Any Lawful Use Act. The Copycat Trap. The Arsenal Reversal.

IN THIS ISSUE:

CEO's Perspective

Strategic outlook from Cambrian leadership

I grew up in a country that managed to rebuild its entire industrial identity after catastrophic failure. Germans did not do that by clinging to the assumptions of the previous order. They did it by examining what had actually changed, accepting it, partially because they had no other choice, and building forward. We have an opportunity to rebuild and remobilize our global economy with its GeoTech systems, but to do so we need to take a clear-eyed examination of our assumptions.

Prior to the events of the past week, Washington assumed it could dictate the terms of AI procurement to the companies it cannot build without. The Gulf assumed that cheap energy and physical infrastructure were a geopolitical moat. America assumed it was winning the AI race because it was winning the benchmarks. Those seemed like reasonable assumptions in the very recent past but, at best, they’re questionable strategies now. Fortunately, we still have time to recast, and we can start that re-calibration with three steps.

First, recognize that the gap between a planning assumption and a planning variable is where most strategic failures are born. Our assumptions are built on historical patterns that create bias, so take the time to imagine the possible futures that could have greater impact on your organization and triage your portfolios accordingly.

Second, become more comfortable and competent with the verification process in an AI-dominated GeoTech era. Your leaders and your organization should know who checks the machines, the drones, the supply chains, and the robots. This is becoming the most valuable capability in every sector we cover. You need to build this layer into every level of decision making.

Finally, come to grips with the reality that the reversals described here are not temporary disruptions. Ukraine is embedding its expertise in Western defense supply chains. Chinese AI models have become an important tool for Western startups. American battery companies are retooling for AI data centers because the original bet on EVs collapsed.

In the moment, these pivots might feel like current events, but they are signs of structural shifts that we underestimate at our own risk. Do not dismiss the chaos for noise. The signals are right here. Take them seriously.

On the Radar

The signals affecting the GeoTech landscape this week

The Pandora’s Box of the Any Lawful Use Act

The U.S. government is building a new procurement framework that requires AI companies to surrender ethical guardrails as a condition of doing business with the state. Big Tech just told Washington it has limits.

BRIEFING: As Anthropic prepares a court challenge to the Pentagon’s decision to formally designate it as a “supply chain risk,” the GSA issued separate guidance that would require AI companies seeking government contracts to grant the U.S. an irrevocable license for “all lawful purposes.” The draft mandates that contractors must not encode “partisan or ideological judgments” into AI outputs and must disclose whether models have been modified to comply with non-U.S. regulatory frameworks, such as the EU AI Act. Lockheed Martin said it would follow the president’s direction and seek other providers. Palantir, which built its Maven Smart System on Claude, faces a six-month transition timeline during active combat operations against Iran.

But broader industry resistance has also been swift. Microsoft, Google, and Amazon each confirmed that Claude will remain available on their platforms for non-defense work, drawing an explicit line between Pentagon contracts and the rest of their business. In fact, Microsoft and a group of scientists have filed amicus briefs aligning themselves with Anthropic stating potential harm to the software industry. Meanwhile, the Information Technology Industry Council (ITI) sent a formal letter warning War Secretary Pete Hegseth that the designation erodes trust across the technology sector. More than 100 Google employees wrote a separate letter calling for clear red lines in government contracts. OpenAI CEO Sam Altman publicly said enforcing the designation would be “very bad for our industry and our country.” In the week since the designation, more than a million users signed up for Claude each day, lifting it past ChatGPT and Gemini as the top AI app in more than 20 countries. By sticking to its principles, Anthropic has even gained a temporary advantage in the heated battle for top AI talent.

SO WHAT FOR LEADERS: The GSA draft converts AI procurement into a compliance regime, but the implications extend well beyond Anthropic. Any technology company whose products carry ethical guardrails, safety filters, or use-case restrictions that conflict with the administration’s posture is now exposed. The “all lawful purposes” standard ties your liability to whatever the government defines as lawful at any given moment, and those definitions shift with the cascade of political dogma, policy agendas, executive orders, and agency guidance. A use case that is prohibited today could become lawful next month with a policy change you had no role in shaping. If your organization sells AI services to any federal agency, these rules will require an irrevocable license, an anti-bias certification, and disclosure of any non-U.S. regulatory configurations. Accept those terms and you surrender ongoing control of how your technology is used.

The industry pushback matters just as much as the policy itself. When three hyperscalers, the largest tech trade group, your direct competitor, and your own employees all draw the same line in the same week, the resulting boundary becomes a legitimate challenge to the governmental dictate. The designation placed on Anthropic has fractured the AI procurement landscape into companies that operate within or outside of state-defined terms.

Map which lane your organization is in, create clear lines for your sales execs on when and when not to sell to the government under certain terms. Model the exposure of opting out if or when the next contract comes due and create contingency options for quick revenue backfill.

The Copycat Trap

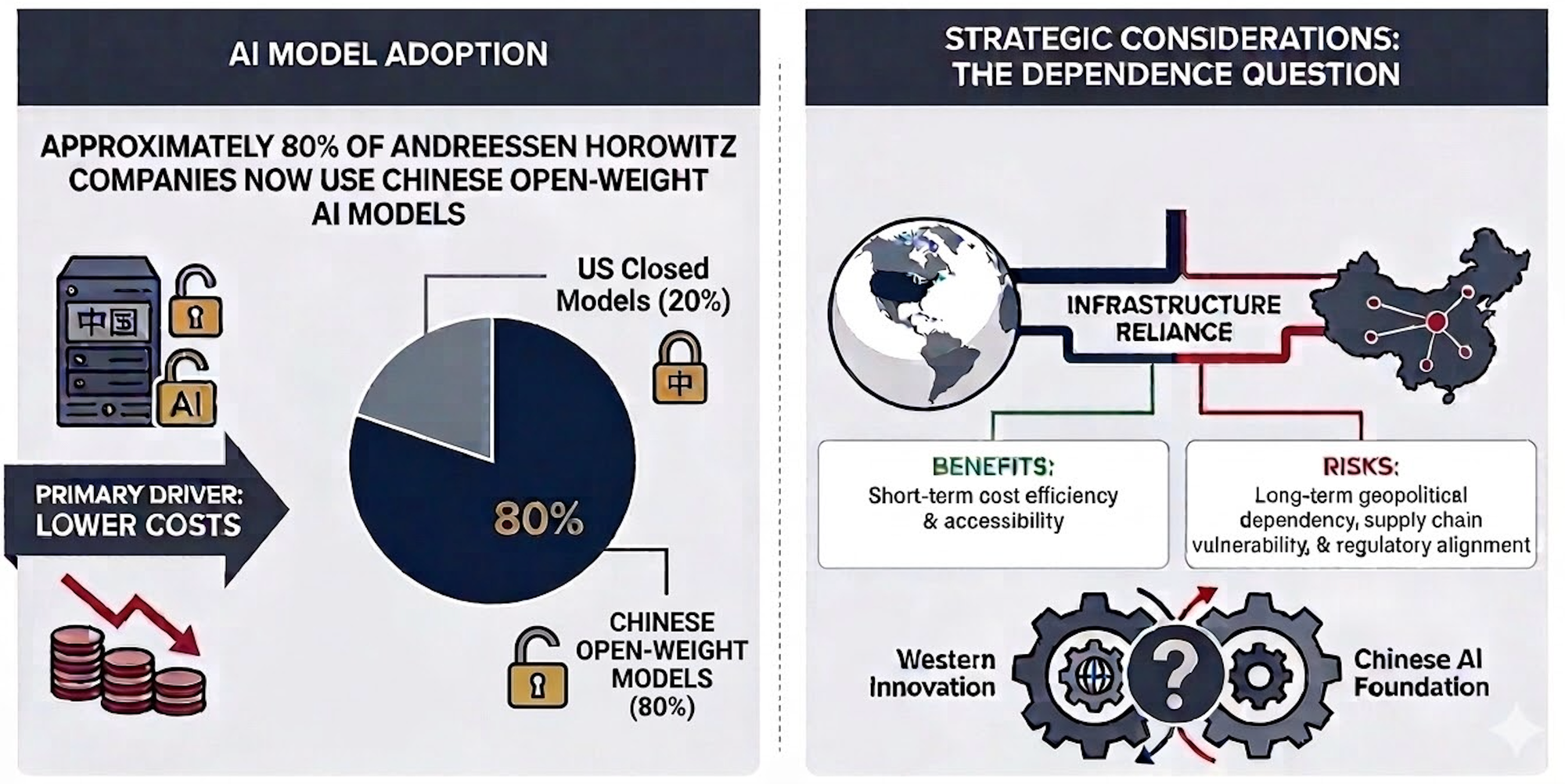

American labs dismiss China’s AI models as imitations. Meanwhile, 80 percent of a top VC firm’s portfolio runs on them. The competition is not where Washington thinks it is.

BRIEFING: The Economist reported in late February that American AI labs increasingly accuse Chinese competitors of copying their techniques. The article cited a16z partner Martin Casado, who estimated that roughly 80 percent of portfolio companies at Andreessen Horowitz now use Chinese open-weight models, driven by inference costs that run orders of magnitude below comparable closed-model pricing from OpenAI and Anthropic. Google DeepMind CEO Demis Hassabis told CNBC in January that Chinese models could be only months behind U.S. capabilities. Nvidia CEO Jensen Huang said the U.S. is “not far ahead” in the broader AI race.

A Stimson Center analysis argued that the U.S. is focused on frontier model breakthroughs while China prioritizes more rapid deployment across manufacturing, logistics, consumer products, and public services. Nathan Lambert’s Interconnects analysis warned that without major Western investment in creating open-weight models in the U.S. or in local markets, Chinese alternatives will continue to increase their lead in both performance and global adoption, potentially allowing Chinese companies to shape the technology interfaces the rest of the world builds on.

SO WHAT FOR LEADERS: The 80 percent figure from a16z should force a reassessment. The strategic question is not whether Chinese open-weight models perform well enough. “Good enough” at a low price point tends to outcompete perfection for most everyday use cases. Rather, it is whether using Chinese AI models as a core component of the AI tech stack makes the Western startup ecosystem overly dependent on China, and what happens to American closed-model providers when the alternative is nearly free. China is not catching up to the U.S. in frontier AI, but it is outflanking American labs by competing on deployment, cost, and distribution while the U.S. competes on benchmarks.

Diagnose which of your use cases are strategically and competitively important, and then choose the model ecosystem based on that assessment. Sometimes your needs will call for a proprietary model, and sometimes open-weight, but make a deliberate decision rather than drifting into one by default.

The Verification Economy

A new economics paper argues that verification, not automation, is the binding constraint of the AI economy. The data is starting to confirm it.

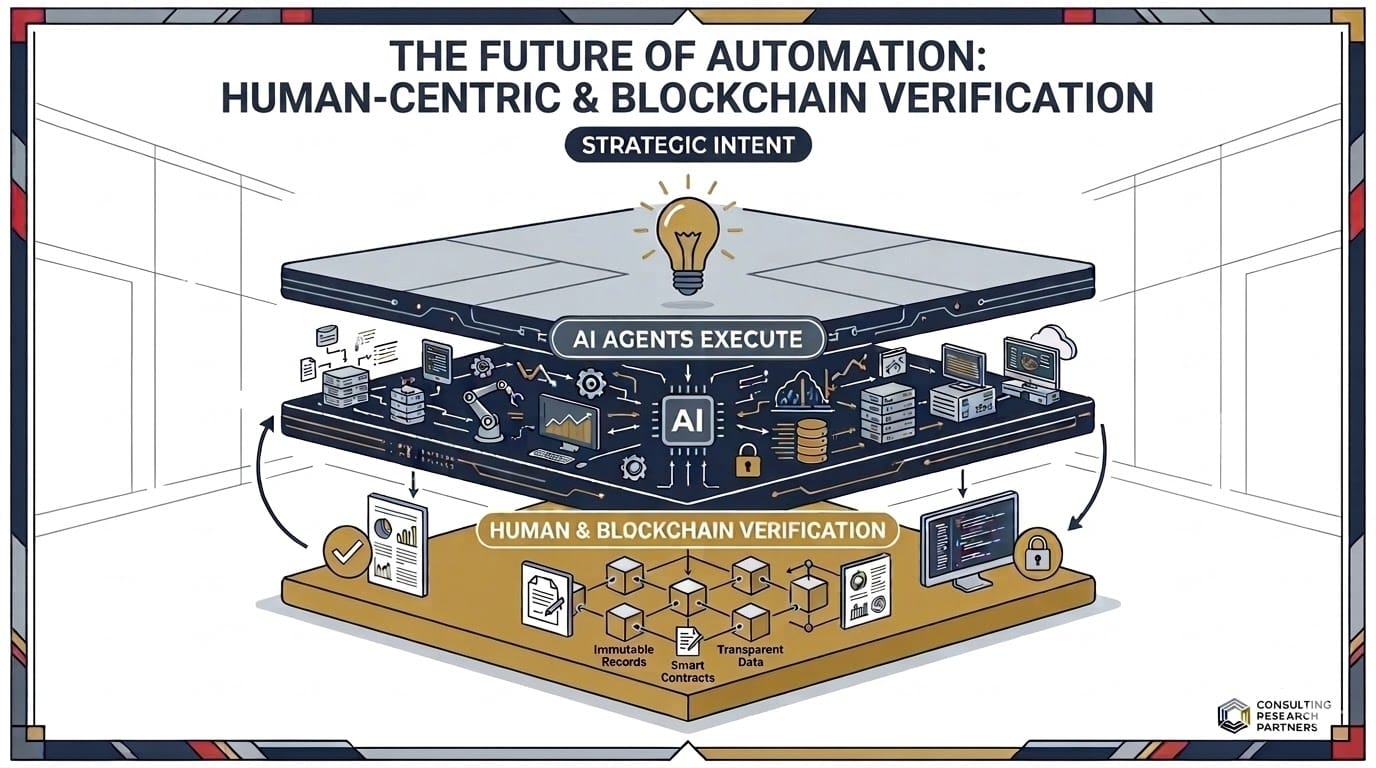

BRIEFING: Christian Catalini, co-founder of Lightspark and founder of the MIT Crypto Economics Lab, published “Some Simple Economics of AGI” in February 2026. The paper argues that anything measurable will be automated, making verification of AI output the most valuable human function in the emerging economy. Catalini describes an “AI sandwich,” where a director sets intent at the top, AI agents execute in the middle, and expert verifiers ensure output quality at the bottom. The paper identifies blockchain networks as a critical verification tool, because information recorded on-chain is cheap to verify, reliable, and trustworthy. Companies shipping unverified AI output are accumulating systemic risk that will surface as failures at scale.

Federal Reserve data supports the framework from two directions. A Dallas Fed analysis found that wages in the most AI-exposed and AI-infused occupations have grown 16.7 percent since late 2022, nearly double the 7.5 percent national average. That confirms Catalini’s prediction: experienced workers who can verify AI output are becoming more valuable as they engage in a symbiosis with AI. But a separate Dallas Fed study found that the job-finding rate for workers under 25 in those same fields has dropped sharply, meaning AI is augmenting senior workers while squeezing out the junior pipeline that produces the next generation of verifiers. Fed Governor Barr warned in February that AI could also shift demand away from professional information work and toward roles that require hands-on experience, physical presence, or human judgment that cannot yet be measured and automated. Anthropic’s own March 5 labor study corroborated the entry-level finding: no systematic unemployment increase for highly exposed workers overall, but suggestive evidence that hiring of younger workers has slowed.

SO WHAT FOR LEADERS: The data increasingly suggests that experienced workers become more valuable and entry-level workers get squeezed out. If your organization is cutting junior roles because AI handles the routine work, you are saving money today while destroying the pipeline of people qualified to check the machine outputs tomorrow. Catalini calls this the codifier’s curse, as the experts who verify AI output simultaneously create training data that could displace them, forcing them to continuously move up the stack.

Build verification tooling now, including automated checking systems, blockchain-based provenance, and expert review workflows. The companies that treat verification as a mere cost center and seek to cut it will suffer the losses when their substandard AI outputs result in failures. The companies that treat it as infrastructure will own the quality layer of the AI economy.

Ukraine’s Defense-Tech Powerhouse Goes Major Leagues in the U.S., Europe, and Beyond

Ukraine built a $50 billion defense industry in four years, flipping from weapon importer to exporter. The first German-Ukrainian drone rolled off the line in February.

BRIEFING: Ukraine’s defense production capacity has grown roughly 50-fold since Russia’s full-scale invasion, reaching an estimated $50 billion to $55 billion annually. Drone and missile production alone could reach $35 billion in 2026. The government authorized wartime defense exports for the first time, with a state commission approving dozens of export license applications. Deputy NSDC Secretary Davyd Aloian estimated export potential for 2026 at “several billion dollars.” Germany, the UK, the Netherlands, Nordic countries, three Middle Eastern states, and at least one Asian country have expressed interest, with particular focus on drones, heavy vehicles, and the FrankenSAM hybrid air defense system that combines Soviet-era launchers with Western missiles. Ukrainian drones, electronic warfare systems, and hybrid air defense platforms have been validated against a peer adversary under conditions no test range can replicate.

Ukraine has taken advantage by embedding itself into Western defense supply chains through joint ventures and co-production rather than traditional arms sales. In February, President Zelensky visited a joint production line between Germany’s Quantum Systems and Ukraine’s Frontline Robotics and received the first jointly produced strike drone. The Quantum Frontline Industries deal is reportedly worth 100 million euros, targeting 10,000 units annually. Similar production lines are running in the UK. Ukrainian manufacturers are competing for U.S. defense contracts and have received invitations to the U.S. Drone Dominance Program, a $1.1 billion competition involving 25 manufacturers worldwide. Brave1, Ukraine’s defense innovation accelerator, will conduct a U.S. venture capital roadshow in March. Meanwhile, Zelensky announced plans for 10 weapons export centers across Europe by the end of 2026, concentrated in the Baltic and Nordic states.

SO WHAT FOR LEADERS: A country that was importing Western weapons four years ago is now exporting scale combat-tested defense technology back to its former suppliers and beyond. This is a remarkably fast transformation that’s looking for equals around the world. For defense procurement leaders, the pipeline of affordable, battlefield-proven systems just expanded significantly. For investors, this is an emerging defense-tech market with sovereign-level demand and NATO-aligned export controls. For legacy defense contractors, it is a new competitor but also potential partner that earned its credibility under fire. Harvest innovation now across defense and civilian dual-use spaces where collaborative autonomy, anti-jamming, positioning and timing, and materials know-how is critical.

The Battery Pivot

America’s EV battery gamble is collapsing. The survivors are pivoting to grid storage and data center backup, where China’s supply chain dominance creates a different problem.

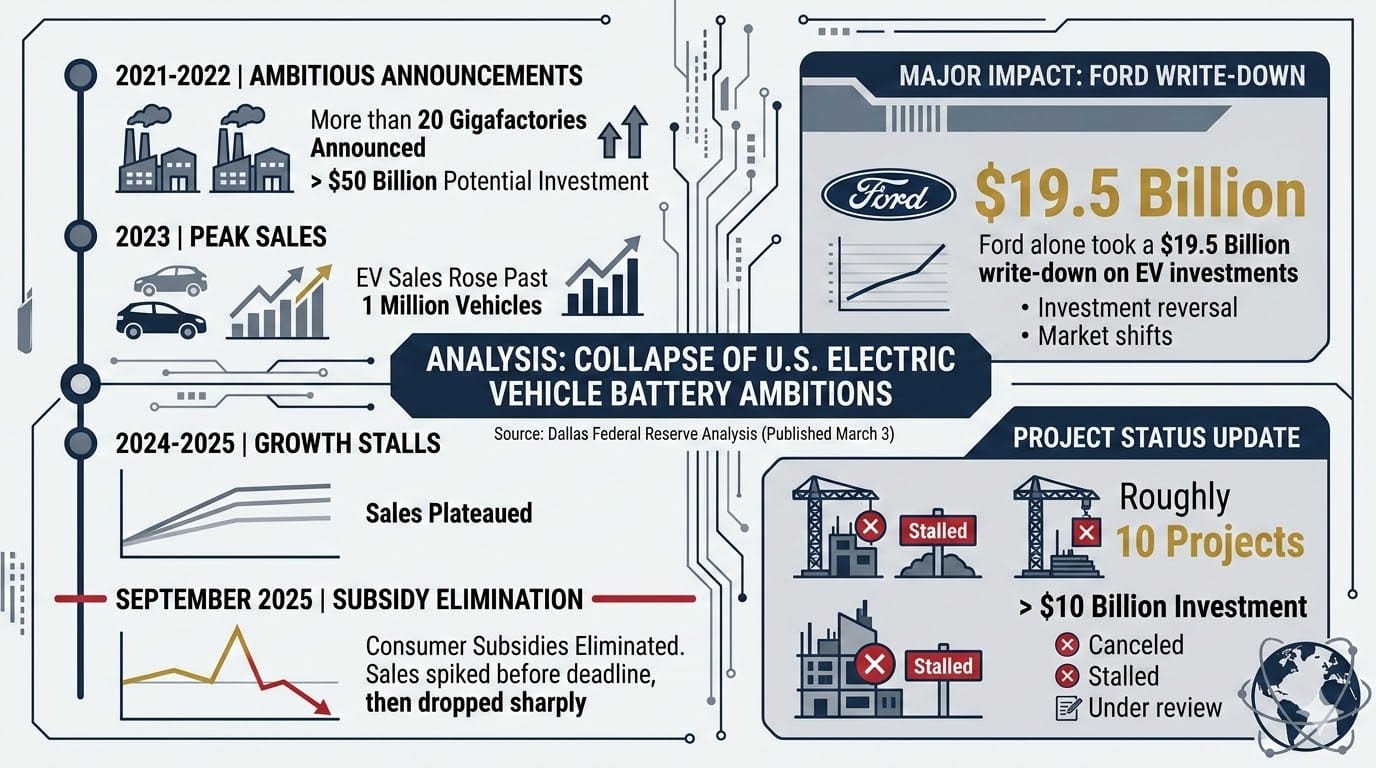

BRIEFING: A March 3 Dallas Federal Reserve analysis documented the collapse of U.S. electric vehicle (EV) battery ambitions. More than 20 gigafactories were announced in 2021 and 2022, representing more than $50 billion in potential investment. EV sales rose past 1 million vehicles in 2023 but plateaued the next two years. Consumer subsidies were eliminated in September 2025, causing sales to spike before the deadline and then drop sharply. Ford alone took a $19.5 billion write-down on EV investments. Roughly 10 projects representing more than $10 billion have been canceled or stalled.

Meanwhile, battery energy storage installations have grown rapidly, driven by falling lithium-ion prices and expanding utility-scale solar. Data centers are emerging as a major new demand source for backup power. The proposed Stargate 1 project in Abilene, Texas, the scope of which has been revised following Oracle’s partial withdrawal but which remains under development with Meta as a potential new partner, could install batteries with a total capacity of 1 gigawatt, roughly 6 percent of all batteries on the U.S. grid in 2025. Tesla, LG Energy, Ford, and others have revised gigafactory plans to include lithium-iron-phosphate (LFP) production alongside or replacing traditional nickel-cobalt-manganese EV batteries. Twelve plants are operating and 23 are under construction, but many face uncertain timelines. The One Big Beautiful Bill Act maintains production and installation tax credits but imposes content requirements and “foreign entity of concern” restrictions that complicate sourcing from Chinese-dominated LFP supply chains.

SO WHAT FOR LEADERS: The U.S. is undermining its own battery competitiveness at the worst possible moment. The U.S. is essentially leaving the global EV market to China’s manufacturers. This was not a deliberate strategic pivot from EVs to data center electrification by the U.S. It was a policy failure that happened to collide with a separate surge in demand from a different industry. No one in Washington planned to redirect battery capacity from electric vehicles to AI data centers. Thanks to a strategic decommitment by the new administration, automakers abandoned EV targets because consumers would not buy the cars at the prices on offer, and battery manufacturers are chasing grid storage and data center backup because that is where the remaining demand is. That also means, however, that the policy framework has not caught up to the shift. China dominates every stage of the LFP supply chain, from cathode materials to cell production, and the One Big Beautiful Bill Act’s foreign entity restrictions block the very suppliers that could help domestic manufacturers scale. The result is a policy framework that simultaneously demands domestic production and cuts off access to the technology, materials, and expertise needed to achieve it. This cuts learning curves. History rhymes: the U.S. made the same mistake with car batteries.

For auto suppliers and Tier 1 manufacturers that retooled for EV battery production, the question is whether to chase the LFP pivot or write off the investment. Companies with existing relationships in the Chinese LFP supply chain face regulatory exposure under the foreign entity rules. Companies without those relationships face a multi-year ramp to build domestic LFP capability. Either way, the planning horizon just compressed. Assess which of your battery-adjacent investments can be redirected toward grid storage and data center applications, identify which supplier relationships need restructuring before the foreign entity restrictions take full effect, and search for small pockets of LFP expertise globally.

Under the Radar

The deep analysis that connects the dots

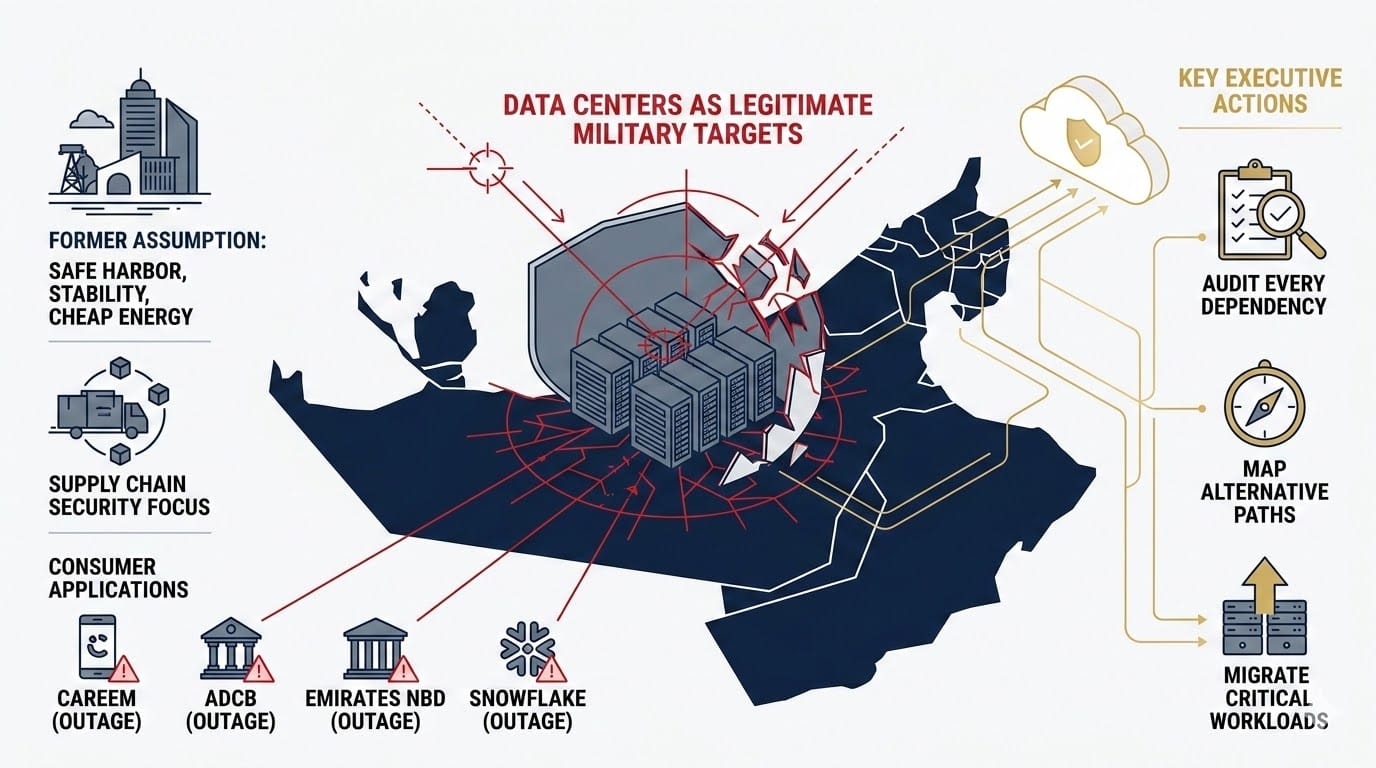

Compute in the Crosshairs

The Gulf sold itself as a safe harbor for the world’s cloud. Then missiles hit its data centers.

Commercial shipping through both the Strait of Hormuz and the Red Sea has effectively halted due to the conflict. The undersea fiber-optic cables that run through these corridors, which carry a significant share of the data traffic linking Europe and Asia, have not been physically severed in the current conflict but face elevated risk from naval activity, debris, and the same conditions that damaged four Red Sea cables in 2024. The threat is disruption and degradation, not a clean shutdown. Data can be rerouted, but at higher latency and cost, and the Gulf data centers that those cables serve are themselves under direct physical attack. Bahrain’s state oil firm declared force majeure after an Iranian strike set fire to its only oil refinery. Energy companies in Kuwait and Qatar triggered similar clauses. Oil prices surpassed $119 before pulling back, and stocks tumbled across Asia. The Gulf has become the chokepoint for oil and data alike.

Three AWS data centers were damaged in the initial wave of strikes, a fact reported in Issue 9, and AWS has since advised customers to migrate workloads out of the Middle East entirely. The more significant development is the scale of disruption to Gulf-based compute capacity. AWS operates three availability zones in the UAE and three in Bahrain. With two UAE zones and one Bahrain zone impaired, roughly half of Amazon’s regional cloud capacity has been degraded. Consumer-facing services including ride-hailing, banking, payments, and enterprise data platforms experienced elevated error rates and outages across the region. Bloomberg reported that Israel and the U.S. also struck at least two data centers in Tehran, one connected to the IRGC, establishing a precedent in which both sides of a conflict deliberately target data infrastructure. The IRGC confirmed it hit the Bahrain AWS facility specifically because of its support for U.S. military operations, treating commercial cloud infrastructure as a legitimate military target.

The GeoTech Signal

With a host of agreements and billions of dollars of data center investments at stake, Gulf officials are already considering how to harden data center defenses against missile strikes rather than just cyberattacks.

Leaders with cloud, AI, or data exposure in the Gulf will need to assess which compute capacity or data pools have been impacted where, and then route their traffic accordingly through data centers in Europe, Central and South Asia. This is non-trivial for you and host governments, as those contingency data centers will inevitably become targets as well. As you reassess, consider and respect data sovereignty policies, because you might need to build redundancy across the region quickly for workloads that cannot be moved and possible future attacks on infrastructure. The Gulf’s AI thesis requires a full security redesign that accounts for kinetic risk at the same level as cyber risk. Until that redesign is complete, treat Gulf compute availability as a planning variable, not a planning assumption.

Cambrian Partner By Invitation

Expert analysis from our global network

Europe's $400 Million Bargaining Chip: ASML Must Become a Continental Strategy

A recent Veritasium documentary entitled, "The World's Most Important Machine" has brought unprecedented public attention to what may be the most complex machine ever built: ASML's extreme ultraviolet (EUV) lithography system for advanced semiconductor chip manufacturing. The numbers are staggering, to quote: Inside each $400 million machine, a laser strikes 50,000 tiny tin droplets per second, heating each one to 220,000 degrees Kelvin, roughly 40 times hotter than the surface of the sun. The Zeiss mirrors guiding the light are so precise that, scaled to the diameter of the Earth, the largest surface imperfection would be no thicker than a playing card. If you placed a hypothetical laser on one of the servos that constantly focus a mirror, it would move by a small enough angle that you could choose which side of a dime (left or right) you want to hit on the moon. The machine overlays one layer of a chip perfectly on top of another and is never off by more than five atoms, all while parts of the machine whip around with accelerations of over 20 g's. When asked how often the laser misses its target, ASML's founders offered a disarmingly simple answer: it doesn't... ever! This is not just engineering at the extreme. It is the technological chokepoint upon which the entire AI economy, and the global semiconductor supply chain, now depends.

SO WHAT

ASML is a Dutch company, but the leverage it represents belongs to all of Europe. Right now, that leverage is being shaped largely by U.S. export control decisions rather than by a coordinated European strategy. That needs to change. European leaders, not just in the Netherlands, but in Germany, France, Italy, and across the semiconductor supply chain, should treat ASML's monopoly as continental strategic infrastructure. Concretely, EU policymakers should: (1) Elevate ASML's role within the EU Chips Act 2.0 framework, ensuring lithography leadership is protected and funded as a pan-European advantage, not a single-nation asset. (2) Use ASML's irreplaceable position to negotiate reciprocal technology access, investment terms, and AI governance standards with the U.S. and key Asian partners. (3) Pull the broader European semiconductor ecosystem, including Zeiss optics and Trumpf lasers in Germany, IMEC research in Belgium, STMicroelectronics' silicon carbide fabs in Italy, Nordic Semiconductor's IoT chip design in Norway, and Arm's processor architectures in the UK, into a unified industrial strategy that converts component excellence into geopolitical weight. The machine that creates miniature supernovas 50,000 times per second should not be a passive pawn in someone else's trade policy. It should be the fulcrum of Europe's seat at the table.

About the Authors

Olaf Groth is the founder/CEO of Cambrian Futures and Professional Faculty at UC Berkeley Haas.

Joe Kewekordes is an entrepreneur-engineer and the co-founder of AutoMate Scientific (successfully exited). Specializing in biotech electronics, Joe spends his time exploring and reviewing the latest innovations in hardware and software.

About Cambrian

Cambrian Futures is a strategic foresight and advisory firm helping government, business, and technology leaders understand how emerging technologies intersect with geopolitics, markets, and national strategy. By combining rigorous research, AI-enabled analysis, and human expertise, Cambrian provides clear insight into global technology trends, risks, and power dynamics. Its work helps decision-makers anticipate disruption, manage uncertainty, and act with strategic confidence in an increasingly competitive GeoTech world.

PRODUCTION TEAM

GeoTech Radar is produced by the Cambrian Futures Insights Platform team:

CEO & Chief Analyst

Managing Director / Producer, Insights Platform

Global Lead, Smart Infrastructure Strategy

Research & Marketing Associate

Editor in Chief

Learn more about Cambrian Futures at cambrian.ai

Produced with

Cite as: Cambrian Futures (2026) 'GeoTech Radar Issue 10'