanced chips, rare earths, and electricity. The AI stack now stretches across lithium brines in Argentina, the 2-nanometer fabrication lines in Japan, and the hyperscale cloud regions in the Middle East. It is a single system with many economic and geopolitical layers and pressure points.

Energy markets reveal the foundational layer of this transformation. As federal climate regulation in the United States is rolled back and Europe debates its security architecture, hedge funds deploy machine learning to trade the volatility produced by extreme weather, renewable intermittency, and AI-driven load growth. Power has become a strategic asset class. The next phase of the AI will be shaped by those who secure compute, minerals, chips, and power – and those who understand that these domains now rise or fall together. The new Geography of Cognitive Power is emerging.

On the Radar

The signals affecting the GeoTech landscape this week

Munich's Fork in the Road

The 62nd Munich Security Conference opened last weekend at one of the most significant inflection points in the transatlantic relationship since the Cold War. U.S. Secretary of State Marco Rubio told European leaders the United States and Europe “belong together” and wants Europe “to be strong.” The tone was warmer than Vice President J.D. Vance’s combative speech last year, but the conditions were no less rigorous. Europe must take “primary responsibility for its own conventional defense,” as Undersecretary Elbridge Colby told NATO defense ministers meeting days before Munich. NATO’s new defense investment pledge, agreed at the 2025 Hague Summit, now calls for countries to commit 5% of GDP by 2035 on combined defense and security-related spending, with at least 3.5% of GDP going to core defense budgets. The commitment requires an additional $1.9 trillion in annual spending across the alliance, according to Atlantic Council estimates. Germany has already announced plans to raise its core defense budget from 86 billion euros today to 153 billion euros by 2029.

The defense-technology dimension is the critical GeoTech signal. European Commissioner for Defense Andrius Kubilius called for “massive innovation in defense” at the Munich Security Breakfast. Autonomous drone partnerships between German firms Helsing and Hensoldt were advertised at Munich Airport. The UK and Italy are taking over NATO joint force commands from the U.S. in Norfolk and Naples. Helsing, a Munich-based defense AI company, is building autonomous targeting systems for European militaries and represents a new class of European defense-tech champions operating outside traditional procurement hierarchies. Meanwhile, artillery shell costs have quadrupled since 2022 (from $2,000 to over $8,000 per 155mm round), and Leopard 2 tank prices have jumped from $23 million to $30 million in months, evidence that defense industrial capacity has become a binding constraint.

The Munich Security Report 2026, titled “Under Destruction,” suggested the world has entered a period of “wrecking-ball politics.” Denmark’s intelligence services assessed the United States itself as a potential security threat after President Trump’s continued rhetoric about Greenland. Russia conducted more than 20 drone intrusions into Polish airspace in September alone, and three MiG-31 fighters violated Estonian airspace for 12 minutes. Russian sabotage, cyberattacks, and surveillance operations against European energy grids are blurring the line between war and peace. CFR President Mike Froman framed the choice in a New York Times guest essay, writing that one path leads to a recalibrated NATO with a strong, self-sufficient Europe, and the other leads to “trans-Atlantic divorce proceedings.”

SO WHAT FOR LEADERS: The early architecture of a European defense-technology ecosystem is being built in real time, creating new procurement channels and industrial partnerships that bypass traditional U.S.-led NATO structures. Business leaders should consider three questions:

1) Which of your defense and dual-use contracts currently flow through U.S.-led NATO procurement channels that could shift to European-led structures?

2) Does your firm have relationships with emerging European defense-tech champions such as Helsing, MBDA, or Rheinmetall?

3) If NATO’s European pillar becomes the primary buyer of conventional defense technology, how does your government affairs strategy need to change?

Anthropic and the Sovereign Wealth Machine

Anthropic closed a $30 billion Series G funding round this week at a $380 billion post-money valuation, more than doubling its value in five months. It is the second-largest private tech financing round on record, behind only OpenAI’s $40 billion raise last year. The investor list reads like a map of global capital allocation strategy. Singapore’s sovereign wealth fund GIC co-led alongside Coatue, with the Qatar Investment Authority, Abu Dhabi’s MGX, and Singapore’s Temasek all participating. Nvidia, Microsoft, BlackRock, and Sequoia joined the party, too.

Anthropic’s annualized revenue has reached $14 billion, growing more than 10x annually for three consecutive years. Its AI coding tool Claude Code now generates $2.5 billion in annualized revenue on its own, with business subscriptions quadrupling since January. The number of enterprise customers spending over $100,000 a year grew 7x in the past 12 months. Eight of the Fortune 10 are now Claude customers. A recent analysis estimated that 4% of all public GitHub commits worldwide are now authored by Claude Code, double the share from a month earlier.

This latest round embeds significant compute dependency. Microsoft and Nvidia’s participation is tied to a commitment for Anthropic to purchase $30 billion in computing capacity from Microsoft’s Azure. Amazon and Google have also been major backers. The three largest cloud providers are simultaneously investors in and suppliers to the company whose products are accelerating the disruption of the software industry – the same industry that built those same clouds in the first place.

SO WHAT FOR LEADERS: Three sovereign wealth funds from the Gulf and Southeast Asia now hold significant positions in both of the world’s most valuable AI startups. These are not passive financial allocations. GIC’s co-lead reflects Singapore’s sovereign compute strategy, which includes building national AI infrastructure on Alibaba’s Qwen models. MGX is Abu Dhabi’s dedicated vehicle for AI infrastructure investment, deploying capital across data centers, chips, and model developers simultaneously. These states are securing preferred access to frontier models as a matter of national capability, not just return on investment. Meanwhile, the concentration of global AI capability in two San Francisco companies – both dependent on the same three cloud providers – creates a fragility that sovereign investors are simultaneously profiting from and insuring against. Business and government leaders should consider three key factors: 1) Track sovereign wealth fund AI investments as signals of national AI strategy. When GIC, MGX, and QIA invest together, they are coordinating state-level compute positioning. 2) If your enterprise is adopting AI coding tools, model the downstream effects on your software vendor relationships. The $2.5 billion Claude Code revenue is coming directly out of traditional developer tooling budgets. 3) The dependency chain from Anthropic to Azure to Nvidia GPUs creates concentration risk that leaders need to track. A disruption at any node can cascade into your critical operations.

The Minerals Chessboard

Two stories are converging into one strategic picture. China continues to weaponize its dominance over critical minerals processing, while Argentina has become the most aggressively deregulated mining jurisdiction in the Western Hemisphere. In October 2025, China suspended its rare earth export controls as part of a trade detente, sparking President Trump’s announcement of a U.S. Strategic Critical Minerals Reserve, which is designed to protect American manufacturers from future Chinese supply cutoffs. China’s April controls on seven rare earth elements remain in force. Companies still require MOFCOM export licenses. The licensing system gives Beijing case-by-case discretion over who gets supplied and when. All told, China controls roughly 70% of global rare earth mining and 90% of processing. For magnets used in EVs, wind turbines, and defense systems, China’s share of global production has risen from approximately 50% two decades ago to 94% today. TDK, the Japanese magnets manufacturer, told investors on its earnings call that tighter Chinese controls are creating a “challenging environment.” New 2026 rules also restrict exports of tungsten, antimony, and silver.

Meanwhile, in Argentina, Rio Tinto’s $2.5 billion investment in the Rincon lithium project in Salta province, approved under President Javier Milei’s Large Investment Incentive Regime (RIGI), is the single largest foreign direct investment in Argentine mining in decades. Ten RIGI-approved mining projects are now in play, with 20 more under evaluation, together representing an estimated $63 billion in potential investment. Production is projected to increase 340% by 2035 according to Benchmark Mineral Intelligence. Rio Tinto acquired Arcadium Lithium for $6.7 billion, consolidating two of Argentina’s three major lithium operations. France’s Eramet and South Korea’s Posco have brought new lithium plants online this year.

The full picture requires an understanding of how these stories fit within a broader global supply chain – including in Australia, Chile, and a half-dozen other producers. For lithium specifically, Australia remains the world’s largest producer (88,000 metric tons in 2024), followed by Chile (49,000 MT), China (41,000 MT), and Argentina (which is fifth, behind Zimbabwe). While Argentina stands out in resources with 23 million tons of identified lithium resources, Bolivia, Chile, and Australia also contain significant resources. The critical minerals picture features a wide range of countries but, at present, China and Argentina are painting the boldest strokes.

SO WHAT FOR LEADERS: China’s processing monopoly is the real chokepoint, not mine production. Even as alternative lithium supply comes online from Australia, Chile, Argentina, and Zimbabwe, those minerals still flow through Chinese refining infrastructure for conversion into battery-grade materials. China controls 60% of global lithium refining and 90% of rare earth processing. Argentina’s RIGI framework is a promising test case for Western-aligned supply, but 30-year regulatory stability requires more than one president, so leaders should keep an eye on Milei’s political durability. In addition, business and government should take three steps: 1) Map every Chinese-origin rare earth and critical mineral input in your supply chain, including through suppliers’ suppliers. The bottleneck is processing, not mining. 2) Evaluate Argentine and Australian sourcing as hedges, but recognize that the gap between China’s tightening and alternative processing capacity coming online is measured in years, not months. 3) Companies that wait for the market to solve this will be the last to secure alternative supply.

The Inference Collapse

An Nvidia analysis published this week shows that four leading inference providers have achieved 4x to 10x reductions in the cost-per-token of running AI models, gains achieved by switching to the new Blackwell GPU platform. Sully.ai cut healthcare inference costs by 90% (a 10x reduction) and improved response times 65% by switching from proprietary models to open-weight alternatives on Blackwell. DeepInfra reduced cost-per-million-tokens for a large mixture-of-experts model from 20 cents on Hopper to 5 cents on Blackwell using the native NVFP4 low-precision format. Decagon saw a 6x cost reduction per query for AI-powered voice customer support. The SemiAnalysis InferenceMAX v1 benchmark, released this month, showed that a $5 million investment in Nvidia’s GB200 NVL72 system can generate $75 million in token revenue, a 15x return on investment.

These numbers confirmed a broader trend noted in Stanford University’s 2025 AI Index, which found that inference costs for GPT-3.5-level performance dropped over 280-fold between November 2022 and October 2024. MIT Sloan research published in January found that open-weight models now achieve near-parity with closed models (a gap of just 1.7% on some benchmarks, down from 8% a year prior) while costing 87% less to run. The researchers estimated that optimal substitution from closed to open-weight models could save the AI industry approximately $25 billion annually. Nvidia is already promising another 10x improvement with the next-generation Rubin platform.

The geopolitical dimension of the open-weight shift is critical. China has emerged as the world’s leading producer of open-weight AI models. Alibaba’s Qwen model family overtook Meta’s Llama as the most downloaded language model family on Hugging Face in September 2025. Stanford HAI researchers found that Chinese developers accounted for 17.1% of all model downloads, edging out U.S. developers at 15.8%. Generative AI developed by Chinese companies now accounts for roughly 15% of global market share, up from approximately 1% a year earlier. DeepSeek, Alibaba, Moonshot AI, and Baidu are all releasing high-performance open-weight models at a fraction of U.S. proprietary pricing. The cost collapse is a hardware story, but also a geopolitical competition in which China’s open-weight strategy is reshaping who controls the economics of AI inference globally.

But here is the critical issue that leaders need to understand. Despite per-token costs plummeting, total enterprise AI inference spending has surged dramatically. This is a textbook case of Jevons paradox. As AI becomes cheaper to use, organizations deploy it across more applications, and aggregate demand overwhelms the per-unit cost savings. MarketsandMarkets Research projects the inference market will reach $255 billion by 2030. In that context, the hyperscaler capex buildout (Amazon $200 billion, Alphabet $175-185 billion, Meta $115-135 billion, and Microsoft roughly $120 billion or more in 2026, totaling close to $650 billion combined) does not look like irrational exuberance. It looks like the infrastructure response to an inference demand growing faster than costs are falling.

SO WHAT FOR LEADERS: The inference collapse is the connective tissue for nearly every story in this issue. It explains why sovereign wealth funds are pouring capital into AI companies, why Japan is racing to build 2nm fabs, why energy trading profits are surging, and why the rare earth and chip supply chains are under pressure. Leaders will need to audit their organizations’ AI model portfolios. If you are paying for proprietary API access, benchmark open-weight alternatives on equivalent hardware. The MIT research suggests potential savings of up to 87% with comparable performance. Organizations will also need to budget for the Jevons paradox, understanding that their per-token costs will fall but their total AI spend will likely rise as new use cases proliferate. Leaders should seek to develop governance frameworks that connect spending to business outcomes. Finally, the shift from training to inference as the dominant cost center changes the infrastructure calculus. Training is a one-time expense, but inference is continuous and scales with every user interaction. Plan your compute procurement accordingly.

Climate Skeptics Kill the EPA Endangerment Finding

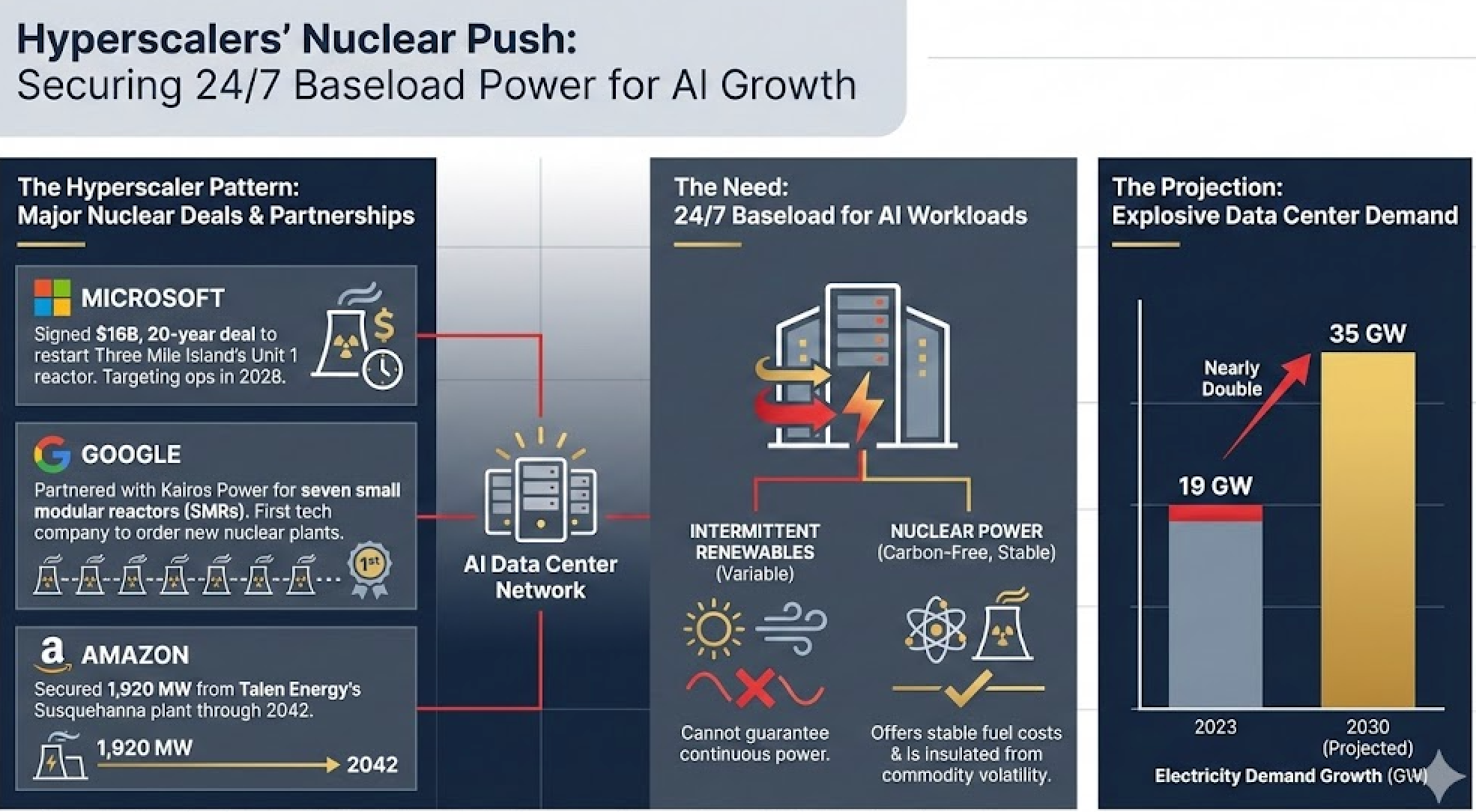

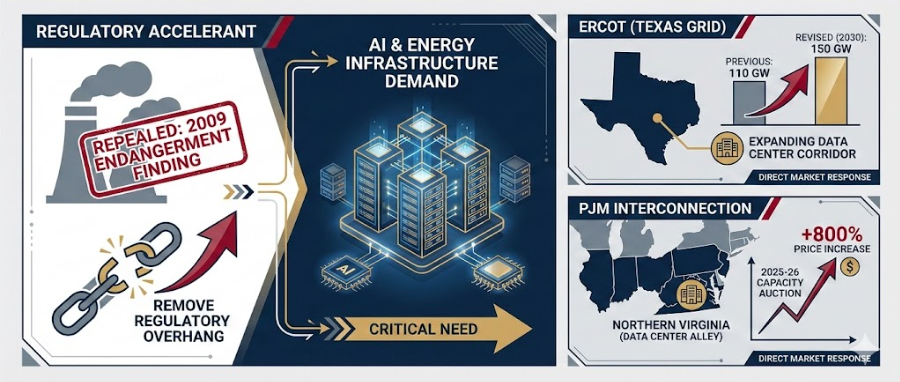

On February 12, the EPA finalized its repeal of the 2009 Endangerment Finding, the scientific and legal determination that greenhouse gas emissions endanger public health and welfare. Administrator Lee Zeldin called it “the single largest deregulatory action in U.S. history.” The repeal eliminates the legal basis for federal regulation of greenhouse gases from vehicles, power plants, oil and gas operations, and industrial facilities. For the AI and energy infrastructure story, this is a direct accelerant, removing the federal regulatory overhang on gas-fired generation at precisely the moment data center operators need it most. The Electric Reliability Council of Texas (ERCOT), which manages the grid serving most of Texas and its rapidly expanding data center corridor, has revised its 2030 capacity needs from 110 GW to 150 GW in a single announcement. PJM Interconnection, the regional transmission organization coordinating the power grid across 13 states from Illinois to New Jersey and home to the densest concentration of data centers in the world (Northern Virginia’s “Data Center Alley”), saw its capacity auction prices for 2025-26 increase over 800% from the year before.

But the repeal simultaneously fragments the regulatory landscape. California and other states retain authority under their own clean air laws. The Motor and Equipment Manufacturers Association (MEMA), an auto parts trade group, specifically asked the EPA to keep greenhouse gas rules for the stability needed to compete globally. Companies now face a two-track compliance world where the federal standard is gone but California’s remains, and the states that follow California’s emissions framework account for roughly a third of the U.S. auto market. The repeal’s original proposal relied heavily on a Department of Energy report written by five known climate skeptics, which a federal judge ruled on January 30 was created through an illegal process. The EPA dropped the controversial report from its final rule entirely, relying instead on a narrow legal argument that Section 202(a) of the Clean Air Act does not authorize emissions standards for climate purposes. Legal experts say this specific framing could create vulnerabilities in court, and the 2007 Supreme Court ruling in Massachusetts v. EPA remains binding precedent. State attorneys general and the U.S. Climate Alliance have already signaled lawsuits.

SO WHAT FOR LEADERS: The GeoTech signal for leaders lies in the intersection of deregulation, grid stress, and AI compute demand. For fossil fuel producers and AI data center operators, the repeal should accelerate permits for gas-fired generation. For grid operators and energy traders, it intensifies the volatility that is already remaking power markets. For manufacturers and automakers, it creates regulatory uncertainty that could become worse than the regulation itself. Business leaders should model permitting and operations under a scenario where federal GHG regulation is gone but state-level regulation intensifies. They also should prepare for two-track compliance, especially in the auto industry. Finally, they should avoid adjustments to their long-term decarbonization strategies based on a rule that could be overturned by the courts. The underlying Supreme Court precedent remains intact.

Japan is executing the most aggressive semiconductor sovereignty play of any advanced economy. Rapidus, Japan’s state-backed 2nm chip venture, is targeting a 50-day wafer cycle time versus the industry standard of 120 days, designed specifically for AI startups and boutique chip designers who prioritize speed over volume. Nvidia is already collaborating with Rapidus on computational lithography. SoftBank and Sony each injected an additional $135 million into Rapidus, becoming its largest private shareholders. Rapidus plans to begin production in the second half of fiscal 2027, scaling from 6,000 to 25,000 wafer starts per month within a year. Rapidus has also launched “Raads,” an AI-assisted chip design tool that uses large language models to help engineers optimize layouts for the 2nm node. Its partnership with IBM and Belgian research hub Imec integrates Rapidus into a Western semiconductor supply chain that’s increasingly wary of over-concentration in the Taiwan Strait.

Simultaneously, TSMC CEO C.C. Wei visited Japan Prime Minister Sanae Takaichi on February 5 to confirm that the company’s second Kumamoto fabrication facility will produce 3nm chips, a dramatic upgrade from the originally planned 6 to 12nm nodes. The total investment is expected to reach $17 billion, with the Japanese government having already approved up to approximately $5 billion in subsidies. And METI’s fiscal 2026 budget allocated 1.23 trillion yen ($7.9 billion) for AI and semiconductors, a nearly 300% increase from previous years. METI has embedded AI and chips into the regular annual budget rather than relying on one-off supplementary allocations, signaling permanent institutional commitment.

The broader policy architecture is equally significant. Japan signed Technology Prosperity Deals with both the United States and South Korea in late 2025, formalizing collaboration on AI, semiconductors, quantum computing, and 6G. Japan leads globally in advanced semiconductor materials and equipment, controlling critical chokepoints in photoresists, silicon wafers, and EUV components. The annual global semiconductor market expanded 25.6% to $791.7 billion in 2025, according to the Semiconductor Industry Association. Deloitte projects that to reach $975 billion in 2026, and the market is expected to surpass $1 trillion by 2027.

SO WHAT FOR LEADERS: Japan’s strategy is qualitatively different from other countries’ chip ambitions. It is simultaneously attracting TSMC’s most advanced commercial node (3nm at Kumamoto), building an indigenous 2nm capability (Rapidus), and leveraging its existing dominance in materials and equipment. Leaders should factor Rapidus and TSMC Kumamoto into their 2028-2030 semiconductor procurement planning. Japan is rapidly becoming a critical supply chain node, and its semiconductor equipment and materials companies (Tokyo Electron, Shin-Etsu, JSR) have become the “picks-and-shovels” play behind both TSMC’s expansion and Rapidus’s buildout. The convergence of AI tools and chip manufacturing is creating “AI-native fabs” that could reshape the economics of semiconductor production. Watch this space.

Under the Radar

The deep analysis that connects the dots

The Power Trader’s New Weapon: How AI, Weather Volatility, and Grid Fragility Are Remaking North American Energy Markets

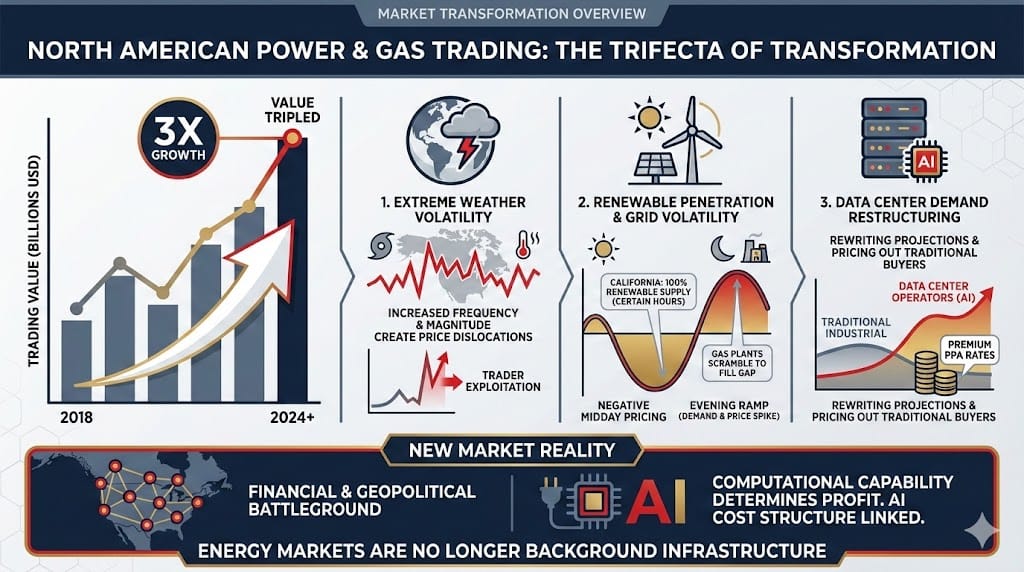

Everyone is watching the AI buildout eat the power grid, but a deeper story is happening in the trading rooms around the country. The value of North American power and gas trading pools have tripled since 2018, to an estimated $10 billion in annual EBIT, according to McKinsey. Within that total, power trading’s share of overall energy trading profits is rising fast, overtaking gas as the primary source of margin growth. Citadel spent $1 billion to acquire natural gas producer Paloma in early 2025, then bought German power-trading firm FlexPower months later, while Balyasny and Jain Global began building physical gas trading operations from scratch. JP Morgan’s head of U.S. power trading called power ‘a macro theme’ now drawing in quantitative funds and macro hedge funds that had never traded electrons before. The players reshaping these markets are not utilities or regulators, they are hedge funds deploying AI to trade volatility that the grid itself is producing.

Three converging forces are driving this transformation. First, extreme weather events are increasing in frequency and magnitude, creating price dislocations that traders can exploit. There have been 273 billion-dollar natural disasters in the U.S. in the past 20 years, compared with 97 in the two prior decades. Canadian droughts have slashed hydroelectric output, cutting electricity exports to the U.S. by nearly 50% and tightening supply in cross-border markets. New England’s grid operator, ISO New England, predicts the region will no longer be a summer-peaking system within five to six years. That means peak electricity demand, historically driven by air conditioning in July and August, will shift to winter heating loads and year-round data center baseload, fundamentally changing when and where price spikes occur.

Second, renewable penetration is amplifying price volatility. In California’s grid, renewable sources now account for 100% of supply during certain hours, producing routinely negative midday wholesale electricity prices followed by steep evening ramp-ups in both demand and price as solar generation drops off and gas plants scramble to fill the gap. Price standard deviations more than doubled from 2016-18 to 2022-23. Weather derivative trading volumes on the Chicago Mercantile Exchange increased more than 250% from 2022 to 2023, a direct response to the growing correlation between weather patterns and power price swings. Catastrophe bond markets have grown 40% over five years.

Third, data centers are rewriting demand projections and restructuring the buyer side of power markets. Data center operators are willing to pay premium power-purchasing agreements at rates that price out traditional industrial buyers. Some, including Amazon and Microsoft, are building or contracting their own dedicated generation facilities. That might reduce their own exposure to grid price swings, but it also pulls generation capacity out of the shared grid, tightening supply for everyone else and increasing the volatility from which traders profit.

The new entrants exploiting these conditions are quantitative hedge funds deploying AI and machine learning for weather prediction, congestion pricing, and real-time dispatch optimization. International energy companies such as Equinor and Shell are translating years of European experience with renewable integration and structured power trading into North American markets, where deregulated wholesale markets offer wider spreads. The definition of what constitutes an “energy company” is expanding to include technology-driven trading firms, AI infrastructure operators, and financial institutions that treat electrons as a tradable commodity class rather than a utility service.

Cambrian Partner By Invitation

Expert analysis from our global network

The Arctic as an Emerging Strategic Market

Greenland's growing prominence in U.S. and allied strategy is emblematic of a broader shift underway in the Arctic. Once viewed primarily through a scientific or environmental lens, the region is now central to discussions about access, resources, and long-term economic and security interests. You need only look at a map to recognize its role as a bridge between the U.S., Indopacific, and Europe.

Yet the region is often misunderstood. The Arctic is not a monolith, but rather a collection of distinct geographies, each shaped by different local politics, infrastructure, and commercial and military requirements. Greenland itself illustrates this reality. Despite its strategic prominence, the country has limited physical infrastructure, only two traffic lights, and a very small number of active mining operations. The potential is real, but it is not plug-and-play, and success depends on understanding conditions on the ground rather than reacting to headlines alone.

What this means for companies

For companies working in Arctic-relevant technologies including defense, sensing, energy, communications, autonomy, infrastructure, and logistics, the opportunity is immediate, but so is the need for precision. Demand is rising faster than governance frameworks, acquisition pathways, and shared operating concepts across allies. In this environment, indigenous communities are critical partners for success and must be engaged early rather than treated as an afterthought. Given the challenging and often expensive operating conditions, success will depend not only on technical performance in extreme environments, but on alignment with policy priorities, region-specific conditions, and missions that span both commercial and public objectives.

About IAF Strategies

Iris Ferguson is a member of the Board of Advisers at Cambrian Futures. She is the former inaugural U.S. Deputy Assistant Secretary of Defense for the Arctic and Global Resilience, and the Founder of IAF Strategies, a boutique strategic advisory firm working with companies, investors, and institutions navigating Arctic opportunities. IAF helps clients develop strategic partnerships and translate policy and geopolitical signals into actionable direction across defense, energy, infrastructure, and emerging Arctic markets.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai